CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

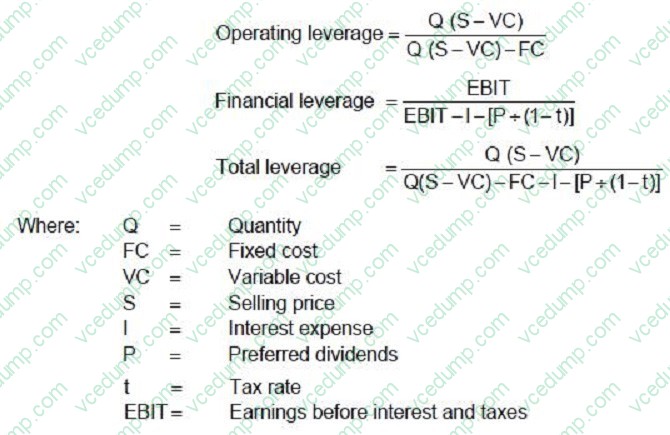

Question 81:

ABC Company presently sells 400,000 bottles of perfume each year. Each bottle costs $.84 to produce and sells for $1.00. Fixed costs are $28,000 per year. The firm has annual interest expense of $6,000, preferred stock dividends of $2,000 per year, and a 40 percent tax rate. ABC uses the following formulas to determine the company's leverage.

The degree of operating leverage for ABC Company is:

A. 2.4

B. 1.78

C. 1.35

D. 2.3 -

Question 82:

When an auditor submits a document containing audited financial statements to a client, and those financial statements include supplementary information required by GAAP, the auditor may choose any of the following options, except:

A. Express an opinion on the information, if he or she has been engaged to examine such information.

B. Express negative assurance on the information, if review procedures have been appropriately performed.

C. Report on whether the information is fairly stated in relation to the financial statements taken as a whole, if appropriate auditing procedures have been applied.

D. Disclaim an opinion on the information. -

Question 83:

Which of the following statements is correct regarding both debt and common shares of a corporation?

A. Common shares represent an ownership interest in the corporation, but debt holders do not have an ownership interest.

B. Common shareholders and debt holders have an ownership interest in the corporation.

C. Common shares typically have a fixed maturity date, but debt does not.

D. Common shares have a higher priority on liquidation than debt. -

Question 84:

This question will represent a statement, question, excerpt, or comment taken from various parts of an auditor's documentation file. Letter choices A-P represent a list of the likely sources of the statement, question, excerpt, or comment.

Select, as the best answer for each item, the most likely source. Select only one source for each item.

The company considers the decline in value of equity securities classified as available-for-sale to be temporary.

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements.

B. Auditor's communications on significant deficiencies in internal control.

C. Audit inquiry letter to legal counsel.

D. Lawyer's response to audit inquiry letter.

E. Communication from those charged with governance to the auditor.

F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies in internal control).

G. Report on the application of accounting principles.

H. Auditor's engagement letter.

I. Letter for underwriters.

J. Accounts receivable confirmation request. K. Request for bank cutoff statement. L. Explanatory paragraph of an auditor's report on financial statements. M. Partner's engagement review notes. N. Management representation letter. O. Successor auditor's communication with predecessor auditor. P. Predecessor auditor's communication with successor auditor. -

Question 85:

When audited financial statements are presented in a client's document containing other information, the auditor should:

A. Perform inquiry and analytical procedures to ascertain whether the other information is reasonable.

B. Add an explanatory paragraph to the auditor's report without changing the opinion on the financial statements.

C. Perform the appropriate substantive auditing procedures to corroborate the other information.

D. Read the other information to determine that it is consistent with the audited financial statements. -

Question 86:

If a retailer's terms of trade are 3/10, net 45 with a particular supplier, what is the cost on an annual basis of not taking the discount? Assume a 360-day year.

A. 37.11 percent.

B. 36.00 percent.

C. 24.74 percent.

D. 31.81 percent. -

Question 87:

In auditing intangible assets, an auditor most likely would review or recompute amortization and determine whether the amortization period is reasonable in support of management's financial statement assertion of:

A. Valuation and allocation.

B. Existence.

C. Completeness.

D. Rights and obligations. -

Question 88:

Which of the following controls is most likely to prevent the improper disposition of equipment?

A. A separation of duties between those authorized to dispose of equipment and those authorized to approve removal work orders.

B. The use of serial numbers to identify equipment that could be sold.

C. Periodic comparison of removal work orders to authorizing documentation.

D. A periodic analysis of the scrap sales and the repairs and maintenance accounts. -

Question 89:

Audit documentation serves mainly to:

A. Provide the principal support for the auditor's report.

B. Satisfy the auditor's responsibilities concerning the Code of Professional Conduct.

C. Monitor the effectiveness of the CPA firm's quality control activities.

D. Document the level of independence maintained by the auditor. -

Question 90:

When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the:

A. Option A

B. Option B

C. Option C

D. Option D

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.