CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 471:

Acorn and Bean were general partners in a farm machinery business. Acorn contracted, on behalf of the partnership, to purchase 10 tractors from ABC Corp. Unknown to ABC, Acorn was not authorized by the partnership agreement to make such contracts. Bean refused to allow the partnership to accept delivery of the tractors and ABC sought to enforce the contract. ABC will:

A. Lose because Acorn's action was beyond the scope of Acorn's implied authority.

B. Prevail because Acorn had implied authority to bind the partnership.

C. Prevail because Acorn had apparent authority to bind the partnership.

D. Lose because Acorn's express authority was restricted, in writing, by the partnership agreement. -

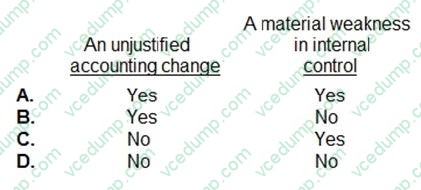

Question 472:

Gail is auditing the financial statements of ABC, a publicly held company. Gail notes several deficiencies in internal control, and is trying to determine whether each deficiency constitutes a significant deficiency or a material weakness. Which best describes the framework Gail should use in making this evaluation?

A. A significant deficiency exists for weaknesses that are important enough to merit the attention of those responsible for financial reporting, and a material weakness exists when there is a reasonable possibility of material misstatement.

B. A significant deficiency exists when there is more than a remote chance of a more than inconsequential misstatement, and a material weakness exists when there is more than a remote chance of a material misstatement.

C. A significant deficiency exists when there is more than a remote chance of a more than inconsequential misstatement, and a material weakness exists when there is a reasonable possibility of material misstatement.

D. A significant deficiency exists for weaknesses that are important enough to merit the attention of those responsible for financial reporting, and a material weakness exists when there is more than a remote chance of a material misstatement. -

Question 473:

To obtain an understanding of a continuing client's business in planning an audit, an auditor most likely would:

A. Perform tests of details of transactions and balances.

B. Review prior-year audit documentation and the permanent file for the client.

C. Read specialized industry journals.

D. Reevaluate the client's internal control environment. -

Question 474:

In 1990, ABC Corp., a closely held corporation, was formed by Adams, Frank, and Berg as incorporators and stockholders. Adams, Frank, and Berg executed a written voting agreement which provided that they would vote for each other as directors and officers. In 1994, stock in the corporation was offered to the public. This resulted in an additional 300 stockholders. After the offering, Adams holds 25%, Frank holds 15%, and Berg holds 15% of all issued and outstanding stock. Adams, Frank, and Berg have been directors and officers of the corporation since the corporation was formed. Regular meetings of the board of directors and annual stockholders meetings have been held. For this question refer to the formation of ABC Corp. and the rights and duties of its stockholders, directors, and officers.

A. Adams, Frank, and Berg must be elected as directors because they own 55% of the issued and outstanding stock.

B. Adams, Frank, and Berg must always be elected as officers because they own 55% of the issued and outstanding stock.

C. Adams, Frank, and Berg must always vote for each other as directors because they have a voting agreement. -

Question 475:

When an independent CPA is associated with the financial statements of a publicly held entity but has not audited or reviewed such statements, the appropriate form of report to be issued must include a(an):

A. Regulation S-X exemption.

B. Report on pro forma financial statements.

C. Unaudited association report.

D. Disclaimer of opinion. -

Question 476:

An auditor would express an unqualified opinion with an explanatory paragraph added to the auditor's report for:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 477:

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

The Moores received $8,400 in gross receipts from their rental property during 1994. The expenses for the residential rental property were:

A. $0

B. $500

C. $900

D. $1,000

E. $1,250

F. $1,300

G. $1,500

H. $2,000

I. $2,500

J. $3,000 K. $10,000 L. $25,000 M. $50,000 N. $55,000 O. $75,000 -

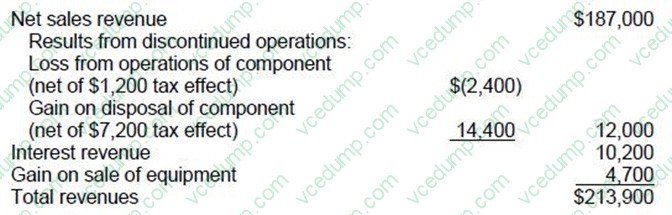

Question 478:

In ABC Food Co.'s 1990 single-step income statement, the section titled "Revenues" consisted of the following:

In the revenues section of its 1990 income statement, ABC Food should have reported total revenues of:

A. $216,300

B. $215,400

C. $203,700

D. $201,900 -

Question 479:

What is the purpose of information presented in notes to the financial statements?

A. To provide disclosures required by generally accepted accounting principles.

B. To correct improper presentation in the financial statements.

C. To provide recognition of amounts not included in the totals of the financial statements.

D. To present management's responses to auditor comments. -

Question 480:

Which of the following parties generally has the most management rights?

A. Minority shareholder in a corporation listed on a national stock exchange.

B. Limited partner in a general partnership.

C. Member of a limited liability company.

D. Limited partner in a limited partnership.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.