AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 121:

Which of the following is an engagement attribute for an audit of an entity that processes most of its financial data in electronic form without any paper documentation?

A. Discrete phases of planning, interim, and year-end fieldwork. B. Increased effort to search for evidence of management fraud. C. Performance of audit tests on a continuous basis. D. Increased emphasis on the completeness assertion.

C. Performance of audit tests on a continuous basis. Choice "c" is correct. Continuous performance of audit tests is required when financial data is processed electronically, without provision of paper documentation, to ensure that controls are operating effectively throughout the period under audit. Choice "a" is incorrect. Discrete phases of planning, interim, and year-end fieldwork are not effective when there is no audit trail, because no evidence is then available to support the operation of the controls or the accuracy of the financial records for periods when the auditor was not present to conduct tests. Choice "b" is incorrect. Consideration of the risk of management fraud is required in all audits, regardless of the method used to process financial data or the adequacy of the paper documentation provided. Choice "d" is incorrect. The completeness assertion must be tested in all audit engagements, regardless of the method used to process financial data or the adequacy of the paper documentation provided.

Question 122:

Which of the following is not correct about the purchasing power parity theory of explaining changes in exchange rates?

A. Purchasing power of a common currency in different economies for similar products will remain the same. B. Inflationary forces on foreign and domestic currencies will cause the exchange rates to automatically adjust to ensure that a common currency will have identical or similar purchasing power in each economy for similar goods. C. Interest rates include a premium or discount that ensures purchasing power parity. D. The purchasing power parity theory is presented in both absolute and relative form.

C. Interest rates include a premium or discount that ensures purchasing power parity. Choice "c" is correct. The purchasing power parity theory holds that inflation will cause exchange rates to automatically adjust to ensure that an equal amount of a common currency will purchase similar goods in separate economies. The International Fischer effect considers the premium or discount on interest rates as an indicator of inflation. Choice "a" is incorrect. The basic idea underlying the purchasing power parity theory is that the purchasing power of a common currency in different economies for similar products will remain the same and that inflation in any particular economy will cause exchange rates to adjust until parity is consistently achieved. Choice "b" is incorrect. The purchasing power parity theory holds that inflationary forces on foreign and domestic currencies will cause the exchange rates to automatically adjust to ensure that a common currency will have identical or similar purchasing power in each economy for similar goods. Choice "d" is incorrect. The purchasing power parity theory is presented as both an absolute theory of parity determination regardless of market imperfections and as a relative concept that considers market imperfections.

Question 123:

Tracing shipping documents to prenumbered sales invoices provides evidence that:

A. No duplicate shipments or billings occurred. B. Shipments to customers were properly invoiced. C. All goods ordered by customers were shipped. D. All prenumbered sales invoices were accounted for.

B. Shipments to customers were properly invoiced. Choice "b" is correct. Tracing from shipping documents (source documents) to sales invoices provides evidence that shipments to customers are properly invoiced. Choice "a" is incorrect. Tracing shipping documents to sales invoices wouldn't necessarily identify duplicate shipments or billings. Duplicate shipments or billings could be identified by accounting for prenumbered shipping documents and sales invoices. Choice "c" is incorrect. The auditor would compare the signed purchase order to shipping documents to determine if all goods ordered by the customer were shipped. Choice "d" is incorrect. To determine that all prenumbered sales invoices were accounted for, an auditor would review the consecutive numbering of invoices and then trace from the sales invoices into the sales journal.

Question 124:

ABC Corp.'s comprehensive insurance policy allows its assets to be replaced at current value. The policy has a $50,000 deductible clause. One of ABC's waterfront warehouses was destroyed in a winter storm. Such storms occur approximately every four years. ABC incurred $20,000 of costs in dismantling the warehouse and plans to replace it. The tax rate is 30%. The following data relate to the warehouse:

Current carrying amount $ 300,000 Replacement cost 1,100,000

What amount of gain should ABC report as a separate component of income before extraordinary items?

A. $1,030,000 B. $780,000 C. $730,000 D. $0

C. $730,000 Choice "c" is correct. $730,000 gain reported as a separate component of income before extraordinary items.

Question 125:

Considering the SCOR Model of supply chain operations, which of the following key management processes does collecting and processing vendor payments fall into?

A. Plan. B. Source. C. Make. D. Deliver.

B. Source. Choice "b" is correct. Once demand has been planned, it is necessary to procure the resources required to meet it and to manage the infrastructure that exists for the sources. Collecting and processing vendor payments falls into the "source" process. Choices "a", "c", and "d" are incorrect, per the above Explanation.

Question 126:

A successor auditor most likely would make specific inquiries of the predecessor auditor regarding:

A. Specialized accounting principles of the client's industry. B. The competency of the client's internal audit staff. C. The uncertainty inherent in applying sampling procedures. D. Disagreements with management as to auditing procedures.

D. Disagreements with management as to auditing procedures. Choice "d" is correct. Inquiries should include specific questions regarding, among other things, facts that might bear on the integrity of management; disagreements with management as to accounting principles, auditing procedures, or other similarly significant matters; communications with those charged with governance regarding fraud, illegal acts, and matters relating to internal control; and the predecessor's understanding as to the reasons for the change of auditors. Choice "a" is incorrect. Specialized industry accounting principles might be discussed; however, the successor would be more likely to inquire about items specific to the client. Choice "b" is incorrect. The competency of the client's internal audit staff might be discussed; however, inquiries of the predecessor auditor regarding the staff are not required. Choice "c" is incorrect. The uncertainty in applying sampling procedures is not something that is typically discussed with the predecessor auditor.

Question 127:

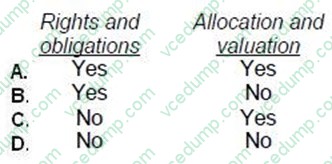

After making inquiries about credit granting policies, an auditor selects a sample of sales transactions and examines evidence of credit approval. This test of controls most likely supports management's financial statement assertion(s) of:

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. By ensuring that credit approval is obtained before goods are shipped to customers, the auditor is testing management's assertion that accounts receivable are collectible (allocation and valuation). Ensuring that credit approval is obtained before goods are shipped does not support the rights and obligations assertion. Choices "a", "b", and "d" are incorrect, based on the above .

Question 128:

Before accepting an engagement to audit a new client, an auditor is required to: A. Make inquiries of the predecessor auditor after obtaining the consent of the prospective client.

B. Obtain an understanding of the entity and its environment, including its internal control.

C. Prepare a memorandum setting forth the staffing requirements and documenting the preliminary audit plan.

D. Discuss the management representation letter with the prospective client's audit committee.

Correct Answer. A

A Choice "a" is correct. Prior to acceptance of a new engagement, an auditor must attempt to communicate with the predecessor auditor. Inquiry is important because the predecessor auditor may provide information critical to the acceptance decision. Under the Rules of the Code of Professional Conduct, the auditor must first request the client's permission. Choice "b" is incorrect. Although the auditor is required to obtain an understanding of the entity and its environment, including its internal control, this typically happens after the engagement is accepted, not before. Choice "c" is incorrect. A planning memo setting forth staff requirements and documenting the preliminary audit plan is usually prepared after accepting an engagement. Choice "d" is incorrect. A management representation letter is usually obtained at the conclusion of the audit and is dated as of the date of auditor's report.

Question 129:

Hannah, CPA, has been engaged to perform financial statement audits for three different clients. The first two clients, ABC Shop and XYZ Technologies, are both nonissuers, while the third client, DEF Industries, is an issuer. Hannah is required to follow PCAOB standards in her audit of DEF Industries. She has also been asked to conduct the XYZ audit in accordance with both generally accepted auditing standards and the auditing standards of the PCAOB. Regarding the ABC engagement, Hannah has decided to follow only generally accepted auditing standards, and not the standards of the PCAOB. Which of the following best describes the scope of Hannah's work related to internal control in these three engagements?

A. Hannah must express an opinion on the effectiveness of internal control in all three engagements. B. Hannah must express an opinion on the effectiveness of internal control in both the DEF and XYZ engagements, but is not required to express such an opinion in the ABC engagement. C. Hannah must express an opinion on the effectiveness of internal control in the DEF engagement, but is not required to express such an opinion in the XYZ and ABC engagements. D. Hannah is not required to express an opinion on the effectiveness of internal control in any of the three engagements, since she was hired to perform a financial statement audit and not to report on internal control.

C. Hannah must express an opinion on the effectiveness of internal control in the DEF engagement, but is not required to express such an opinion in the XYZ and ABC engagements. Choice "c" is correct. Be careful. While it is true that Hannah is following PCAOB standards in both the DEF and XYZ engagements, PCAOB standards do not require expanded testing and reporting on internal control for nonissuers. Therefore, only in the DEF engagement would Hannah be required to express an opinion on the effectiveness of internal control. Choice "a" is incorrect. Hannah is not required to express an opinion on internal control in either the XYZ engagement (because PCAOB standards do not require such an opinion for financial statement audits of nonissuers) or the ABC engagement (because generally accepted auditing standards do not require such an opinion for financial statement audits). Choice "b" is incorrect. Hannah is not required to express an opinion on internal control in the XYZ engagement because PCAOB standards do not require such an opinion for financial statement audits of nonissuers. Choice "d" is incorrect. Hannah is required to express an opinion on internal control in the DEF engagement. PCAOB standards require the auditor to express such an opinion, in conjunction with financial statement audits of issuers.

Question 130:

Which of the following should be disclosed in a summary of significant accounting policies?

A. Basis of profit recognition on long-term construction contracts. B. Future minimum lease payments in the aggregate and for each of the five succeeding fiscal years. C. Depreciation expense. D. Composition of sales by segment.

A. Basis of profit recognition on long-term construction contracts. Choice "a" is correct. The summary of significant accounting policies should disclose policies. The only policy in this question is the "basis" of profit recognition on long-term construction contracts. The other disclosures are accounting details and would be disclosed in other footnotes, but not in the summary of significant accounting policies. Choice "b" is incorrect. The future minimum lease payments should be disclosed, but not in the summary of significant accounting policies. Choice "c" is incorrect. Depreciation expense should certainly be disclosed, but not in the summary of significant accounting policies. Choice "d" is incorrect. The composition of sales by segment should be disclosed, but not in the summary of significant accounting policies.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.