FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:May 24, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 81:

The cumulative effect of a change in accounting estimate should be shown separately:

A. On the income statement above income from continuing operations.

B. On the income statement after income from continuing operations and before extraordinary items.

C. On the retained earnings statement as an adjustment to the beginning balance.

D. It should not be recorded separately on any financial statement. -

Question 82:

Mellow Co. depreciated a $12,000 asset over five years, using the straight-line method with no salvage value. At the beginning of the fifth year, it was determined that the asset will last another four years. What amount should Mellow report as depreciation expense for year 5?

A. $600

B. $900

C. $1,500

D. $2,400 -

Question 83:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial

statements, or neither an accounting change nor an accounting error.

During 1993, Quo increased its investment in Worth, Inc. from a 10% interest, purchased in 1992, to 30%, and acquired a seat on Worth's board of directors. As a result of its increased investment, Quo changed its method of accounting for

investment in Worth, Inc. from the cost method to the equity method.

List A

A. Change in accounting principle.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error. -

Question 84:

Several sources of GAAP consulted by an auditor are in conflict as to the application of an accounting principle. Which of the following should the auditor consider the most authoritative?

A. FASB Technical Bulletins.

B. AICPA Accounting Interpretations.

C. FASB Statements of Financial Accounting Concepts.

D. AICPA Technical Practice Aids. -

Question 85:

A change from the cost approach to the market approach of measuring fair value is considered to be what type of accounting change?

A. Change in accounting estimate.

B. Change in accounting principle.

C. Change in valuation technique.

D. Error correction. -

Question 86:

In single period statements, which of the following should not be reflected as an adjustment to the opening balance of retained earnings?

A. Effect of a failure to provide for uncollectible accounts in the previous period.

B. Effect of a decrease in the estimated useful life of depreciable equipment.

C. Cumulative effect of a change from the percentage of completion to the completed contract method of accounting for long-term construction projects.

D. Cumulative effect of a change from LIFO to FIFO in valuing merchandise inventory. -

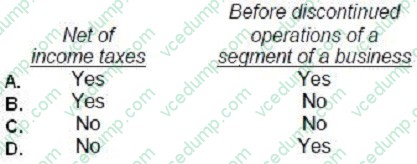

Question 87:

An extraordinary item should be reported separately on the income statement as a component of income:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 88:

During the first quarter of 1993, Tech Co. had income before taxes of $200,000, and its effective income tax rate was 15%. Tech's 1992 effective annual income tax rate was 30%, but Tech expects its 1993 effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of income tax expense should Tech report?

A. $0

B. $30,000

C. $50,000

D. $60,000 -

Question 89:

Under FASB Statement of Financial Accounting Concepts #5, which of the following items would cause earnings to differ from comprehensive income for an enterprise in an industry not having specialized accounting principles?

A. Unrealized loss on investments in noncurrent marketable equity securities available for sale.

B. Unrealized loss on investments in current marketable equity securities held for trading.

C. Loss on exchange of nonmonetary assets without commercial substance.

D. Loss on exchange of nonmonetary assets with commercial substance. -

Question 90:

In which of the following situations should a company report a prior-period adjustment?

A. A change in the estimated useful lives of fixed assets purchased in prior years.

B. The correction of a mathematical error in the calculation of prior years' depreciation.

C. A switch from the straight-line to double-declining balance method of depreciation.

D. The scrapping of an asset prior to the end of its expected useful life.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.