CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 141:

A parent corporation owned more than 90% of each class of the outstanding stock issued by a subsidiary corporation and decided to merge that subsidiary into itself. Under the Revised Model Business Corporation Act, which of the following actions must be taken?

A. The subsidiary corporation's board of directors must pass a merger resolution.

B. The subsidiary corporation's dissenting stockholders must be given an appraisal remedy.

C. The parent corporation's stockholders must approve the merger.

D. The parent corporation's dissenting stockholders must be given an appraisal remedy. -

Question 142:

When assessing the internal auditors' competence, the independent CPA should obtain information about the:

A. Organizational level to which the internal auditors report.

B. Educational background and professional certification of the internal auditors.

C. Policies prohibiting the internal auditors from auditing areas where relatives are employed.

D. Internal auditors' access to records and information that is considered sensitive. -

Question 143:

A company has daily cash receipts of $150,000. The treasurer of the company has investigated a lockbox service whereby the bank that offers this service will reduce the company's collection time by four days at a monthly fee of $2,500. If money market rates average four percent during the year, the additional annual income (loss) from using the lockbox service would be:

A. $6,000

B. $(6,000)

C. $12,000

D. $(12,000) -

Question 144:

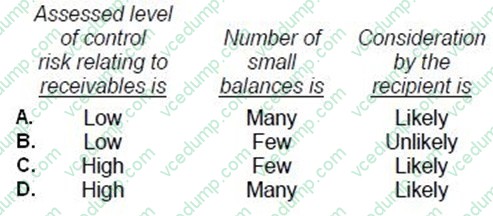

The negative request form of accounts receivable confirmation is useful particularly when the: A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer. A -

Question 145:

Tracing bills of lading to sales invoices provides evidence that:

A. Shipments to customers were recorded as sales.

B. Recorded sales were shipped.

C. Invoiced sales were shipped.

D. Shipments to customers were invoiced. -

Question 146:

Farr made a gift of stock to her child, Pat. At the date of gift, Farr's stock basis was $10,000 and the stock's fair market value was $15,000. No gift taxes were paid. What is Pat's basis in the stock for computing gain?

A. $0

B. $5,000

C. $10,000

D. $15,000 -

Question 147:

A vendor offered ABC Co. $25,000 compensation for losses resulting from faulty raw materials. Alternately, a lawyer offered to represent ABC in a lawsuit against the vendor for a $12,000 retainer and 50% of any award over $35,000. Possible court awards with their associated probabilities are:

Compared to accepting the vendor's offer, the expected value for ABC to litigate the matter to verdict provides a:

A. $4,000 loss.

B. $18,200 gain.

C. $21,000 gain.

D. $38,000 gain. -

Question 148:

Harry, Betty, and Jim decide to form a hair salon business. Betty and Jim agree to equally manage the business and have agreed to accept full personal liability for obligations of the business. Harry contributes money to help them get started. Harry does not want any personal liability but does want access to the books and records and to share in the profits. They have all agreed that unanimous consent is needed to transfer their ownership interests. Assume any necessary filings

have been made. What type of business entity best reflects the terms of their agreement? The three have formed:

A. A limited partnership.

B. A limited liability company.

C. A general partnership.

D. A corporation. -

Question 149:

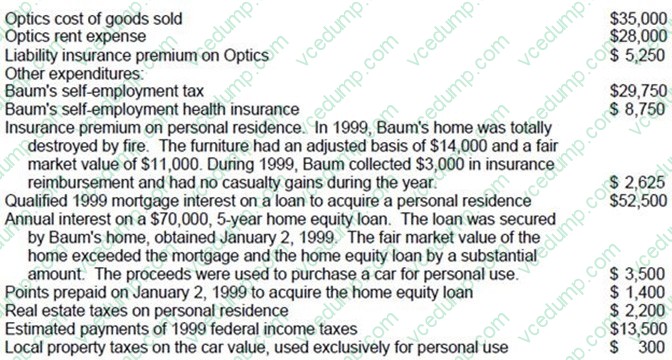

Baum, an unmarried optometrist and sole proprietor of Optics, buys and maintains a supply of eyeglasses and frames to sell in the ordinary course of business. In 1999, Optics had $350,000 in gross business receipts and its year-end

inventory was not subject to the uniform capitalization rules. Baum's 1999 adjusted gross income was $90,000 and Baum qualified to itemize deductions. During 1999, Baum recorded the following information:

Business expenses:

What amount should Baum report as 1999 net earnings from self-employment?

A. $243,250

B. $252,000

C. $273,000

D. $281,750 -

Question 150:

During 1990, ABC Co. had the following unusual financial events occur:

?Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. ABC has frequently retired bonds early when interest rates declined significantly. ?A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location. ?A component of ABC's operations, steel transportation, was sold at a net loss of $350,000.

This was ABC's first divestiture of one of its operating segments. Before income taxes, what amount of gain (loss) should be reported separately as a component of income from continuing operations in 1990?

A. $260,000

B. $5,000

C. $(255,000)

D. $(350,000)

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.