AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 61:

Sound internal control dictates that, immediately upon receiving checks from customers by mail, a responsible employee should:

A. Add the checks to the daily cash summary. B. Verify that each check is supported by a prenumbered sales invoice. C. Prepare a duplicate listing of checks received. D. Record the checks in the cash receipts journal.

C. Prepare a duplicate listing of checks received. Choice "c" is correct. Upon receipt of cash, a remittance listing should be prepared. Choice "a" is incorrect. Recording the check in the daily cash summary would ordinarily be done by a second party after the initial listing has been prepared. Choice "b" is incorrect. Verifying that each check is supported by a valid invoice is not necessary. Choice "d" is incorrect. Recording the check in the cash receipts journal would ordinarily be done by a second party after the initial listing has been prepared.

Question 62:

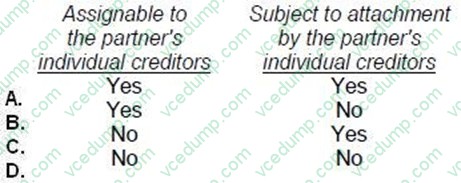

A partner's interest in specific partnership property is:

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. No - No. Rule: A partner's interest in specific partnership property is neither assignable to the partner's individual creditors nor is it subject to attachment by the partner's individual creditors. Choices "a", "b", and "c" are incorrect, per the above rule.

Question 63:

Allen owns 100 shares of ABC Corp., a publicly-traded company, which Allen purchased on January 1, 2001, for $10,000. On January 1, 2003, ABC declared a 2-for-1 stock split when the fair market value (FMV) of the stock was $120 per share. Immediately following the split, the FMV of ABC stock was $62 per share. On February 1, 2003, Allen had his broker specifically sell the 100 shares of ABC stock received in the split when the FMV of the stock was $65 per share. What amount should Allen recognize as long-term capital gain income on his Form 1040, U.S. Individual Income Tax Return, for 2003?

A. $300 B. $750 C. $1,500 D. $2,000

C. $1,500 Choice "c" is correct. The receipt of a nontaxable stock dividend will require the shareholder to spread the basis of his original shares over both the original shares and the new shares received, resulting in the same total basis but a lower basis per share of stock held. Therefore, Allen's total basis remains the same, $10,000, but is now split between 200 shares (a 2-for-1 split and he originally owned 100 shares). Therefore, his basis per share goes from $100/share ($10,000/100) to $50/share ($10,000/200). Consequently, his basis in the 100 shares sold is 100 x $50 = $5,000. Calculate his gain as follows: Choices "a", "b", and "d" are incorrect.

Question 64:

During 20X5, ABC Corp. made the following accounting changes:

What amount should be shown in the 20X5 retained earnings statement as an adjustment to the beginning balance?

A. $0 B. $30,000 C. $98,000 D. $128,000

C. $98,000 Choice "c" is correct. $98,000. The cumulative effect of a change in accounting principle is now shown on the retained earnings statement as an adjustment to the beginning balance of retained earnings, assuming that the cumulative effect can be calculated. A change from LIFO to FIFO for inventory valuation (costing) is a change in accounting principle. An exception is made however, for a change in depreciation method, since a change in depreciation method is no longer considered to be a change in accounting principle. A change in depreciation method is now considered to be both a change in principle and a change in estimate. These changes should now be accounted for as a change in estimate and handled prospectively. The new depreciation method should be used as of the beginning of the year of change and should start with the current book value of the underlying asset. No retroactive or retrospective calculations should be made, and no adjustment should be made to retained earnings. Choices "a", "b", and "d" are incorrect, per the above Explanation.

Question 65:

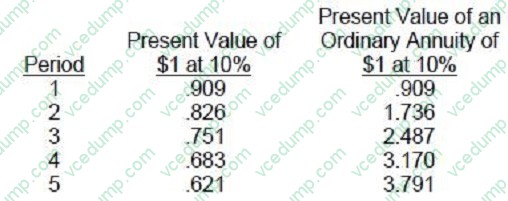

In order to increase production capacity, ABC Industries is considering replacing an existing production machine with a new technologically improved machine effective January 1, 1997. The following information is being considered by ABC

Industries.

?The new machine would be purchased for $160,000 in cash. Shipping, installation, and testing would cost an additional $30,000.

?The new machine is expected to increase annual sales by 20,000 units at a sales price of $40 per unit. Incremental operating costs are comprised of $30 per unit in variable costs and total fixed costs of $40,000 per year.

?The investment in the new machine will require an immediate increase in working capital of $35,000. ?ABC uses straight-line depreciation for financial reporting and tax reporting purposes. The new machine has an estimated useful life of

five years and zero salvage value. ?ABC is subject to a 40 percent corporate income tax rate. ABC uses the net present value method to analyze investments and will employ the following factors and rates.

ABC Industries' net cash outflow in a capital budgeting decision would be:

A. $190,000 B. $195,000 C. $204,525 D. $225,000

D. $225,000 Explanation Explanation/Reference:Choice "d" is correct. $225,000 net cash outflow. Choices "a", "b", and "c" are incorrect, per the above calculation. Note: This question is the first from a series of questions on a prior exam. The last in the series is presented for you in the regular homework questions (not the supplemental questions) for this chapter.

Question 66:

A limited partnership must have:

A. One general partner and two limited partners. B. All must be general partners and one limited partner. C. One general partner and one limited partner. D. All limited partners.

C. One general partner and one limited partner. Choice "c" is correct. Rule: A limited partnership must have at least one general partner and one limited partner. Choices "a", "b", and "d" are incorrect, per the above rule. Be careful of answers that include the word "all."

Question 67:

A sole proprietorship would be an ideal form of business to select if:

A. The individual desired no liability beyond his capital investment. B. The individual wanted to be able sell the business at will. C. The individual wanted the business to be a separate entity from the sole proprietor. D. The individual wanted the business to continue indefinitely.

B. The individual wanted to be able sell the business at will. Choice "b" is correct. A sole proprietor is free to transfer or sell the business at will. Choice "a" is incorrect because a sole proprietor is personally liable for all obligations of the business. Choice "c" is incorrect. A sole proprietorship is not considered an entity separate from the sole proprietor. Choice "d" is incorrect because a sole proprietorship ends with the death of the sole proprietor.

Question 68:

All of the following capital budgeting analysis techniques use cash flows as the primary basis for the calculation, except for the:

A. Net present value. B. Internal rate of return. C. Discounted payback period. D. Accounting rate of return.

D. Accounting rate of return. Choice "d" is correct. The accounting rate of return does not use cash flows as the primary basis for the calculation. It measures the accrual accounting return instead of cash flows: Choice "a" is incorrect. Net present value method discounts cash flows for an investment over its life to time period zero using a desired or minimum rate of return. Choice "b" is incorrect. Internal rate of return (IRR) determines the compound interest rate of an investment where the present value of the cash inflows equals the present value of the cash outflows. The IRR is the discount rate that results in a net present value of zero. Choice "c" is incorrect. The discounted payback period is the time period required for discounted cash inflows to equal the initial investment. The time value of money is considered.

Question 69:

At the beginning of year 1, $10,000 is invested at 8% interest, compounded annually. What amount of interest is earned for year 2?

A. $800.00 B. $806.40 C. $864.00 D. $933.12

C. $864.00 Choice "c" is correct. This question is a compound interest question because the interest is to be determined at the end of the second year. The calculation is as follows and uses different symbols than the SI = PIN formula in the text to show candidates the PRT formula as well (the CPA exam often uses different terminology): Interest = PRT (for the first year) Interest = $1,000 x .08 x 1 = $800 and adding the $800 to the beginning principal Interest = PRT (for the second year) Interest = $1,800 x .08 x 1 = $864 It is obvious from the answer that the interest earned in year 2 is interest earned on the original principal ($10,000 x .08 = $800) plus interest on the year 1 interest ($800 x .08 = $64). Choice "a" is incorrect. This answer is interest only on the original principal, and not on the year 1 interest. Choice "b" is incorrect. This answer has a decimal point error in calculating the year 2 interest on year 1 interest. Choice "d" is incorrect. This answer is apparently made up. It is sometimes difficult to come up with 3 decent wrong answers, especially with simple questions.

Question 70:

Two assertions for which confirmation of accounts receivable balances provides primary evidence are:

A. Completeness and valuation. B. Valuation and rights and obligations. C. Rights and obligations and existence. D. Existence and completeness.

C. Rights and obligations and existence. Choice "c" is correct. Two assertions for which the confirmation of accounts receivable balances provides primary evidence are rights and obligations (does the client have a right to the receivable?) and existence (does the receivable really exist?). Choices "a", "b", and "d" are incorrect. Confirmation of receivables does not provide evidence about completeness, since the sample begins with recorded receivables. (To test completeness, we would be looking for unrecorded receivables). In addition, confirmation of receivables does not necessarily provide evidence related to the valuation assertion. While the existence of the receivables is confirmed, their collectability is not.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.