FINANCIAL-ACCOUNTING-AND-REPORTING Exam Details

-

Exam Code

:FINANCIAL-ACCOUNTING-AND-REPORTING -

Exam Name

:Financial Reporting -

Certification

:Test Prep Certifications -

Vendor

:Test Prep -

Total Questions

:163 Q&As -

Last Updated

:May 24, 2026

Test Prep FINANCIAL-ACCOUNTING-AND-REPORTING Online Questions & Answers

-

Question 91:

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before,

and instituted new accounting policies.

Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements.

This question represents one of Quo's transactions. List B represents the general accounting treatment required for these transactions. These treatments are:

A. Cumulative effect approach.

B. Retroactive or retrospective restatement approach.

C. Prospective approach. -

Question 92:

On December 31, 20X2, the Board of Directors of Maxy Manufacturing, Inc. committed to a plan to discontinue the operations of its Alpha division. Maxy estimated that Alpha's 20X3 operating loss would be $500,000 and that the fair value of Alpha's facilities was $300,000 less than their carrying amounts.

Alpha's 20X2 operating loss was $1,400,000, and the division was actually sold for $400,000 less than its carrying amount in 20X3. Maxy's effective tax rate is 30%. In its 20X2 income statement, what amount should Maxy report as loss from discontinued operations?

A. $980,000

B. $1,190,000

C. $1,400,000

D. $1,700,000 -

Question 93:

A material loss should be presented separately as a component of income from continuing operations when it is:

A. An extraordinary item.

B. A cumulative effect type change in accounting principle.

C. Unusual in nature and infrequent in occurrence.

D. Not unusual in nature but infrequent in occurrence. -

Question 94:

A segment of Ace Inc. was discontinued during 1992. Ace's loss from discontinued operations should not:

A. Include employee relocation costs associated with the decision to dispose.

B. Exclude operating losses from the date the decision to dispose of the segment was made until the end of 1992.

C. Include additional pension costs associated with the decision to dispose.

D. Include operating losses of the current period up to the date the decision to dispose of the segment was made. -

Question 95:

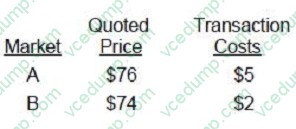

There are multiple active markets for a financial asset with different observable market prices:

There is no principal market for the financial asset. What is the fair value of the asset?

A. $71

B. $72

C. $74

D. $76 -

Question 96:

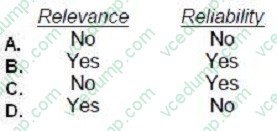

According to the FASB conceptual framework, the quality of information that helps users increase the likelihood of correctly forecasting the outcome of past or present events is called:

A. Feedback value.

B. Predictive value.

C. Representational faithfulness.

D. Reliability. -

Question 97:

According to the FASB conceptual framework, predictive value is an ingredient of:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 98:

What information should a public company present about revenues from its reporting segments?

A. Disclose separately the amount of sales to unaffiliated customers and the amount of intracompany sales.

B. Disclose as a combined amount sales to unaffiliated customers and intracompany sales between geographic areas.

C. Disclose separately the amount of sales to unaffiliated customers but not the amount of intracompany sales between geographic areas.

D. No disclosure of revenues from foreign operations need be reported. -

Question 99:

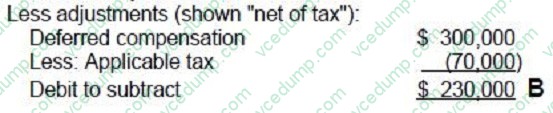

On January 2, 1991, Air, Inc. agreed to pay its former president $300,000 under a deferred compensation arrangement. Air should have recorded this expense in 1990 but did not do so. Air's reported income tax expense would have been $70,000 lower in 1990 had it properly accrued this deferred compensation in its December 31,1991, financial statements, Air should adjust the beginning balance of its retained earnings by a:

A. $230,000 credit.

B. $230,000 debit.

C. $300,000 credit.

D. $370,000 debit. -

Question 100:

Which of the following information should be included in Melay, Inc.'s 1992 summary of significant accounting policies?

A. Property, plant, and equipment is recorded at cost with depreciation computed principally by the straight-line method.

B. During 1992, the Delay component was sold.

C. Business segment 1992 sales are Alay $1M, Belay $2M, and Celay $3M.

D. Future common share dividends are expected to approximate 60% of earnings.

Related Exams:

-

AACD

American Academy of Cosmetic Dentistry -

ACLS

Advanced Cardiac Life Support -

ASSET

ASSET Short Placement Tests Developed by ACT -

ASSET-TEST

ASSET Short Placement Tests Developed by ACT -

BUSINESS-ENVIRONMENT-AND-CONCEPTS

Certified Public Accountant (Business Environment amd Concepts) -

CBEST-SECTION-1

California Basic Educational Skills Test - Math -

CBEST-SECTION-2

California Basic Educational Skills Test - Reading -

CCE-CCC

Certified Cost Consultant / Cost Engineer (AACE International) -

CGFNS

Commission on Graduates of Foreign Nursing Schools -

CLEP-BUSINESS

CLEP Business: Financial Accounting, Business Law, Information Systems & Computer Applications, Management, Marketing

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only Test Prep exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your FINANCIAL-ACCOUNTING-AND-REPORTING exam preparations and Test Prep certification application, do not hesitate to visit our Vcedump.com to find your solutions here.