AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

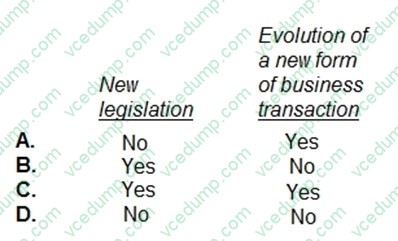

Question 531:

According to the profession's ethical standards, which of the following events may justify a departure from a Statement of Financial Accounting Standards?

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. Yes - Yes. Rule 203 of the code of professional conduct of the AICPA states that if the financial statements or data contain a GAAP departure, the departure may be justified if the CPA can demonstrate that due to unusual circumstances, such as new legislation or the evolution of a new form of business transaction, the FS would otherwise be misleading. Under these circumstances, the auditor's report should describe the departure, its approximate effects, if practicable, and the reasons why compliance with the generally accepted principle would result in a misleading statement. Choices "a", "b", and "d" are incorrect, per the above explanation.

Question 532:

Jones, Smith, and Bay wanted to form a company called ABC Co. but were unsure about which type of entity would be most beneficial based on their concerns. They all desired the opportunity to make taxfree contributions and distributions where appropriate. They wanted earnings to accumulate tax-free. They did not want to be subject to personal holding tax and did not want double taxation of income. Bay was going to be the only individual giving management advice to the company and wanted to be a member of ABC through his current company, XYZ, Inc. Which of the following would be the most appropriate business structure to meet all of their concerns?

A. Proprietorship. B. S corporation. C. C corporation. D. Limited liability partnership.

D. Limited liability partnership. Choice "d" is correct. An LLP does not pay taxes on its earnings. Instead, the profits and losses flow through to the partners as in a general partnership. The LLP files an informational tax return like that of a general partnership. The partners may agree to have the entity managed by one or more of the partners. A partner may be another entity. Choice "a" is incorrect. A proprietorship by definition has only one owner, not three owners. Choice "b" is incorrect. While an S corporation allows for the same treatment of its earnings and distributions as in the facts, it is prohibited from having another company as an owner. Choice "c" is incorrect. A C corporation pays its own taxes on its earnings, and any distributions to its shareholders are again taxed at the shareholder level (known as "double taxation").

Question 533:

An auditor who discovers that a client's employees have paid small bribes to public officials most likely would withdraw from the engagement if the:

A. Client receives financial assistance from a federal government agency. B. Audit evidence that is necessary to prove that the illegal acts were committed does not exist. C. Employees' actions affect the auditor's ability to rely on management's representations. D. Notes to the financial statements fail to disclose the employees' actions.

C. Employees' actions affect the auditor's ability to rely on management's representations. Choice "c" is correct. When an auditor cannot rely on management's representations, he or she should withdraw from the engagement. Choice "a" is incorrect. As long as the client takes appropriate remedial action, the auditor would not need to withdraw from the engagement simply because the client receives federal financial assistance. However, the auditor would be subject to a variety of reporting requirements related to this discovery. Choice "b" is incorrect. If there is no evidence that an illegal act was committed, management may be unable to take remedial action against the related employees. As long as the illegal act is immaterial and the auditor is satisfied that management's response is appropriate in the circumstances, there would be no reason for the auditor to withdraw. Choice "d" is incorrect. The auditor should evaluate the adequacy of disclosure in the financial statements with respect to the potential effects of an illegal act. If the auditor concludes that disclosure is inadequate, he or she should express a qualified or adverse opinion, but would not necessarily need to withdraw from the engagement (unless the client refused to accept the modified report).

Question 534:

Which of the following would lead to the most inflation?

A. Both aggregate demand and aggregate supply increase. B. Both aggregate demand and aggregate supply decrease. C. Aggregate demand increases and aggregate supply decreases. D. Aggregate demand decreases and aggregate supply increases.

C. Aggregate demand increases and aggregate supply decreases. Choice "c" is correct. Choice "c" contains both demand-pull inflation (when the aggregate demand curve shifts right) and cost-push inflation (when the aggregate supply curve shifts left). An increase in aggregate demand causes output to rise and the price level to rise. A decrease in aggregate supply causes output to fall and the price level to rise. Thus, an increase in aggregate demand and a decrease in aggregate supply is the most inflationary. Choice "a" is incorrect. If aggregate supply increases, the price level will fall (reducing inflation). Choice "b" is incorrect. If aggregate demand decreases, the price level will fall (reducing inflation). Choice "d" is incorrect per above Explanation.

Question 535:

Which of the following is subject to the Uniform Capitalization Rules of Code Sec. 263A?

A. Editorial costs incurred by a freelance writer. B. Research and experimental expenditures. C. Mine development and exploration costs. D. Warehousing costs incurred by a manufacturing company with $12 million in annual gross receipts.

D. Warehousing costs incurred by a manufacturing company with $12 million in annual gross receipts. Choice "d" is correct. Uniform capitalization rules apply to the following: (1) real or tangible personal property produced by the taxpayer for use in his or her trade or business; (2) real or tangible personal property produced by the taxpayer for sale to his or her customers; and (3) real or tangible personal property acquired by the taxpayer for resale, provided the taxpayer's annual average gross receipts for the preceding three years exceeds $10,000,000. Warehousing costs incurred by a manufacturing company (making inventory for sale to its customers) are subject to the Uniform Capitalization Rules. Further, they are the only item on the list that is real or tangible personal property. In this case, the inventory is not acquired for resale (it is produced by the taxpayer for sale to his or her customers), so the fact that the annual sales are $12,000,000 does not matter in this case. The sales could have been less than $10,000,000 annually, and the Uniform Capitalization Rules would still have applied. Choices "a", "b", and "c" are incorrect, based on the above discussion.

Question 536:

Which of the following statements is not correct about materiality?

A. The concept of materiality recognizes that some matters are important for fair presentation of financial statements in conformity with GAAP, while other matters are not important. B. An auditor considers materiality for planning purposes in terms of the largest aggregate level of misstatements that could be material to any one of the financial statements. C. Materiality judgments are made in light of surrounding circumstances and necessarily involve both quantitative and qualitative judgments. D. An auditor's consideration of materiality is influenced by the auditor's perception of the needs of a reasonable person who will rely on the financial statements.

B. An auditor considers materiality for planning purposes in terms of the largest aggregate level of misstatements that could be material to any one of the financial statements. Choice "b" is correct. Materiality levels include an overall level for each statement; however, because the statements are interrelated, and for reasons of efficiency, the auditor ordinarily considers materiality for planning purposes in terms of the smallest aggregate level of misstatements that could be considered material to any one of the financial statements. Choice "a" is incorrect. The concept of materiality recognizes that some matters, either individually or in the aggregate, are important for the fair presentation of financial statements in conformity with GAAP, while other matters are not important. Choice "c" is incorrect. Materiality judgments are made in light of the surrounding circumstances and necessarily involve both quantitative and qualitative considerations. Choice "d" is incorrect. The auditor's consideration of materiality is influenced by his or her perception of the needs of a reasonable person relying on the financial statements.

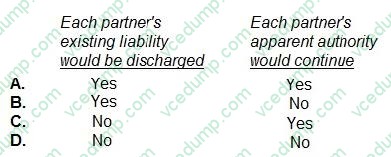

Question 537:

The partners of College Assoc., a general partnership, decided to dissolve the partnership and agreed that none of the partners would continue to use the partnership name. Under the Revised Uniform Partnership Act, which of the following events will occur on dissolution of the partnership?

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. "No - Yes." Rule: Upon the dissolution of the partnership, each of the partners continues to have liability for partnership debts. Upon dissolution of the partnership each of the partners will continue to have apparent authority. The apparent authority of a partner can only be negated upon proper notice to third parties. Choices "a", "b", and "d" are incorrect, per the above rule.

Question 538:

At December 31, 20X2, ABC Co. had the following balances in selected asset accounts:

ABC also had current liabilities of $1,000 at December 31, 20X2, and net credit sales of $7,200 for the year then ended. What was the average number of days to collect ABC's accounts receivable during 20X2?

A. 30.4 B. 40.6 C. 50.7 D. 60.8

C. 50.7 Choice "c" is correct. The average number of days to collect accounts receivable is calculated by dividing 365 days by the accounts receivable turnover. Accounts receivable turnover is net credit sales divided by the average accounts receivable: Choice "a" is incorrect. The denominator should be net credit sales ($7,200) divided by average receivables $1,000), or 7.2, not 12. Choice "b" is incorrect. The average receivable balance is $1,000, not $800. The right-hand column shows the increase over 20X1, so the 20X1 receivable balance was $1,200 - $400, or $800. Since the 20X2 receivable balance was given as $1,200, the average receivable balance is $1,000. Choice "d" is incorrect. Average inventory ($1,000), not ending inventory ($1,200), should be used.

Question 539:

Which one of the following statements concerning cash discounts is correct?

A. The cost of not taking a 2/10, net 30 cash discount is usually less than the prime rate. B. With trade terms of 2/15, net 60, if the discount is not taken, the buyer receives 45 days of free credit. C. The cost of not taking the discount is higher for terms of 2/10, net 60 than for 2/10, net 30. D. The cost of not taking a cash discount is generally higher than the cost of a bank loan.

D. The cost of not taking a cash discount is generally higher than the cost of a bank loan. Choice "d" is correct. The cost of not taking a cash discount is generally higher than the cost of a bank loan. Choice "a" is incorrect. The cost of not taking a 2/10, net 30 cash discount is usually more than the prime rate. Choice "b" is incorrect. With trade terms of 2/15, net 60, if the discount is not taken, the buyer receives 60 (not 45) days of free credit. Choice "c" is incorrect. The cost of not taking the discount is lower (not higher) for terms of 2/10, net 60 than for 2/10, net 30.

Question 540:

In 1992, Anchor, Chain, and Hook created ACH Associates, a general partnership. The partners orally agreed that they would work full time for the partnership and would distribute profits based on their capital contributions. Anchor

contributed $5,000; Chain $10,000; and Hook $15,000. For the year ended December 31, 1993, ACH Associates had profits of $60,000 that were distributed to the partners. During 1994, ACH Associates was operating at a loss. In

September 1994, the partnership dissolved.

In October 1994, Hook contracted in writing with Ace Automobile Co. to purchase a car for the partnership. Hook had previously purchased cars from Ace Automobile Co. for use by ACH Associates partners. ACH Associates did not honor the

contract with Ace Automobile Co. and Ace Automobile Co. sued the partnership and the individual partners.

Determine whether (A) or (B) is correct. Select the answer that corresponds to the correct statement.

A. ACH Associates and Hook would be the only parties liable to pay any judgment recovered by Ace Automobile Co. B. Anchor, Chain, and Hook would be jointly and severally liable to pay any judgment recovered by Ace Automobile Co.

B. Anchor, Chain, and Hook would be jointly and severally liable to pay any judgment recovered by Ace Automobile Co. Choice "b" is correct. Since Ace brought suit against both the partnership and the individual partners, if judgment is rendered against the partnership, all partners could be held jointly and severally liable.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.