AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 521:

What is the underlying concept that supports the immediate recognition of a contingent loss?

A. Substance over form. B. Consistency. C. Matching. D. Conservatism.

D. Conservatism. Choice "d" is correct. Conservatism is a prudent reaction to uncertainty to try to ensure that uncertainty and risks inherent in business situations are adequately considered. Recognition of a contingent loss is the recording of an amount representing uncertainty and risk in a business situation. SFAC 2, SFAS 5 para. 82 Choice "a" is incorrect. The substance over form concept presumes that the transaction form may not dictate the accounting treatment. Choice "b" is incorrect. Consistency is conformity from period to period with unchanging policies and procedures. SFAC 2 Choice "c" is incorrect. The matching principle dictates that expenses be matched with the related revenues generated or the time period in which the expense is incurred and known. SFAS #5 cites matching as the one concept supporting the immediate recognition of a contingent loss, but it is not the primary underlying concept. SFAS 5 para. 76

Question 522:

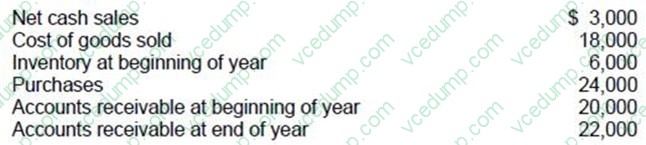

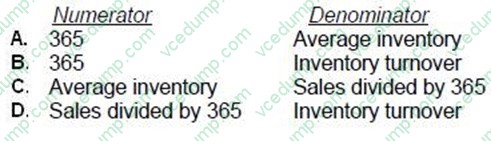

Selected data pertaining to ABC Co. for the calendar year 20X4 is as follows:

ABC would use which of the following to determine the average day's sales in inventory?

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. Average number of days sales in inventory is defined as 365 days per year divided by the inventory turnover. Choice "a" is incorrect. The denominator used to determine average days sales in inventory is inventory turnover. Inventory turnover is cost of goods sold divided by average inventory, not simply average inventory. Choice "c" is incorrect. The days sales in inventory calculation uses the cost of goods sold figure, not the sales figure. Choice "d" is incorrect. The days sales in inventory calculation uses 365 in the numerator, not sales divided by 365.

Question 523:

Which of the following matters is an auditor not required to communicate to those charged with governance?

A. Significant adjustments arising from the audit that were recorded by management. B. The basis for the auditor's conclusions about the reasonableness of management's sensitive accounting estimates. C. The level of responsibility assumed by the auditor under generally accepted auditing standards. D. The degree of reliance the auditor placed on the management representation letter.

D. The degree of reliance the auditor placed on the management representation letter. Choice "d" is correct. The auditor is not required to communicate to those charged with governance the degree of reliance placed on the management representation letter. Choice "a" is incorrect. Unless all those charged with governance are also involved with managing the entity, the auditor should inform those charged with governance about adjustments arising from the audit, regardless of whether or not management recorded them. Choice "b" is incorrect. The auditor should communicate qualitative aspects of the process used by management in formulating sensitive accounting estimates, which would likely include discussion of the basis for the auditor's conclusions regarding the reasonableness of those estimates. Choice "c" is incorrect. The auditor should communicate the level of responsibility that he/she is assuming under GAAS.

Question 524:

In a general partnership, the authorization of all partners is required for an individual partner to bind the partnership in a business transaction to:

A. Purchase inventory. B. Hire employees. C. Sell goodwill. D. Sign advertising contracts.

C. Sell goodwill. Choice "c" is correct. All partners have apparent authority to enter into transactions apparently within the regular scope of the partnership business. No such authority exists, however, for transactions outside the regular scope of business. The sale of a business's goodwill is extraordinary and is outside the ordinary scope of business. Thus, a partner must get authorization from all other partners to make the sale. Choice "a" is incorrect. All partners have apparent authority to enter into transactions apparently within the regular scope of the partnership business. Purchasing inventory is within the regular scope of business, so a partner need not get permission from the other partners to bind the partnership. Choice "b" is incorrect. All partners have apparent authority to enter into transactions apparently within the regular scope of the partnership business. Hiring employees is within the regular scope of a business, so a partner need not get permission from the other partners to bind the partnership. Choice "d" is incorrect. All partners have apparent authority to enter into transactions apparently within the regular scope of the partnership business. Entering into advertising contracts is within the regular course of business, and so a partner need not get permission from the other partners to bind the partnership.

Question 525:

In using the work of a specialist, an auditor of a nonissuer may refer to the specialist in the auditor's report if, as a result of the specialist's findings, the auditor:

A. Becomes aware of conditions causing substantial doubt about the entity's ability to continue as a going concern. B. Desires to disclose the specialist's findings, which imply that a more thorough audit was performed. C. Is able to corroborate another specialist's earlier findings that were consistent with management's representations. D. Discovers significant deficiencies in the design of the entity's internal control that management does not correct.

A. Becomes aware of conditions causing substantial doubt about the entity's ability to continue as a going concern. Choice "a" is correct. The auditor may, as a result of the report or findings of the specialist, decide to add explanatory language to the auditor's standard report or depart from an unqualified opinion. Reference to and identification of the specialist may be made in the auditor's report if the auditor believes such reference will facilitate an understanding of the reason for the explanatory paragraph or the departure from the unqualified opinion. Choice "b" is incorrect. The auditor should not refer to the work or findings of the specialist unless the specialist's work results in a change to the auditor's report. Choice "c" is incorrect. The auditor should not refer to the work or findings of the specialist unless the specialist's work results in a change to the auditor's report. Choice "d" is incorrect. The identification of significant deficiencies in the design of the client's internal control would not result in a change to the auditor's report. The auditor should not refer to the work or findings of the specialist unless the specialist's work results in a change to the auditor's report.

Question 526:

Utility companies can generally price their product, a good that establishes a comfortable life-style (i.e., electricity, gas for home heating) based on the fact that the demand:

A. Is relatively elastic. B. Is perfectly elastic. C. Is relatively inelastic. D. Is perfectly inelastic.

C. Is relatively inelastic. Choice "c" is correct. Goods that are important for a comfortable life-style would be relatively price insensitive (i.e., inelastic). For example, demand for electricity would only decrease if there were an enormous increase in price (people might then use other forms of energy - such as solar). Only goods that are absolute necessities (a theoretical example is water) have perfectly inelastic demand curves. That is, no matter what price is charged, people will still buy the product because they need it to stay alive. Choices "a", "b", and "d" are incorrect, per for choice "c" above.

Question 527:

The method that divides a project's annual after-tax net income by the average investment cost to measure the estimated performance of a capital investment is the:

A. Internal rate of return method. B. Accounting rate of return method. C. Payback method. D. Net present value method.

B. Accounting rate of return method. Explanation Explanation/Reference: Choice "b" is correct. Accounting rate of return divides annual after-tax net income by average investment amount. Choices "a", "c", and "d" are incorrect. IRR, NPV and payback all use cash flows, not net income.

Question 528:

Heather, Erika, and Shelby are members in ABC LLC. Heather works 40 hours per week and Erika and Shelby work 20 hours per week. Heather contributed $30,000 to the LLC and Erika and Shelby contributed $60,000 each. Erika and

Shelby have each originated 45% of the LLC's business and Heather has originated the other 10%.

If ABC were a general partnership, who controls management?

A. Heather, because she works the most. B. Erika and Shelby equally because they contributed the most. C. Heather, Erika, and Shelby equally because of state law. D. Erika and Shelby, because they originate most of the work.

C. Heather, Erika, and Shelby equally because of state law. Choice "c" is correct. Rule: Absent an agreement to the contrary, partners have equal management authority. Choices "a", "b", and "d" are incorrect, per the above rule.

Question 529:

When auditing prepaid insurance, an auditor discovers that the original insurance policy on plant equipment is not available for inspection. The policy's absence most likely indicates the possibility of a (an):

A. Insurance premium due but not recorded. B. Deficiency in the coinsurance provision. C. Lien on the plant equipment. D. Understatement of insurance expense.

C. Lien on the plant equipment. Choice "c" is correct. If an auditor discovers that the original insurance policy on plant equipment is not available for inspection, this most likely indicates that there is a lien on the plant equipment, since the original policy would likely be in the possession of the lien holder. Choices "a", "b", and "d" are incorrect. The absence of the original policy does not necessarily indicate that there is an insurance premium due but not recorded, that there is a deficiency in the coinsurance provision, or that insurance expense is understated, since the policy must be reviewed before any of these conclusions can be drawn.

Question 530:

Which of the following statements would least likely appear in an auditor's engagement letter?

A. Fees for our services are based on our regular per diem rates, plus travel and other out-of-pocket expenses. B. During the course of our audit we may observe opportunities for economy in, or improved controls over, your operations. C. Our engagement is subject to the risk that material errors or fraud, including defalcations, if they exist, will not be detected. D. After performing our preliminary analytical procedures we will discuss with you the other procedures we consider necessary to complete the engagement.

D. After performing our preliminary analytical procedures we will discuss with you the other procedures we consider necessary to complete the engagement. Choice "d" is correct. The auditor does not consult with the client about audit procedures that will be performed. Choice "a" is incorrect. Since the engagement letter serves as a contract between the auditor and client, fee arrangements are typically disclosed in the letter. Choice "b" is incorrect. A discussion regarding possible auditor suggestions is appropriate for inclusion in an engagement letter. Choice "c" is incorrect. The fact that audit risk exists and that an audit only provides reasonable assurance of the detection of errors and fraud is typically disclosed in an engagement letter.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.