AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

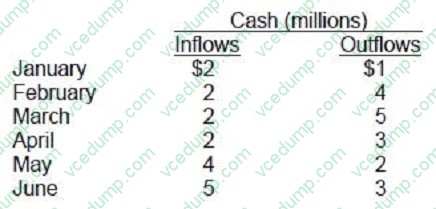

Question 71:

The treasury analyst for ABC Manufacturing has estimated the cash flows for the first half of next year (ignoring any short-term borrowings) as follows: ABC has a line of credit of up to $4 million on which it pays interest monthly at a rate of 1 percent of the amount utilized. ABC is expected to have a cash balance of $2 million on January 1 and no amount utilized on its line of credit. Assuming all cash flows occur at the end of the month, approximately how much will ABC pay in interest during the first half of the year?

A. $61,000 B. $80,000 C. $132,000 D. $240,000

A. $61,000 Explanation Explanation/Reference:Choice "a" is correct. First, determine the amount and timing of cash needs: Comments 1 Given 2 Computed balance, positive cash flows 3 Computed balance, negative cash flows 4 Borrow from LOC 5 Computed balance, negative cash flows + interest 6 Cumulative LOC Balance 7 Computed positive cash flows 8 Computed balance, positive cash flows - interest 9 Immediate pay down of LOC Choices "b", "c", and "d" are incorrect, per the above calculation.

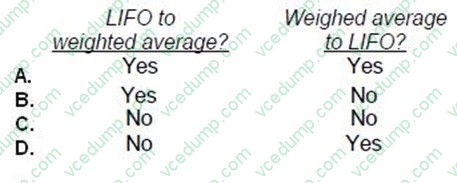

Question 72:

Is the cumulative effect of an inventory pricing change on prior years earnings reported on the financial statements for

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. The cumulative effect of a change in accounting principle is now reported as an adjustment to beginning retained earnings when it is considered practicable to calculate the cumulative effect. When making a change to LIFO, it is generally considered impracticable to calculate the cumulative effect of the change (in most cases, data on the historical LIFO layers in not available). In a change to LIFO, the beginning inventory dollar amount becomes the first LIFO layer. No cumulative effect adjustment is made. The change is accounted for prospectively. A change from LIFO to weighted average, there is no such impracticability. The cumulative effect is computed and the change is handled retrospectively. Choices "a", "c", and "d" are incorrect, per the above Explanation.

Question 73:

A project's net present value, ignoring income tax considerations, is normally affected by the:

A. Proceeds from the sale of the asset to be replaced. B. Carrying amount of the asset to be replaced by the project. C. Amount of annual depreciation on the asset to be replaced. D. Amount of annual depreciation on fixed assets used directly on the project.

A. Proceeds from the sale of the asset to be replaced. Choice "a" is correct. A project's net present value is a function of current and future cash flows, including proceeds from the sale of the old asset. Choice "b" is incorrect. A project's net present value is a function of current and future cash flows. The carrying amount of the asset does not affect cash flows. Choice "c" is incorrect. A project's net present value is a function of current and future cash flows. Depreciation is a noncash item and does not affect cash flows. Choice "d" is incorrect. A project's net present value is a function of current and future cash flows. Depreciation is a noncash item and does not affect cash flows.

Question 74:

A working capital technique that increases the payable float and, therefore, delays the outflow of cash is:

A. Concentration banking. B. A draft. C. A lock-box system. D. The use of a local post office box.

B. A draft. Choice "b" is correct. A draft is a working capital technique that increases the payable float and, therefore, delays the outflow of cash. Each of the three following choices accelerate the flow of cash and/or data: Choice "a" is incorrect. Concentration banking automatically channels funds from every source of the business into a single usable account, thus quickly identifying available funds each day, and moving them to accounts that have funding requirements that day, and investing the remainder in short-term, interest bearing instruments until needed. Choice "c" is incorrect. A lock-box system is simply a central collection location that receives payment checks (generally, the bank where a central checking account is maintained by the firm). Choice "d" is incorrect. The use of a local post office box allows more rapid access to mail than actual delivery to a street address.

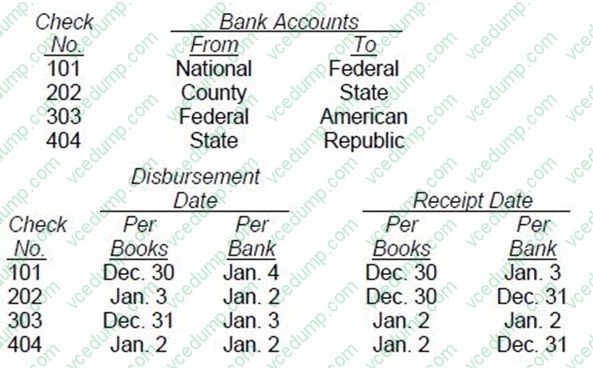

Question 75:

The information below was taken from the bank transfer schedule prepared during the audit of ABC Co.'s financial statements for the year ended December 31, 20X1. Assume all checks are dated and issued on December 30, 20X1.

Which of the following checks illustrate deposits/transfers in transit at December 31, 20X1?

A. #101 and #202. B. #101 and #303. C. #202 and #404. D. #303 and #404.

B. #101 and #303. Choice "b" is correct. A deposit in transit is a disbursement recorded in one accounting period with the receipt occurring in the subsequent period. Assuming all checks were dated and issued on December 30, 20X1, any deposits with a receipt date in 20X2 would indicate a deposit in transit at December 31, 20X1. Checks #101 and #303 both meet this criterion and therefore illustrate deposits/transfers in transit at December 31, 20X1. Choices "a", "c", and "d" are incorrect, based on the above .

Question 76:

In the long run in a competitive market, a maximum or ceiling price set below the equilibrium price will:

A. Cause a surplus to be produced. B. Have no effect on the market. C. Cause a shortage to be created. D. Result in a decrease in price.

C. Cause a shortage to be created. Choice "c" is correct. Setting a ceiling price below the price dictated by market forces (which is the equilibrium price set by the supply and demand curves) would create excess demand for the product (at its reduced price) and, consequently, a shortage. Choice "a" is incorrect. A surplus would be produced if a floor price (under which no supplier could sell) were set above the equilibrium price, because suppliers would supply excess product at the inflated price. Choices "b" and "d" are incorrect, per the above Explanation.

Question 77:

Why would a firm generally choose to finance temporary assets with short-term debt?

A. Matching the maturities of assets and liabilities reduces risk. B. Short-term interest rates have traditionally been more stable than long-term interest rates. C. A firm that borrows heavily long term is more apt to be unable to repay the debt than a firm that borrows heavily short term. D. Financing requirements remain constant.

A. Matching the maturities of assets and liabilities reduces risk. Choice "a" is correct. Matching the maturities of current assets with liabilities as they come due is designed to ensure liquidity and reduce risk of cash shortages. Temporary assets (such as inventories, generally, and seasonal inventories, specifically) might be financed with short term debt such that the earnings from the sales of those temporary assets could be used to liquidate the related obligations as they come due and ensure that cash is available to meet cash flow requirements. Choice "b" is incorrect. Interest rate risks would likely motivate a firm to use longer term financing than short-term financing. Choice "c" is incorrect. Matching cash inflows with cash outflows are more influential in determining a firm's ability to repay debt rather than the length of the obligation. Choice "d" is incorrect. Long-term rather than short-term debt promotes consistent finance charges. The requirements for financing itself are driven by business practice, not by the maturity of financial instruments used.

Question 78:

An accountant may accept an engagement to apply agreed-upon procedures to prospective financial statements provided that:

A. Use of the report is restricted to the specified parties. B. The prospective financial statements are also examined. C. Responsibility for the adequacy of the procedures performed is taken by the accountant. D. Negative assurance is expressed on the prospective financial statements taken as a whole.

A. Use of the report is restricted to the specified parties. Choice "a" is correct. An accountant may accept an engagement to apply agreed-upon procedures to prospective financial statements provided that certain conditions are met, including that the use of the report be restricted to the specified parties. Choice "b" is incorrect. There is no requirement that the prospective financial statements be examined. In fact, the practitioner's report on the application of agreed-upon procedures states that the auditor did not perform an examination. Choice "c" is incorrect. The specified parties must understand that they take responsibility for the sufficiency of the attest procedures. Choice "d" is incorrect. No assurance is expressed in an agreed-upon procedures engagement.

Question 79:

When management's assertion about the effectiveness of a nonissuer's internal control is presented in a representation letter that will not accompany the CPA's report:

A. Use of the report is restricted to management and the board of directors. B. The report should contain a statement of management's assertion. C. The CPA should not accept the engagement. D. The report should include a negative assurance with respect to the effectiveness of the entity's internal control.

B. The report should contain a statement of management's assertion. Choice "b" is correct. When management's assertion does not accompany the CPA's report, the first paragraph of the report should contain a statement of management's assertion. Choice "a" is incorrect. There is no requirement to limit the use of the report, but the report must include a statement of management's assertion. Choice "c" is incorrect. The CPA may accept such an engagement but is required to include management's assertion in the report. Choice "d" is incorrect. Negative assurance is prohibited with respect to a report on the effectiveness of an entity's internal control.

Question 80:

An auditor's plan to examine long-term debt most likely would include steps that require:

A. Comparing the carrying amount of the debt to its year-end market value. B. Correlating interest expense recorded for the period with outstanding debt. C. Verifying the existence of the holders of the debt by direct confirmation. D. Inspecting the accounts payable subsidiary ledger for unrecorded long-term debt.

B. Correlating interest expense recorded for the period with outstanding debt. Choice "b" is correct. An auditor's plan to examine long-term debt most likely would include steps that require correlating interest expense recorded for the period with outstanding debt. This is an analytical procedure that would provide evidence regarding the reasonableness of the interest expense balance. Choice "a" is incorrect. This question was released prior to the issuance of FAS 107, which requires disclosure of the fair values of financial instruments. Accordingly, the auditor now needs to audit the year- end market values of long-term debt. Choice "a" is still not the best answer, however, since the auditor would not need to compare the carrying amount to the year-end market value. (Both values are shown, as FAS 107 does not require that debt securities be written down to (a lower) market value.) Choice "c" is incorrect. Generally the existence of the holders of the debt is not verified. Choice "d" is incorrect. Inspecting the accounts payable subsidiary ledger would be included in the audit of accounts payable, not long-term debt.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.