FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:Jul 15, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 11:

Reclassification adjustments must be shown in the financial statement that discloses comprehensive income:

A. To show what portion of comprehensive income is from the realization of current assets.

B. To show the tax effect of items of comprehensive income.

C. To avoid double counting in comprehensive income items, which are currently displayed in net income.

D. To avoid including transactions with shareholders in items of comprehensive income. -

Question 12:

How should the effect of a change in accounting principle that is inseparable from the effect of a change in accounting estimate be reported?

A. As a component of income from continuing operations.

B. By restating the financial statements of all prior periods presented.

C. As a correction of an error.

D. By footnote disclosure only. -

Question 13:

Rock Co.'s financial statements had the following balances at December 31:

What amount should Rock report as comprehensive income for the year ended December 31?

A. $400,000

B. $420,000

C. $520,000

D. $570,000 -

Question 14:

According to the FASB conceptual framework, which of the following attributes would not be used to measure inventory?

A. Historical cost.

B. Replacement cost.

C. Net realizable value.

D. Present value of future cash flows. -

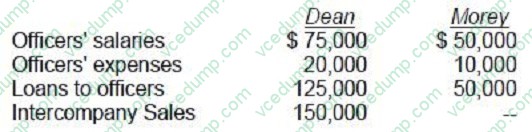

Question 15:

Dean Co. acquired 100% of Morey Corp. prior to 1989. During 1989, the individual companies included in their financial statements the following: What amount should be reported as related party disclosures in the notes to Dean's 1989 consolidated financial statements?

A. $150,000

B. $155,000

C. $175,000

D. $330,000 -

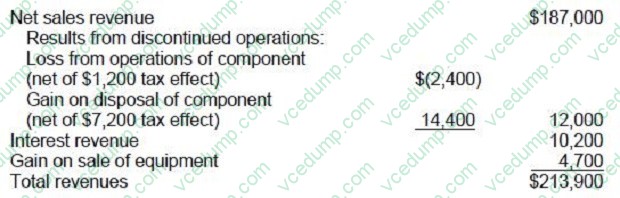

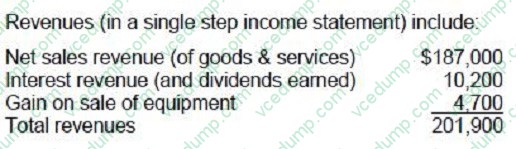

Question 16:

In Baer Food Co.'s 1990 single-step income statement, the section titled "Revenues" consisted of the following:

In the revenues section of its 1990 income statement, Baer Food should have reported total revenues of:

A. $216,300

B. $215,400

C. $203,700

D. $201,900 -

Question 17:

Which of the following statements is incorrect regarding the inputs that can be used to measure fair value?

I. Level I inputs are the most reliable fair value measurements and Level III inputs are the least reliable.

II. Level I measurements are quoted prices in active markets for identical or similar assets or liabilities.

III. A fair value measurement based on management assumptions only (no market data) would not be acceptable per GAAP.

IV.

The level in the fair value hierarchy of a fair value measurement is determined by the level of the highest level significant input.

A. I only.

B. I, II, IV.

C. II, III, IV.

D. I, II, III, IV.

I. Level I inputs are the most reliable fair value measurements and Level III inputs are the least reliable. II. Level I measurements are quoted prices in active markets for identical or similar assets or liabilities. III. A fair value measurement based on management assumptions only (no market data) would not be acceptable per GAAP. IV. The level in the fair value hierarchy of a fair value measurement is determined by the level of the highest level significant input. -

Question 18:

Deficits accumulated during the development stage of a company should be:

A. Reported as organization costs.

B. Reported as a part of stockholders' equity.

C. Capitalized and written off in the first year of principal operations.

D. Capitalized and amortized over a five year period beginning when principal operations commence. -

Question 19:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial

statements, or neither an accounting change nor an accounting error.

Item to Be Answered

As a result of a production breakthrough, Quo determined that manufacturing equipment previously depreciated over 15 years should be depreciated over 20 years.

List A (Select one)

A. Change in accounting principal.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error. -

Question 20:

In 1990, Brighton Co. changed from the individual item approach to the aggregate approach in applying the lower of FIFO cost or market to inventories. The cumulative effect of this change should be reported in Brighton's financial statements as a:

A. Retrospective adjustment on the retained earnings statement, with separate disclosure.

B. Component of income from continuing operations, with separate disclosure.

C. Component of income from continuing operations, without separate disclosure.

D. Component of income after continuing operations, with separate disclosure.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.