FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:Jul 15, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 1:

Foy Corp. failed to accrue warranty costs of $50,000 in its December 31, 1992, financial statements. In addition, a $30,000 change from straight-line to accelerated depreciation was made at the beginning of 1993. Both the $50,000 and the $30,000 are net of related income taxes. What amount should Foy report as prior period adjustments in 1993?

A. $0

B. $30,000

C. $50,000

D. $80,000 -

Question 2:

Arpco, Inc., a for-profit provider of healthcare services, recently purchased two smaller companies and is researching accounting issues arising from the two business combinations. Which of the following accounting pronouncements are the most authoritative?

A. AICA Statements of Position.

B. AICPA Industry and Audit Guides.

C. FASB Statements of Financial Accounting Concepts.

D. FASB Statements of Financial Accounting Standards. -

Question 3:

On August 31, 1992, Harvey Co. decided to change from the FIFO periodic inventory system to the weighted average periodic inventory system. Harvey is on a calendar year basis. The cumulative effect of the change is determined:

A. As of January 1, 1992.

B. As of August 31, 1992.

C. During the eight months ending August 31, 1992, by a weighted average of the purchases.

D. During 1992 by a weighted average of the purchases. -

Question 4:

What is the purpose of information presented in notes to the financial statements?

A. To provide disclosures required by generally accepted accounting principles.

B. To correct improper presentation in the financial statements.

C. To provide recognition of amounts not included in the totals of the financial statements.

D. To present management's responses to auditor comments. -

Question 5:

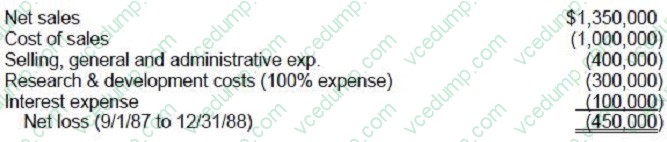

Chester Corp. was a development stage enterprise from its inception on September 1, 1987 to December 31, 1988. The following information was taken from Chester's accounting records for the above period:

For the period September 1, 1987 to December 31, 1988, what amount should Chester report as net loss?

A. $ 50,000

B. $150,000

C. $350,000

D. $450,000 -

Question 6:

On December 31, 20X2, the Board of Directors of Maxy Manufacturing, Inc. committed to a plan to discontinue the operations of its Alpha division. Maxy estimated that Alpha's 20X3 operating loss would be $500,000 and that the fair value of

Alpha's facilities was $300,000 less than their carrying amounts.

The estimate for 20X3 turned out to be correct. Alpha's 20X2 operating loss was $1,400,000, and the division was actually sold for $400,000 less than its carrying amount. Maxy's effective tax rate is 30%.

In its 20X3 income statement, what amount should Maxy report as loss from discontinued operations?

A. $350,000

B. $500,000

C. $420,000

D. $600,000 -

Question 7:

According to the FASB conceptual framework, the objectives of financial reporting for business enterprises are based on:

A. Generally accepted accounting principles.

B. Reporting on management's stewardship.

C. The need for conservatism.

D. The needs of the users of the information. -

Question 8:

In April 30, 20X4, Deer Corp. approved a plan to dispose of a component of its business. For the period January 1 through April 30, 20X4, the component had revenues of $500,000 and expenses of $800,000. The assets of the component were sold on October 15, 20X4 at a loss. In its income statement for the year ended December 31, 20X4, how should Deer report the component's operations from January 1 to April 30, 20X4?

A. $500,000 and $800,000 should be included with revenues and expenses, respectively, as part of continuing operations.

B. $300,000 should be reported as part of the loss on disposal of a component and included as part of continuing operations.

C. $300,000 should be reported as an extraordinary loss.

D. $300,000 should be reported as a loss from operations of a component and included in loss from discontinued operations. -

Question 9:

Which of the following is true regarding the comparison of managerial to financial accounting?

A. Managerial accounting is generally more precise.

B. Managerial accounting has a past focus and financial accounting has a future focus.

C. The emphasis on managerial accounting is relevance and the emphasis on financial accounting is timeliness.

D. Managerial accounting need not follow generally accepted accounting principles (GAAP) while financial accounting must follow them. -

Question 10:

What are the Statements of Financial Accounting Concepts intended to establish?

A. Generally accepted accounting principles in financial reporting by business enterprises.

B. The meaning of "Present fairly in accordance with generally accepted accounting principles."

C. The objectives and concepts for use in developing standards of financial accounting and reporting.

D. The hierarchy of sources of generally accepted accounting principles.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.