CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 131:

Which of the following is the primary reason that many auditors hesitate to use embedded audit modules?

A. Embedded audit modules cannot be protected from computer viruses.

B. Auditors are required to monitor embedded audit modules continuously to obtain valid results.

C. Embedded audit modules can easily be modified through management tampering.

D. Auditors are required to be involved in the system design of the application to be monitored. -

Question 132:

ABC Industries, which has no current debt, has a beta of .95 for its common stock. Management is considering a change in the capital structure to 30% debt and 70% equity. This change would increase the beta on the stock to 1.05, and the after-tax cost of debt will be 7.5%. The expected return on equity is 16%, and the risk-free rate is 6%. Should ABC's management proceed with the capital structure change?

A. No, because the cost of equity capital will increase.

B. Yes, because the cost of equity capital will decrease.

C. Yes, because the weighted average cost of capital will decrease.

D. No, because the weighted average cost of capital will increase. -

Question 133:

Which one of the following management considerations is usually addressed first in strategic planning?

A. Overall goals of the firm.

B. Organizational structure.

C. Recent annual budgets.

D. Being an industry leader. -

Question 134:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

The Moores received a stock dividend in 1994 from ABC Corp. They had the option to receive either cash or ABC stock with a fair market value of $900 as of the date of distribution. The par value of the stock was $500.

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000 -

Question 135:

For an entity that does not receive governmental financial assistance, an auditor's standard report on financial statements generally would not refer to:

A. Significant estimates made by management.

B. An assessment of the entity's accounting principles.

C. Management's responsibility for the financial statements.

D. The entity's internal control. -

Question 136:

If demand is unit elastic:

A. An increase in price will result in a decline in total revenue.

B. An increase in price will result in a decline the quantity demanded that is less than the increase in price.

C. An increase in price will result in an increase in total revenue.

D. An increase in price will have no effect on total revenue. -

Question 137:

Which of the following evidence provides the least assurance of reliability?

A. Accounts receivable confirmation.

B. Sales invoice.

C. Vendor invoice.

D. Bank statement. -

Question 138:

According to the FASB conceptual framework, which of the following situations violates the concept of reliability?

A. Data on segments having the same expected risks and growth rates are reported to analysts estimating future profits.

B. Financial statements are issued nine months late.

C. Management reports to stockholders regularly refer to new projects undertaken, but the financial statements never report project results.

D. Financial statements include property with a carrying amount increased to management's estimate of market value. -

Question 139:

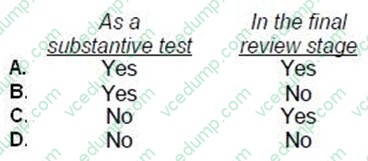

For audits of financial statements made in accordance with generally accepted auditing standards, the use of analytical procedures is required to some extent:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 140:

Symbol A most likely represents:

A. Remittance advice file.

B. Receiving report file.

C. Accounts receivable master file.

D. Cash disbursements transaction file.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.