AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1:

The net present value (NPV) of a project has been calculated to be $215,000. Which one of the following changes in assumptions would decrease the NPV?

A. Decrease the estimated effective income tax rate. B. Extend the project life and associated cash inflows. C. Increase the estimated salvage value. D. Increase the discount rate.

D. Increase the discount rate. Choice "d" is correct. An increase in the discount rate will decrease the present value of future cash inflows and, therefore, decrease the net present value of the project. Each of the other options would increase the NPV: Choice "a" is incorrect. A decrease in the estimated effective income tax rate will reduce the depreciation tax shield and therefore increase the cash inflow. A larger cash inflow in the future will increase the present value of the cash inflows and therefore increase the net present value of the project. Choice "b" is incorrect. Increasing the project life and associated cash inflows will increase the present value of the cash inflows and therefore increase the net present value. Choice "c" is incorrect. An increase in the estimated salvage value will decrease the present value of the cash outflow and therefore increase the net present value.

Question 2:

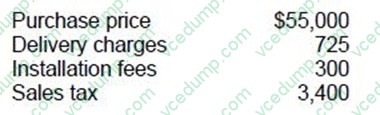

Starr, a self-employed individual, purchased a piece of equipment for use in Starr's business. The costs associated with the acquisition of the equipment were:

What is the depreciable basis of the equipment?

A. $55,000 B. $58,400 C. $59,125 D. $59,425

D. $59,425 Explanation Explanation/Reference:Choice "d" is correct. The rules for depreciable basis in tax are generally the same as the GAAP rules for capitalizing an asset. The depreciable basis is the cost associated with the purchase of the asset and with getting the asset ready for its intended use. Further improvements are also capitalized, and the basis is reduced for any accumulated depreciation. In this case, the cost of obtaining the equipment and getting the equipment ready for its intended use includes all the items shown above, as follows: Choice "a" is incorrect. The costs of delivery charges, installation, and sales tax are all part of the cost of obtaining the asset and getting the asset ready for its intended use. All of these charges are included in the depreciable basis of the equipment. Choice "b" is incorrect. The costs of delivery charges and installation are both part of the cost of obtaining the asset and getting the asset ready for its intended use. These charges are included in the depreciable basis of the equipment. Choice "c" is incorrect. The cost of installation is part of the cost getting the asset ready for its intended use. This charge is included in the depreciable basis of the equipment.

Question 3:

The determination of gross domestic product (GDP) by the expenditure approach would include:

A. Net exports. B. Business profits. C. Compensation to employees. D. A capital consumption allowance.

A. Net exports. Choice "a" is correct. The expenditure approach to computing GDP includes: Consumption Net exports Government expenditures Capital investment Choices "b", "c", and "d" are incorrect, per theabove.

Question 4:

Which of the following is not an external factor that directly affects the competitive environment of the firm?

A. Barriers to market entry. B. Bargaining power of suppliers. C. Political issues. D. Existence of substitute products.

C. Political issues. Choice "c" is correct. Political issues are external factors that affect the overall industry, not simply the competitive environment of the firm. Choices "a", "b", and "d" are incorrect, as all of these factors directly affect the competitive environment of the firm.

Question 5:

Which of the following statements best describes an operating procedure for issuing a new Financial Accounting Standards Board (FASB) statement?

A. The emerging issues task force must approve a discussion memorandum before it is disseminated to the public. B. The exposure draft is modified per public opinion before issuing the discussion memorandum. C. A new statement is issued only after a majority vote by the members of the FASB. D. A new FASB statement can be rescinded by a majority vote of the AICPA membership.

C. A new statement is issued only after a majority vote by the members of the FASB. Choice "c" is correct. A new statement from the FASB is issued only after a majority vote of the members of the FASB. Choice "a" is incorrect. There is no necessity for the EITF to approve a discussion memorandum (presumably the question means a discussion memorandum of the FASB statement itself and not an EITF statement) before it is disseminated to the public. Choice "b" is incorrect. There is no necessity for an exposure draft to be modified per public opinion before issuing the discussion memorandum (a question can be raised here as to "what" discussion memorandum"). Exposure drafts are quite/most often modified before they are issued as FASB statements, but they do not have to be. Whether they are or are not modified is a function of whether the FASB thinks they should be modified, partly due to the public comments that have been received. Choice "d" is incorrect. There is no way to rescind a new FASB statement, although, in reality, a FASB statement can be rescinded by the issuance of a new statement on the same subject. However, even if there was a way to rescind a new FASB statement, it would not be by a majority vote of the AICPA membership, but by a majority vote of the members of the FASB.

Question 6:

If, in a competitive market, a price ceiling is imposed establishing a maximum price below the market equilibrium price, this price ceiling would result in:

A. Shortages because the quantity demanded would exceed the quantity supplied. B. No effect on the quantity supplied or demanded. C. Surpluses because the quantity supplied would exceed the quantity demanded. D. Surpluses because the supply curve would shift to the right.

A. Shortages because the quantity demanded would exceed the quantity supplied. Explanation Explanation/Reference:Choice "a" is correct. Setting a ceiling price below the price dictated by the market (as established by the equilibrium price) would create excess demand and a shortage. Choices "b", "c", and "d" are incorrect, per above Explanation.

Question 7:

Using a 360-day year, what is the opportunity cost to a buyer of not accepting terms 3/10, net 45?

A. 55.67 percent. B. 31.81 percent. C. 15.43 percent. D. 24.00 percent.

B. 31.81 percent. Choice "b" is correct. 31.81% Formula:

Question 8:

Green, CPA, was engaged to audit the financial statements of ABC Co. after its fiscal year had ended. The timing of Green's appointment as auditor and the start of fieldwork made confirmation of accounts receivable by direct communication with the debtors ineffective. However, Green applied other procedures and was satisfied as to the reasonableness of the account balances. Green's auditor's report most likely contained a(an):

A. Unqualified opinion. B. Unqualified opinion with an explanatory paragraph. C. Qualified opinion due to a scope limitation. D. Qualified opinion due to a departure from generally accepted auditing standards.

A. Unqualified opinion. Choice "a" is correct. There is a presumption that the auditor will request the confirmation of accounts receivable during an audit unless accounts receivable are immaterial, the use of confirmations would be ineffective, or the assessed inherent risk is so low that the evidence expected to be provided by analytical procedures or other substantive tests of details would be sufficient. In this example, the confirmation of accounts receivable by direct communication with the debtors would be ineffective. If Green was able to apply alternative audit procedures and was satisfied as to the reasonableness of the account balances, then an unqualified opinion could be issued. Choice "b" is incorrect. Since Green was satisfied as far as the accounts receivable balances, there is no need to add an explanatory paragraph. Choice "c" is incorrect. Since Green was able to perform alternative procedures and was satisfied as far as the reasonableness of the account balances, there is no scope limitation. Choice "d" is incorrect. Since Green was able to perform alternative procedures and was satisfied as far as the reasonableness of the account balances, there is no departure from generally accepted auditing standards.

Question 9:

Doris and Lydia are equal partners in the capital and profits of Agee and Nolan, but are otherwise unrelated. The following information pertains to 300 shares of ABC Corp. stock sold by Lydia to Agee and Nolan:

The amount of long-term capital loss that Lydia realized in 1988 on the sale of this stock was:

A. $5,000 B. $3,000 C. $2,500 D. $0

A. $5,000 Explanation Explanation/Reference:Choice "a" is correct. $5,000 long term capital loss "realized" in 1988 by Lydia. Be careful, and always check the question being asked. In this case, the question is how much of a capital loss Lydia realized in 1988. Choice "b" is incorrect. $3,000 represents the portion of the $5,000 realized loss that would currently be recognized unless there were additional capital transactions resulting in gains. Remember that the deduction for capital losses for an individual is limited to $3,000 each year. Choice "c" is incorrect. $2,500 represents the pre-1986 portion of the $5,000 realized loss that would have given rise to a recognized loss. Pre-1986 law required $2 of net long term loss to give the benefit of $1 of tax deduction. Current law gives a dollar-for-dollar deduction limited to $3,000 in any year. Choice "d" is incorrect. $0 would have been the amount of loss recognized if Lydia owned more than a 50% interest in the partnership. Losses realized on transactions between a partnership and a partner owning more than a 50% interest are not deductible as the parties would be considered related and any realized loss would be disallowed.

Question 10:

In 19X4, Smith, a divorced person, provided over one half the support for his widowed mother, Ruth, and his son, Clay, both of whom are U.S. citizens. During 19X4, Ruth did not live with Smith. She received $9,000 in Social Security benefits. Clay, a 25 year-old full-time graduate student, and his wife lived with Smith. Clay had no income but filed a joint return for 19X4, owing an additional $500 in taxes on his wife's income. How many exemptions was Smith entitled to claim on his 19X4 tax return?

A. 4 B. 3 C. 2 D. 1

C. 2 Choice "c" is correct. Smith is entitled to an exemption for himself. He is also entitled to an exemption for his mother Ruth (qualifying relative). Ruth has $9,000 in Social Security payments during 19X4, but since that is her only income, the Social Security is not taxable, and nontaxable income does not count in calculating whether an exemption can be taken for a dependent. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay's wife because she filed a joint return with Clay. Smith is entitled to two exemptions. Choice "a" is incorrect. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay's wife because she filed a joint return with Clay. Choice "b" is incorrect. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay's wife because she filed a joint return with Clay. Choice "d" is incorrect. Smith is entitled to an exemption for his mother, Ruth. Ruth has $9,000 in Social Security payments during 19X4, but because that is her only income, the Social Security income is not taxable, and nontaxable income does not count in calculating whether an exemption can be taken for a dependent.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.