CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 1231:

Which of the following should be disclosed in a summary of significant accounting policies?

A. Management's intention to maintain or vary the dividend payout ratio. II. Criteria for determining which investments are treated as cash equivalents. III. Composition of the sales order backlog by segment.

B. I only.

C. I and III.

D. II only.

E. II and III. -

Question 1232:

When an accountant examines projected financial statements, the accountant's report should include a separate paragraph that:

A. Describes the limitations on the usefulness of the presentation.

B. Provides an of the differences between an examination and an audit.

C. States that the accountant is responsible for events and circumstances up to one year after the report's date.

D. Disclaims an opinion on whether the assumptions provide a reasonable basis for the projection. -

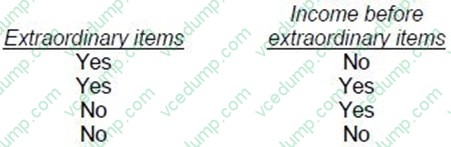

Question 1233:

An extraordinary item should be reported separately on the income statement as a component of income:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 1234:

ABC Industries, a vertically integrated producer and retailer of high end audio visual equipment has mapped out its overall business process as beginning with product development followed by product testing then raw materials purchasing then manufacturing and assembly, and, finally, sales and service. Finance staff at ABC Industries are trying to evaluate the efficiency and the effectiveness of each process and the relationship between each process. This evaluation is often referred to as:

A. Process improvement.

B. Continuous quality improvement.

C. Value chain analysis.

D. Benchmarking. -

Question 1235:

All of the following actions are valid tools that the Federal Reserve Bank uses to control the supply of money, except:

A. Selling government securities.

B. Changing the reserve ratio.

C. Raising or lowering the discount rate.

D. Printing money when the money supply appears low. -

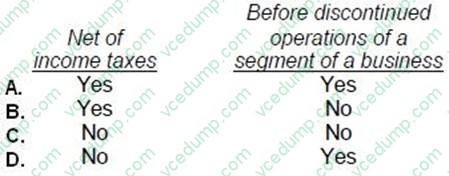

Question 1236:

Earnings per share data should be reported on the income statement for: A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer. B -

Question 1237:

The following data pertain to ABC, Inc., for the year ended December 31, 20X4: What was ABC's rate of return on assets for 20X4?

A. 5%

B. 6%

C. 20%

D. 24% -

Question 1238:

Management accountants are frequently asked to analyze various decision situations including the following.

A. The cost of a special device that is necessary if a special order is accepted. II. The cost proposed annually for the plant service for the grounds at corporate headquarters. III. Joint production costs incurred, to be considered in a sell-at-split versus a process-further decision. IV. The costs associated with alternative uses of plant space, to be considered in a make/buy decision.

B. The cost of obsolete inventory acquired several years ago, to be considered in a keep-versusdisposal decision. The cost described in situation II above is a:

C. Prime cost.

D. Sunk cost.

E. Discretionary cost.

F. Relevant cost. -

Question 1239:

Which of the following would be used on a review engagement?

A. Examination of board minutes.

B. Confirmation of cash and accounts receivable.

C. Comparison of current-year to prior-year account balances.

D. Recalculation of depreciation expense. -

Question 1240:

An entity with a large volume of customer remittances by mail could most likely reduce the risk of employee misappropriation of cash by using:

A. Employee fidelity bonds.

B. Independently prepared mailroom prelists.

C. Daily check summaries.

D. A bank lockbox system.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.