CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

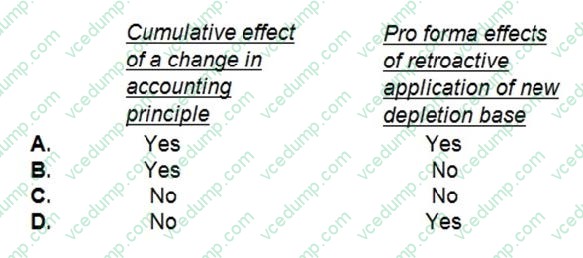

Question 41:

During 1992, ABC Co. increased the estimated quantity of copper recoverable from its mine. ABC uses the units of production depletion method. As a result of the change, which of the following should be reported in ABC's 1992 financial statements?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 42:

ABC, Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments.

?ABC can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling the issue, an average premium of $30 per bond would be received, and the firm must pay floatation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent. ?ABC can sell 8 percent preferred stock at par value, $105 per share. The cost of issuing and selling the preferred stock is expected to be $5 per share. ?ABC' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7 per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and floatation costs are expected to amount to $5 per share. ?ABC expects to have available $100,000 of retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing. ?ABC' preferred capital structure is: Long-term debt 30% Preferred stock 20 Common stock 50

The cost of funds from the sale of common stock for ABC, Inc. is:

A. 7.0 percent.

B. 7.6 percent.

C. 7.4 percent.

D. 7.8 percent. -

Question 43:

An examination of a financial forecast is a professional service that involves:

A. Compiling or assembling a financial forecast that is based on management's assumptions.

B. Limiting the distribution of the accountant's report to management and the board of directors.

C. Assuming responsibility to update management on key events for one year after the report's date.

D. Evaluating the preparation of a financial forecast and the support underlying management's assumptions. -

Question 44:

To establish the existence and ownership of a long-term investment in the common stock of a publicly traded company, an auditor ordinarily performs a security count or:

A. Relies on the client's internal accounting controls if the auditor has reasonable assurance that the control activities are being applied as prescribed.

B. Confirms the number of shares owned that are held by an independent custodian.

C. Determines the market price per share at the balance sheet date from published quotations.

D. Confirms the number of shares owned with the issuing company. -

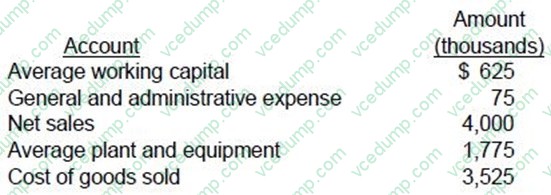

Question 45:

Listed below is selected financial information for the Western Division of the ABC Company for last year.

If ABC treats the Western Division as an investment center for performance measurement purposes, what is the before-tax return on investment for last year?

A. 26.76 percent.

B. 22.54 percent.

C. 19.79 percent.

D. 16.67 percent. -

Question 46:

The amount of inventory that a company would tend to hold in safety stock would increase as the:

A. Cost of carrying inventory decreases.

B. Variability of sales decreases.

C. Costs of running out of stock decreases.

D. Length of time that goods are in transit decreases. -

Question 47:

Which of the following formulas should be used to calculate the economic rate of return on common stock?

A. (Dividends + change in price) divided by beginning price.

B. (Net income - preferred dividend) divided by common shares outstanding.

C. Market price per share divided by earnings per share.

D. Dividends per share divided by market price per share. -

Question 48:

Which of the following control activities is not usually performed in the vouchers payable department?

A. Determining the mathematical accuracy of the vendor's invoice.

B. Having an authorized person approve the voucher.

C. Controlling the mailing of the check and remittance advice.

D. Matching the receiving report with the purchase order. -

Question 49:

Which of the following must be included in a company's summary of significant accounting policies in the notes to the financial statements?

A. Description of current year equity transactions.

B. Summary of long-term debt outstanding.

C. Schedule of fixed assets.

D. Revenue recognition policies. -

Question 50:

If a product has a price elasticity of demand of 2.0, the demand is said to be:

A. Perfectly elastic.

B. Perfectly inelastic.

C. Relatively elastic.

D. Relatively inelastic.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.