CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 541:

Smith was an officer of CCC Corp. As an officer, the business judgment rule applies to Smith in which of the following ways?

A. Because Smith is not a director, the rule does not apply.

B. If Smith makes, in good faith, a serious but honest mistake in judgment, Smith is generally not liable to CCC for damages caused.

C. If Smith makes, in good faith, a serious but honest mistake in judgment, Smith is generally liable to CCC for damages caused, but CCC may elect to reimburse Smith for any damages Smith paid.

D. If Smith makes, in good faith, a serious but honest mistake in judgment, Smith is generally liable to CCC for damages caused, and CCC is prohibited from reimbursing Smith for any damages Smith paid. -

Question 542:

The GAO standards of reporting for governmental financial audits incorporate the AICPA standards of reporting and prescribe supplemental standards to satisfy the unique needs of governmental audits. Which of the following is a supplemental reporting standard for governmental financial audits?

A. Auditors should report the scope of their testing of compliance with laws and regulations and of internal controls.

B. Material indications of illegal acts should be reported in a document distributed only to the entity's senior officials.

C. All changes in the audit program from the prior year should be reported to the entity's audit committee.

D. Any privileged or confidential information discovered should be reported to the organization that arranged for the audit. -

Question 543:

An engagement to express an opinion on the internal control of a nonissuer will generally:

A. Require procedures that duplicate those already applied in assessing control risk during a financial statement audit.

B. Increase the reliability of the financial statements that have already been audited.

C. Be more extensive in scope than the assessment of control risk made during a financial statement audit.

D. Be more limited in scope than the assessment of control risk made during a financial statement audit. -

Question 544:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

In 1992, Joan received an acre of land as an inter-vivos gift from her grandfather. At the time of the gift, the land had a fair market value of $50,000. The grandfather's adjusted basis was $60,000. Joan sold the land in 1994 to an unrelated

third party for $56,000.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000 -

Question 545:

Which of the following statements is true regarding the risk assessment component of internal control?

A. An auditor evaluates an entity's risk assessment because it is a component of overall audit risk in a financial statement audit.

B. An auditor's evaluation of an entity's risk assessment may not be applicable to the audit of every entity.

C. An auditor evaluates an entity's risk assessment to understand how management addresses risks relevant to financial reporting.

D. An auditor need not consider an entity's risk assessment because he or she is primarily concerned with audit risk in a financial statement audit. -

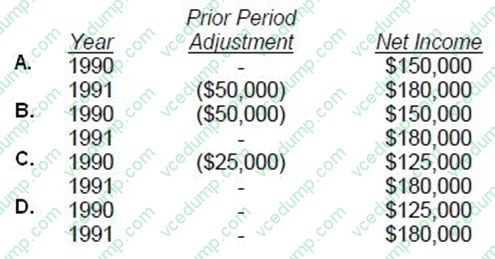

Question 546:

While preparing its 1991 financial statements, ABC Corp. discovered computational errors in its 1990 and 1989 depreciation expense. These errors resulted in overstatement of each year's income by $25,000, net of income taxes. The following amounts were reported in the previously issued financial statements:

ABC's 1991 net income is correctly reported at $180,000. Which of the following amounts should be reported as prior period adjustments and net income in ABC's 1991 and 1990 comparative financial statements?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 547:

The element of the audit planning process most likely to be agreed upon with the client before implementation of the audit strategy is the determination of the:

A. Evidence to be gathered to provide a sufficient basis for the auditor's opinion.

B. Procedures to be undertaken to discover litigation, claims, and assessments.

C. Pending legal matters to be included in the inquiry of the client's attorney.

D. Timing of inventory observation procedures to be performed. -

Question 548:

In considering materiality for planning purposes, an auditor believes that misstatements aggregating $10,000 would have a material effect on an entity's income statement, but that misstatements would have to aggregate $20,000 to materially affect the balance sheet. Ordinarily, it would be appropriate to design auditing procedures that would be expected to detect misstatements that aggregate:

A. $10,000

B. $15,000

C. $20,000

D. $30,000 -

Question 549:

An auditor's communication of internal control related matters noted in an audit usually should be addressed to:

A. Management and those charged with governance.

B. The director of internal auditing.

C. The chief financial officer.

D. The chief accounting officer. -

Question 550:

In planning an audit of a new client, an auditor most likely would consider the methods used to process accounting information because such methods:

A. Influence the design of internal control.

B. Affect the auditor's preliminary judgment about materiality levels.

C. Assist in evaluating the planned audit objectives.

D. Determine the auditor's acceptable level of audit risk.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.