AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 511:

Which of the following is a conceptual difference between the attestation standards and generally accepted auditing standards?

A. The attestation standards provide a framework for the attest function beyond historical financial statements. B. The requirement that the practitioner be independent in mental attitude is omitted from the attestation standards. C. The attestation standards do not permit an attest engagement to be part of a business acquisition study or a feasibility study. D. None of the standards of fieldwork in generally accepted auditing standards are included in the attestation standards.

A. The attestation standards provide a framework for the attest function beyond historical financial statements. Choice "a" is correct. Attestation standards provide a framework for the attest function beyond historical financial statements. Choice "b" is incorrect. The independence standard is almost the same for both attest engagements and audits. Choice "c" is incorrect. An attest engagement may be part of a larger engagement (such as a business acquisition study or a feasibility study). Choice "d" is incorrect. Attestation standards include two of the three GAAS fieldwork standards: planning/ supervision and evidence. They do not include the internal control standard.

Question 512:

ABC Corp. declared a 7% stock dividend on its common stock. The dividend:

A. Must be registered with the SEC pursuant to the Securities Act of 1933. B. Is includable in the gross income of the recipient taxpayers in the year of receipt. C. Has no effect on ABC's earnings and profits for federal income tax purposes. D. Requires a vote of ABC's stockholders.

C. Has no effect on ABC's earnings and profits for federal income tax purposes. Choice "c" is correct. A stock dividend means that the corporation issues its existing shareholders more stock. In essence, the corporation is merely diluting the proportional ownership interest of existing shares. This has no effect on the corporation's earnings and profits for federal income tax purposes. Choice "a" is incorrect. There is no requirement that stock dividends be registered with the SEC because no "sale" is involved. Choice "b" is incorrect. The receipt of a stock dividend is not the recognition of income. It merely divides the stockholders' current ownership interests into more pieces; it does not increase proportional ownership interest in the corporation. Choice "d" is incorrect. The issuance of dividends, including stock dividends, is at the directors' discretion; shareholders do not vote on dividends.

Question 513:

An auditor most likely would issue a disclaimer of opinion because of: A. Inadequate disclosure of material information.

B. The omission of the statement of cash flows.

C. A material departure from generally accepted accounting principles.

D. Management's refusal to furnish written representations.

Correct Answer. D

D Choice "d" is correct. Management's refusal to furnish written representations is a significant client imposed restriction on the scope of an audit, ordinarily warranting a disclaimer of opinion. Choice "a" is incorrect. Inadequate disclosure would result in a qualified or adverse opinion. Choice "b" is incorrect. A qualified report would be appropriate when a "statement of cash flows" is omitted and the scope of the audit is not restricted. Choice "c" is incorrect. A departure from GAAP would result in either a qualified or adverse opinion, depending on materiality.

Question 514:

An auditor was unable to obtain audited financial statements or other evidence supporting an entity's investment in a foreign subsidiary. Between which of the following opinions should the entity's auditor choose?

A. Adverse and unqualified with an explanatory paragraph added. B. Disclaimer and unqualified with an explanatory paragraph added. C. Qualified and adverse. D. Qualified and disclaimer.

D. Qualified and disclaimer. Choice "d" is correct. When an auditor is unable to obtain audited financial statements or other evidence supporting an entity's investment in a subsidiary (foreign or domestic), the auditor should issue a qualified or disclaimer of opinion depending on the materiality of the investment in the subsidiary. Choices "a", "b", and "c" are incorrect. An adverse opinion is only issued when the FS are not presented fairly in conformity with GAAP, and an unqualified opinion with an explanatory paragraph is not appropriate for a scope limitation.

Question 515:

Which best describes the documentation completion date?

A. Forty-five days from the report release date, based on PCAOB standards. B. Sixty days from the report release date, based on PCAOB standards. C. Seven years from the report release date, based on auditing standards. D. Five years from the report release date, based on auditing standards.

A. Forty-five days from the report release date, based on PCAOB standards. Choice "a" is correct. According to PCAOB standards, the documentation completion date is forty-five days following the report release date. Choice "b" is incorrect. According to auditing standards, the documentation completion date is sixty days following the report release date. Choices "c" and "d" are incorrect. Seven years and five years refer to the required retention period under PCAOB standards and auditing standards, respectively.

Question 516:

Before applying principal substantive tests to the details of accounts at an interim date prior to the balance sheet date, an auditor should:

A. Assess control risk at a low level for the assertions embodied in the accounts selected for interim testing. B. Determine that the accounts selected for interim testing are not material to the financial statements taken as a whole. C. Consider whether the amounts of the year-end balances selected for interim testing are reasonably predictable. D. Obtain written representations from management that all financial records and related data will be made available.

C. Consider whether the amounts of the year-end balances selected for interim testing are reasonably predictable. Choice "c" is correct. Before performing substantive tests at an interim date, an auditor should consider whether the amounts of the year-end balances selected for interim testing are reasonably predictable with respect to amount, relative significance and composition. Choice "a" is incorrect. It is not necessary for control risk to be assessed at a low level for the assertions relating to the accounts that will be substantively tested at an interim date. It may simply be more efficient to perform a substantive audit. As long as the balances tested at interim are reasonably predictable with respect to amount, relative significance and composition, the account may be tested at interim. Choice "b" is incorrect. Material account balances, such as accounts receivable and inventory, are commonly tested at an interim date. Choice "d" is incorrect. The written representation letter will not be obtained until after year-end.

Question 517:

The scope of audits of recipients of federal financial assistance in accordance with federal audit regulations varies. Which of the following elements do these audits have in common?

A. The auditor is required to disclose all situations and transactions that could be indicative of fraud, abuse, and illegal acts to the federal inspector general. B. The materiality levels are higher and are determined by the government entities that provide the federal financial assistance to the recipients. C. The auditor is required to document an understanding of internal control established to ensure compliance with the applicable laws and regulations. D. The accounts should be 100% verified by substantive tests because certain statistical sampling applications are not permitted.

C. The auditor is required to document an understanding of internal control established to ensure compliance with the applicable laws and regulations. Choice "c" is correct. Auditors engaged to perform audits of federal financial assistance (generally under the provisions of the Single Audit Act) must perform procedures to obtain an understanding of internal control pertaining to compliance, and should document this understanding of internal control. Choice "a" is incorrect. The auditor is required to disclose actual instances of fraud and illegal acts, not all situations that could be indicative of fraud, abuse, or illegal acts. Choice "b" is incorrect. Materiality levels of organizations receiving federal financial assistance are set by the auditor, not the government. Materiality levels depend upon auditor judgment and will not fall or rise purely as a result of federal participation. Choice "d" is incorrect. Statistical sampling applications are permitted, and 100% verification of accounts is not required.

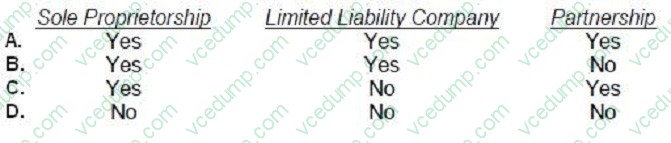

Question 518:

Which of the following forms of business can be formed with only one individual owning the business?

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. A sole proprietorship and (in most states) a limited liability company can be formed with only one owner. A partnership requires two or more partners. Choices "a", "c", and "d" are incorrect per the explanation above.

Question 519:

ABC, Inc. is a multidivisional corporation, which has both intersegment sales and sales to unaffiliated customers. ABC should report segment financial information for each division meeting which of the following criteria?

A. Segment operating profit or loss is 10% or more of consolidated profit or loss. B. Segment operating profit or loss is 10% or more of combined operating profit or loss of all company segments. C. Segment revenue is 10% or more of combined revenue of all the company segments. D. Segment revenue is 10% or more of consolidated revenue.

C. Segment revenue is 10% or more of combined revenue of all the company segments. Choice "c" is correct. Segment revenue is 10% or more of combined revenue of all the company segments. Rule: To be significant enough to report on, a segment must be at least 10% of: 1. Combined revenues (whether intersegment or affiliated customers) or 2. Operating profit (of all segments not having an operating loss), or 3. Identifiable assets. Choice "a" is incorrect. Rule is 10% of "operating profit," not "consolidated profit." Choice "b" is incorrect. Segments with "operating losses" are not combined with those having "operating profits" in determining a segment. Choice "d" is incorrect. "Consolidated revenue" would not include "intersegment revenue." Rule is "combined revenue," not "consolidated revenue."

Question 520:

A firm can best delay disbursements through the use of:

A. A centralized disbursement function. B. Drafts. C. Factoring. D. Trade discounts.

B. Drafts. Choice "b" is correct. Paying by means of a draft (or check) allows the firm to take advantage of the float period. This delays cash disbursements. Choice "a" is incorrect. A centralized disbursement function will not necessarily delay cash disbursements. Choice "c" is incorrect. Factoring is the sale of accounts receivable to a factor. This has no effect on cash disbursements. Choice "d" is incorrect. Trade discounts are discounts on account receivable and do not impact cash disbursements.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.