FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:May 24, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 71:

Financial reporting by a development stage enterprise differs from financial reporting for an established operating enterprise in regard to footnote disclosures:

A. Only.

B. And expense recognition principles only.

C. And revenue recognition principles only.

D. And revenue and expense recognition principles. -

Question 72:

According to the FASB's conceptual framework, the process of reporting an item in the financial statements of an entity is:

A. Recognition.

B. Realization.

C. Allocation.

D. Matching. -

Question 73:

In open market transactions, Gold Corp. simultaneously sold its long-term investment in Iron Corp. bonds and purchased its own outstanding bonds. The broker remitted the net cash from the two transactions. Gold's gain on the purchase of

its own bonds exceeded its loss on the sale of the Iron bonds. Assume the transaction to purchase its own outstanding bonds is unusual in nature and has occurred infrequently.

Gold should report the:

A. Net effect of the two transactions as an extraordinary gain.

B. Net effect of the two transactions in income before extraordinary items.

C. Effect of its own bond transaction gain in income before extraordinary items, and report the Iron bond transaction as an extraordinary loss.

D. Effect of its own bond transaction as an extraordinary gain, and report the Iron bond transaction loss in income before extraordinary items. -

Question 74:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment required for these transactions. These treatments are:

A. Cumulative effect approach.

B. Retroactive or retrospective restatement approach.

C. Prospective approach. -

Question 75:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial

statements, or neither an accounting change nor an accounting error.

Item to Be Answered

Quo changed from LIFO to FIFO to account for its finished goods inventory.

List A (Select one)

A. Change in accounting principal.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error. -

Question 76:

Which of the following types of entities are required to report on business segments?

A. Nonpublic business enterprises.

B. Publicly-traded enterprises.

C. Not-for-profit enterprises.

D. Joint ventures. -

Question 77:

Kell Corp.'s $95,000 net income for the quarter ended September 30, 1990, included the following aftertax items:

A. $91,000

B. $103,000

C. $111,000

D. $115,000 -

Question 78:

Opto Co. is a publicly-traded, consolidated enterprise reporting segment information. Which of the following items is a required enterprise-wide disclosure regarding external customers?

A. The fact that transactions with a particular external customer constitute more than 10% of the total enterprise revenues.

B. The identity of any external customer providing 10% or more of a particular operating segment's revenue.

C. The identity of any external customer considered to be "major" by management.

D. Information on major customers is not required in segment reporting. -

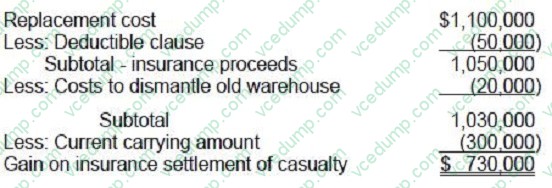

Question 79:

Ocean Corp.'s comprehensive insurance policy allows its assets to be replaced at current value. The policy has a $50,000 deductible clause. One of Ocean's waterfront warehouses was destroyed in a winter storm. Such storms occur approximately every four years. Ocean incurred $20,000 of costs in dismantling the warehouse and plans to replace it. The tax rate is 30%. The following data relate to the warehouse:

Current carrying amount $ 300,000 Replacement cost 1,100,000

What amount of gain should Ocean report as a separate component of income before extraordinary items?

A. $1,030,000

B. $780,000

C. $730,000

D. $0 -

Question 80:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment required for these transactions. These treatments are:

A. Cumulative effect approach.

B. Retroactive or retrospective restatement approach.

C. Prospective approach.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.