AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 51:

Ryan, age 57, is single with no dependents. On July 1, 1997, Ryan's principal residence was sold for the net amount of $500,000 after all selling expenses. Ryan bought the house in 1963 and occupied it until sold. On the date of sale, the house had a basis of $180,000. Ryan does not intend to buy another residence. What is the maximum exclusion of gain on sale of the residence that may be claimed in Ryan's 1997 income tax return?

A. $320,000 B. $250,000 C. $125,000 D. $0

B. $250,000 Choice "b" is correct. $250,000 maximum exclusion from taxable income. Rule: An individual may exclude from income up to $250,000 gain provided that the property was the taxpayer's primary residence for 2 of the last 5 years. Married taxpayers may exclude gains up to $500,000. Choice "a" is incorrect. $320,000. Ryan, age 57, was not married. Thus, his exclusion was limited to $250,000. Choice "c" is incorrect. The $125,000 exclusion was old law and eliminated for sales after 5/6/97. Choice "d" is incorrect, per the above rule.

Question 52:

If a firm increases its cash balance by issuing additional shares of common stock, working capital:

A. Remains unchanged and the current ratio remains unchanged. B. Increases and the current ratio remains unchanged. C. Increases and the current ratio decreases. D. Increases and the current ratio increases.

D. Increases and the current ratio increases. Choice "d" is correct. If a firm increases its cash balance by issuing additional shares of common stock, working capital increases and the current ratio increases.

Question 53:

The quarterly data required by SEC Regulation S-K have been omitted. Which of the following statements must be included in the auditor's report?

A. The auditor was unable to review the data. B. The company's internal control provides an adequate basis to complete the review. C. The company has not presented the selected quarterly financial data. D. The auditor will review the selected data during the review of the subsequent quarterly financial data.

C. The company has not presented the selected quarterly financial data. Choice "c" is correct. If the quarterly data required by SEC Regulation S-K have been omitted, the auditor's report must include a statement indicating that the company has not presented such data. Choice "a" is incorrect. The auditor's report should only state that the auditor was unable to review quarterly data required by SEC Regulation S-K when the data have been included, but the auditor has not reviewed such data. Choice "b" is incorrect. Generally, the auditor's report does not make reference to a review of interim financial information, since such information is not a required part of GAAP financial statements. (Note, however, that the auditor's report might be modified to indicate that the company's internal control was not sufficient to provide an adequate basis for a review of such information, in situations where quarterly data is included but not reviewed). Choice "d" is incorrect. If an entity is required to file quarterly reports, a review of this quarterly data is also required. Such review should be completed before the quarterly report is filed, not postponed to a subsequent quarter.

Question 54:

Which of the following activities is considered a support activity?

A. Delivery of products. B. Procurement of materials. C. Product advertising. D. In-home warranty service.

B. Procurement of materials. Choice "b" is correct. Support activities are those activities that are performed by the support staff of an organization (e.g., purchasing of materials and supplies, development of the technology used, management of employees, accounting, finance, strategic planning, etc.). Choices "a", "c", and "d" are incorrect, as these are all considered primary activities. Primary activities are those that are involved with the direct manufacture of products, the delivery of products through distribution channels, and the support of the product that exists after the sale is made (e.g., handling the raw materials, the manufacturing process, taking orders for the product, advertising the product, and servicing the product after it is sold).

Question 55:

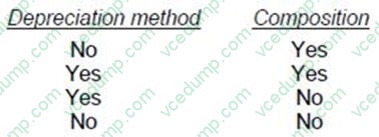

Which of the following facts concerning fixed assets should be included in the summary of significant accounting policies?

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. Yes - No. Yes - "Depreciation methods" should be disclosed in the "summary of significant accounting policies." No - Composition of fixed assets (or any other account) should not be disclosed in the "summary of significant accounting policies."

Question 56:

For a nonissuer, a previously communicated significant deficiency that has not been corrected, ordinarily should be communicated again:

A. Only if the deficiency has a material effect on the auditor's assessment of control risk. B. Unless the entity accepts that degree of risk because of cost-benefit considerations. C. Only if the deficiency is considered a material weakness. D. In writing, during the current audit.

D. In writing, during the current audit. Choice "d" is correct. A previously communicated significant deficiency that has not been corrected ordinarily should be communicated again in writing, during the current audit. Choices "a" and "c" are incorrect. The auditor is required to communicate significant deficiencies each year, regardless of whether the deficiency has a material effect on the auditor's assessment of control risk or the deficiency is considered a material weakness. Choice "b" is incorrect. The auditor is required to communicate significant deficiencies each year, even if the entity accepts that degree of risk because of cost-benefit considerations.

Question 57:

An auditor vouched data for a sample of employees in a payroll register to approved clock card data to provide assurance that:

A. Payments to employees are computed at authorized rates. B. Employees work the number of hours for which they are paid. C. Segregation of duties exists between the preparation and distribution of the payroll. D. Internal controls relating to unclaimed payroll checks are operating effectively.

B. Employees work the number of hours for which they are paid. Choice "b" is correct. By vouching to time card data, the auditor is testing the existence assertion for hours worked. Choice "a" is incorrect. Vouching to approved time card data would provide evidence about hours worked, not pay rates. Pay rates would be tested by comparing to personnel records. Choice "c" is incorrect. Vouching to approved time cards does not provide evidence about segregation of duties. Choice "d" is incorrect. Vouching to the approved time cards does not provide evidence about internal controls related to unclaimed paychecks. The auditor would need to observe a payroll distribution to evaluate these controls.

Question 58:

Which of the following procedures would an auditor least likely perform in planning a financial statement audit?

A. Coordinating the assistance of entity personnel in data preparation. B. Discussing matters that may affect the audit with firm personnel responsible for non-audit services to the entity. C. Selecting a sample of vendors' invoices for comparison to receiving reports. D. Reading the current year's interim financial statements.

C. Selecting a sample of vendors' invoices for comparison to receiving reports. Choice "c" is correct. Selecting a sample of vendors' invoices for comparison to receiving reports is performed during fieldwork. This is not part of the planning phase. Choice "a" is incorrect. Coordinating the assistance of entity personnel in data preparation is usually performed during the planning phase. Choice "b" is incorrect. During the planning phase, matters that may affect the audit should be discussed with firm personnel responsible for non-audit services to the entity. Choice "d" is incorrect. During the planning phase, the auditor generally would read the current year's interim financial statements.

Question 59:

In testing long-term investments, an auditor ordinarily would use analytical procedures to ascertain the reasonableness of the:

A. Completeness of recorded investment income. B. Classification between balance sheet portfolios. C. Valuation of marketable equity securities. D. Existence of unrealized gains or losses in the portfolio.

A. Completeness of recorded investment income. Choice "a" is correct. In testing long-term investments, an auditor ordinarily would use analytical procedures to ascertain the reasonableness of the completeness of recorded investment income. These procedures would probably include a comparison of the recorded investment income with the expected amount (based upon the related interest rate, dividends declared, etc.) and the income balance audited in the prior year. Choice "b" is incorrect. Classification between balance sheet portfolios would most likely be tested by confirming the terms of the investment and making inquiries of management regarding how long they intend to hold the securities. Choice "c" is incorrect. To test the valuation of marketable equity securities an auditor would most likely compare to market quotations (cost method) or examine the audited financial statements of the investee company (equity method). Choice "d" is incorrect. To identify and quantify the existence of unrealized gains and losses in the portfolio, an auditor would examine the trading prices in the Wall Street Journal (or other source) for those long-term investments carried under the cost method. For those carried under the equity method, an auditor would review the audited financial statements of the investee company.

Question 60:

What term is used to describe a partnership without a specified duration?

A. A perpetual partnership. B. A partnership by estoppel. C. An indefinite partnership. D. A partnership at will.

D. A partnership at will. Choice "d" is correct. A partnership at will is a partnership with no definite term (i.e., without specified duration). Such a partnership can be terminated at any time. Choice "a" is incorrect. A partnership without a specified duration is called a partnership at will, not a perpetual partnership. There is no such thing as a perpetual partnership because a partnership is not perpetual. A partnership may be dissolved after a partner dies or otherwise dissociates from the partnership. Choice "b" is incorrect. A partnership by estoppel is the appearance of a partnership when there is no formal partnership. If parties who are not partners give the appearance to third parties that they are partners, the law may deem the parties to be a partnership by estoppel. The parties will be treated as partners, even though they are not. Choice "c" is incorrect. The legal term for a partnership of indefinite duration is a partnership at will, not an indefinite partnership.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.