AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 111:

Which of the following is a generally accepted accounting principle that illustrates the practice of conservatism during a particular reporting period?

A. Capitalization of research and development costs. B. Accrual of a contingency deemed to be reasonably possible. C. Reporting investments with appreciated market values at market value. D. Reporting inventory at the lower of cost or market value.

D. Reporting inventory at the lower of cost or market value. Choice "d" is correct. The rule of conservatism states that revenues and gains should be recognized when the earnings process is complete, but that expenses and losses should be expensed immediately. Reporting inventory at the lower of cost or market requires the recording of a loss on inventory when market is lower than cost in the period the loss is sustained, rather than when the inventory is sold, consistent with the rule of conservatism. Choice "a" is incorrect. Because the future benefits of RandD costs are questionable, these cost should be expensed immediately, consistent with the rule of conservatism and the matching principle. Choice "b" is incorrect. The rule of conservatism only requires the accrual of "probable" losses. The accrual of a reasonably possible loss is not required and the accrual of any contingent gain, whether probable, reasonably possible, or remote, is prohibited. Choice "c" is incorrect. The reporting of marketable securities with appreciated values at market value requires the recording of a gain on the asset before the gain is realized. This contradicts the rule of conservatism, but is allowed because fair value is a more relevant measure of the value of marketable securities.

Question 112:

The imputed interest rate used in the residual income approach for performance measurement and evaluation can best be characterized as the:

A. Historical weighted average cost of capital for the company. B. Average return on investment that has been earned by the company over a particular time period. C. Average return on assets employed over a particular time period. D. Average prime lending rate for the year being evaluated.

A. Historical weighted average cost of capital for the company. Choice "a" is correct. Historical weighted average cost of capital is usually used as the target or hurdle rate in the residual income approach. Choices "b", "c", and "d" are incorrect, per the above definition.

Question 113:

Analytical procedures used in planning an audit should focus on:

A. Evaluating the adequacy of evidence gathered concerning unusual balances. B. Testing individual account balances that depend on accounting estimates. C. Enhancing the auditor's understanding of the client's business. D. Identifying material weaknesses in internal control.

C. Enhancing the auditor's understanding of the client's business. Choice "c" is correct. The purpose of applying analytical procedures in planning the audit is to assist in planning the nature, timing, and extent of auditing procedures that will be used to obtain audit evidence for specific account balances or classes of transactions. To accomplish this, the analytical procedures used in planning the audit should focus on (a) enhancing the auditor's understanding of the client's business and the transactions and events that have occurred since the last audit date, and (b) identifying areas that may represent specific risks relevant to the audit. Choice "a" is incorrect. Analytical procedures to assess the adequacy of evidence would be used in the final review stage. Choice "b" is incorrect. Testing individual account balances that depend on accounting estimates would be a substantive application of analytical procedures and would not be used in the planning stages of an audit. Choice "d" is incorrect. Analytical procedures are generally not useful in detecting material weaknesses in the client's internal control.

Question 114:

A partnership agreement must be in writing if:

A. Any partner contributes more than $500 in capital. B. The partners reside in different states. C. The partnership intends to own real estate. D. The partnership's purpose cannot be completed within one year of formation.

D. The partnership's purpose cannot be completed within one year of formation. Choice "d" is correct. Under the statute of frauds, a partnership agreement must be in writing if by its terms the agreement cannot be completed within one year. Choice "a" is incorrect. No such rule. Although the statute of frauds requires a contract for the sale of goods for $500 or more to be evidenced by a writing, a writing is not required to contribute more than $500 in capital to a partnership. Choice "b" is incorrect. No such rule, a far out distracter. Choice "c" is incorrect. While a contract to buy or sell real estate will require a writing, a partnership agreement to own/buy real estate need not be in writing.

Question 115:

Economic theory identifies two basic types of goods: inferior goods and superior goods. As consumer income rises, a lower percentage of earnings are expended on inferior goods while a higher percentage of earnings are spent on superior goods. Overall strategies for achieving organizational missions would most likely match with types of goods as follows:

A. Cost leadership strategies for superior goods, differentiation strategies for inferior goods. B. Cost leadership strategies for inferior goods, differentiation strategies for superior goods. C. Cost leadership strategies would most likely be used for both inferior and superior goods. D. Differentiation strategies would most likely be used for both inferior and superior goods.

B. Cost leadership strategies for inferior goods, differentiation strategies for superior goods. Rule: Overall strategies are divided into two different types that are defined as follows: Cost leadership: Organization seeks to capture market share through maintaining the lowest cost. Differentiation: Organization seeks to capture market share by demonstrating product value. Choice "b" is correct. Organizations that sell economically inferior goods (necessities such as cotton swabs, light bulbs, etc.) are more likely to posture themselves as cost leaders than organizations that sell economically superior goods (luxuries such as cruise packages, fine china, jewelry, etc.) who will likely seek to differentiate the value of their product as part of their strategy. Choice "a" is incorrect. Economically inferior products would likely be associated with cost leadership, not differentiation while economically superior products would likely be associated with differentiation. Choice "c" is incorrect. Economically inferior products would likely be associated with cost leadership, not differentiation while economically superior products would likely be associated with differentiation. Choice "d" is incorrect. Economically inferior products would likely be associated with cost leadership, not differentiation while economically superior products would likely be associated with differentiation.

Question 116:

A stockholder's right to inspect books and records of a corporation will be properly denied if the stockholder:

A. Wants to use corporate stockholder records for a personal business. B. Employs an agent to inspect the books and records. C. Intends to commence a stockholder's derivative suit. D. Is investigating management misconduct.

A. Wants to use corporate stockholder records for a personal business. Choice "a" is correct. In general, a shareholder has a right to inspect the books and records of a corporation for purposes reasonably related to his or her status as a shareholder. This right will be properly denied where the purpose is not reasonably related to their status as a shareholder. Choice "b" is incorrect. In general, a shareholder has a right to inspect the books and records of a corporation for purposes reasonably related to his or her status as a shareholder. A shareholder need not conduct the inspection personally; a shareholder may send an agent such as an attorney or an accountant. Choices "c" and "d" are incorrect. In general, a shareholder has a right to inspect the books and records of a corporation for purposes reasonably related to his or her status as a shareholder. Choices "c" and "d" are purposes reasonably related to the shareholder's status as a shareholder. Thus, the stockholder would have a right to inspect for those reasons.

Question 117:

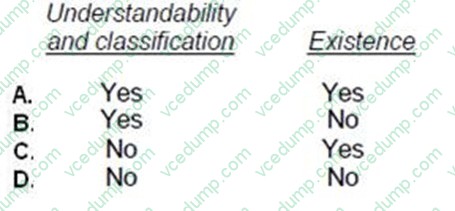

An auditor observes the mailing of monthly statements to a client's customers and reviews evidence of follow-up on errors reported by the customers. This test of controls most likely is performed to support management's financial statement assertions of:

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. In testing the existence or occurrence assertion, the auditor is concerned that fictitious or overstated receivables may have been recorded. Observing the mailing of monthly statements and reviewing evidence of follow-up on errors reported by customers provides evidence that procedures are in place to identify and correct such errors. Choice "a" is incorrect. Follow up of errors in monthly statements does not provide any evidence to support understandability and classification. Choice "b" is incorrect. Follow up of errors in monthly statements does not provide any evidence to support understandability and classification, but does provide evidence regarding the existence of receivables. Choice "d" is incorrect. Follow up of errors in monthly statements does provide evidence regarding the existence of receivables, since customers will be likely to report discrepancies.

Question 118:

Eller, Fort and Owens are members of ABC, LLC. XYZ Corp. brought a breach of contract suit against ABC for a contract executed by Eller as an agent of the LLC. If XYZ prevails, XYZ will generally be able to collect the judgment from:

A. The LLC's assets only. B. The personal assets of Eller, Fort and Owens jointly. C. Eller's personal assets only after LLC assets are exhausted. D. Eller's personal assets only.

A. The LLC's assets only. Choice "a" is correct. Rule: Members of an LLC are not personally liable for the LLC's obligations. Moreover, an agent is not liable on a contract the agent enters into on behalf of a disclosed principal. Here, the contract was entered into by Eller on behalf of Venture, an LLC, and Eller disclosed that he was acting only as an agent of Venture. Thus, Trent Corp. can collect from the LLC'S assets only. Choices "b", "c", and "d" are incorrect, per the above rule.

Question 119:

Which one of the following statements concerning pure monopolies is correct?

A. The demand curve of a monopolist is perfectly elastic. B. The price at which a monopolist maximizes its profit is where price equals both marginal cost and marginal revenue. C. A monopolist's marginal revenue curve lies below its demand curve. D. The supply curve of a monopolist is perfectly inelastic.

C. A monopolist's marginal revenue curve lies below its demand curve. Choice "c" is correct. A monopolist's marginal revenue curve lies below its demand curve. Choice "a" is incorrect. The demand curve of a monopolist is not perfectly elastic. Choice "b" is incorrect. A monopolist sets its price higher than marginal revenue. Choice "d" is incorrect. A monopolist can change the quantity supplied or fix the price but cannot do both simultaneously. In any case, its supply curve is not perfectly inelastic.

Question 120:

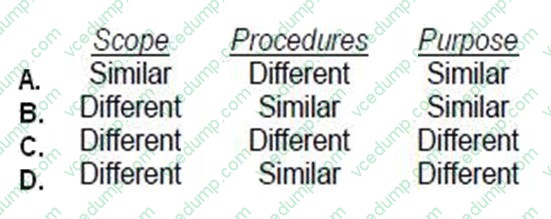

How do the scope, procedures, and purpose of an engagement to express a separate opinion on a nonissuer's internal control compare to those for obtaining an understanding of internal control and assessing control risk as part of an audit?

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. In an engagement to express a separate opinion on an entity's internal control, the scope is extensive, and the purpose is directed primarily toward the internal control report. In an audit, the scope is less extensive, and the purpose is to determine the nature, timing, and extent of auditing procedures. Similar procedures generally would be used in both types of engagements. Choices "a", "b", and "c" are incorrect, based on the above Explanation.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.