FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:May 24, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 101:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial

statements, or neither an accounting change nor an accounting error.

Item to Be Answered

Quo sells extended service contracts on its products. Because related services are performed over several years, in 1993 Quo changed from the cash method to the accrual method of recognizing income from these service contracts.

List A (Select one)

A. Change in accounting principal.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error. -

Question 102:

Which of the following statements regarding fair value is/are correct?

I. The fair value of an asset or liability is specific to the entity making the fair value measurement.

II. Fair value is the price to acquire an asset or assume a liability.

III. Fair value includes transportation costs, but not transaction costs.

IV.

The price in the principal market for an asset or liability will be the fair value measurement.

A. I and II

B. I and IV

C. II and III

D. III and IV

I. The fair value of an asset or liability is specific to the entity making the fair value measurement. II. Fair value is the price to acquire an asset or assume a liability. III. Fair value includes transportation costs, but not transaction costs. IV. The price in the principal market for an asset or liability will be the fair value measurement. -

Question 103:

Which of the following statements best describes an operating procedure for issuing a new Financial Accounting Standards Board (FASB) statement?

A. The emerging issues task force must approve a discussion memorandum before it is disseminated to the public.

B. The exposure draft is modified per public opinion before issuing the discussion memorandum.

C. A new statement is issued only after a majority vote by the members of the FASB.

D. A new FASB statement can be rescinded by a majority vote of the AICPA membership. -

Question 104:

In general, an enterprise preparing interim financial statements should:

A. Defer recognition of seasonal revenue.

B. Disregard permanent decreases in the market value of its inventory.

C. Allocate revenues and expenses evenly over the quarters, regardless of when they actually occurred.

D. Use the same accounting principles followed in preparing its latest annual financial statements. -

Question 105:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial

statements, or neither an accounting change nor an accounting error.

Item to Be Answered

During 1993, Quo determined that an insurance premium paid and entirely expensed in 1992 was for the period January 1, 1992, through January 1, 1994.

List A (Select one)

A. Change in accounting principal.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error. -

Question 106:

On December 2, 20X1, Flint Corp.'s board of directors voted to discontinue operations of its frozen food division and to sell the division's assets on the open market as soon as possible. The division reported net operating losses of $20,000 in December and $30,000 in January. On February 26, 20X2, sale of the division's assets resulted in a gain of $90,000. Assuming that the frozen foods division qualifies as a component of the business and ignoring income taxes, what amount of gain/loss from discontinued operations should Flint recognize in its income statement for 20X2?

A. $0

B. $40,000

C. $60,000

D. $90,000 -

Question 107:

According to the FASB conceptual framework, an entity's revenue may result from:

A. A decrease in an asset from primary operations.

B. An increase in an asset from incidental transactions.

C. An increase in a liability from incidental transactions.

D. A decrease in a liability from primary operations. -

Question 108:

Tack, Inc. reported a retained earnings balance of $150,000 at December 31,1990. In June 1991, Tack discovered that merchandise costing $40,000 had not been included in inventory in its 1990 financial statements. Tack has a 30% tax rate. What amount should Tack report as adjusted beginning retained earnings in its statement of retained earnings at December 31, 1991?

A. $190,000

B. $178,000

C. $150,000

D. $122,000 -

Question 109:

On January 1, 1991, Brecon Co. installed cabinets to display its merchandise in customers' stores. Brecon expects to use these cabinets for five years. Brecon's 1991 multi-step income statement should include:

A. One-fifth of the cabinet costs in cost of goods sold.

B. One-fifth of the cabinet costs in selling, general, and administrative expenses.

C. All of the cabinet costs in cost of goods sold.

D. All of the cabinet costs in selling, general, and administrative expenses. -

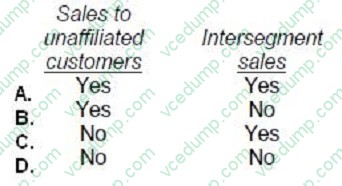

Question 110:

In financial reporting of segment data, which of the following must be considered in determining if an industry segment is a reportable segment?

A. Option A

B. Option B

C. Option C

D. Option D

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.