AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 451:

Which of the following is correct concerning financial statement disclosure of accounting policies?

A. Disclosures should be limited to principles and methods peculiar to the industry in which the company operates. B. Disclosure of accounting policies is an integral part of the financial statements. C. The format and location of accounting policy disclosures are fixed by generally accepted accounting principles. D. Disclosures should duplicate details disclosed elsewhere in the financial statements.

B. Disclosure of accounting policies is an integral part of the financial statements. Choice "b" is correct. Disclosure of accounting policies (and all other disclosure also) is an integral part of the financial statements. Choice "a" is incorrect. For disclosure of accounting policies, disclosure should not be limited to principles and methods peculiar to the industry in which the company operates. All material accounting policies should be disclosed. Choice "c" is incorrect. For disclosure of accounting policies, the format and location of accounting policies are not fixed by GAAP. Accounting policy disclosures are normally Note 1, but that is a (reasonable and very general) practice and not a "rule." It does make sense to disclose the "why" before the "what." Choice "d" is incorrect. Disclosure of accounting policies should not duplicate details disclosed elsewhere in the financial statements.

Question 452:

With respect to the audit of a nonissuer, significant deficiencies are matters that come to an auditor's attention, which should be communicated to an entity's management and those charged with governance because they represent:

A. Material irregularities or illegal acts perpetrated by high-level management. B. Deficiencies in the design or operation of internal control that could reasonably be expected to cause a non-inconsequential misstatement in the financial statements. C. Flagrant violations of the entity's documented conflict-of-interest policies. D. Intentional attempts by client personnel to limit the scope of the auditor's fieldwork.

B. Deficiencies in the design or operation of internal control that could reasonably be expected to cause a non-inconsequential misstatement in the financial statements. Choice "b" is correct. Significant deficiencies in the design or operation of internal control should be communicated to management and those charged with governance because there is more than a remote likelihood that they will result in a financial statement misstatement that is more than inconsequential. Choice "a" is incorrect. Irregularities or illegal acts may not represent deficiencies in internal control (e.g., if such acts occur through collusion). Choice "c" is incorrect. Significant deficiencies do not necessarily involve violations of an entity's conflictof- interest policies. Choice "d" is incorrect. Interfering with the auditor's procedures would not constitute a significant deficiency, since such interference would not affect the financial statements.

Question 453:

In evaluating the impact of relative inflation rates on the demand for a foreign currency, which of the following is true?

A. Inflation is irrelevant to currency demand. B. As inflation associated with a foreign economy increases in relation to a domestic economy, demand for the foreign currency falls. C. As inflation associated with a foreign economy increases in relation to a domestic economy, demand for the foreign currency increases. D. As inflation associated with a foreign economy decreases in relation to a domestic economy, demand for the foreign currency falls.

B. As inflation associated with a foreign economy increases in relation to a domestic economy, demand for the foreign currency falls. Choice "b" is correct. As inflation associated with a foreign currency increases in relation to a domestic economy, demand for the foreign currency falls. Inflation weakens the foreign currency in relation to the domestic currency and makes foreign products more expensive and reduces demand. Reduced demand for a foreign import will reduce the demand for its currency. Choice "a" is incorrect. Inflation, along with interest rates and trade restrictions are significant determinants of exchange rates. Choice "c" is incorrect. As inflation associated with a foreign currency increases in relation to a domestic economy, demand for the foreign currency falls. Inflation weakens the foreign currency in relation to the domestic currency and makes foreign products more expensive and reduces demand. Reduced demand for a foreign import will reduce the demand for its currency, not increase demand. Choice "d" is incorrect. As inflation associated with a foreign currency decreases in relation to a domestic economy, demand for the foreign currency rises. Inflation weakens the domestic currency in relation to the foreign currency and makes foreign products less expensive and increases demand. Increased demand for a foreign import will increase the demand for its currency, not decrease demand.

Question 454:

Which of the following describes how the objective of a review of financial statements differs from the objective of a compilation engagement?

A. The primary objective of a review engagement is to test the completeness of the financial statements prepared, but a compilation tests for reasonableness. B. The primary objective of a review engagement is to provide positive assurance that the financial statements are fairly presented, but a compilation provides no such assurance. C. In a review engagement, accountants provide limited assurance, but a compilation expresses no assurance. D. In a review engagement, accountants provide reasonable or positive assurance that the financial statements are fairly presented, but a compilation provides limited assurance.

C. In a review engagement, accountants provide limited assurance, but a compilation expresses no assurance. Choice "c" is correct. A review provides limited assurance that there are no material modifications that should be made to the financial statements in order for them to be in conformity with generally accepted accounting principles, whereas a compilation provides no assurance. Choice "a" is incorrect. A review does not test for completeness, nor does a compilation test for reasonableness. A review provides limited assurance about the financial statements based on inquiry and analytical review procedures, while a compilation provides no assurance and includes no testing for reasonableness. Choice "b" is incorrect. A review provides limited assurance that there are no material modifications that should be made to the financial statements in order for them to be in conformity with generally accepted accounting principles, and it is based on inquiry and analytical review procedures. Positive assurance (such as an audit opinion) is only provided when more extensive procedures have been performed. Choice "d" is incorrect. A review provides limited assurance that there are no material modifications that should be made to the financial statements in order for them to be in conformity with generally accepted accounting principles, and it is based on inquiry and analytical review procedures. Positive or reasonable assurance (such as an audit opinion) is only provided when more extensive procedures have been performed. A compilation provides no assurance at all.

Question 455:

Which of the following combinations of procedures would an auditor most likely perform to obtain evidence about fixed asset additions?

A. Inspecting documents and physically examining assets. B. Recomputing calculations and obtaining written management representations. C. Observing operating activities and comparing balances to prior period balances. D. Confirming ownership and corroborating transactions through inquiries of client personnel.

A. Inspecting documents and physically examining assets. Choice "a" is correct. In order to obtain evidence about fixed asset additions, an auditor would most likely inspect documents (e.g., purchase invoices) and physically examine the new assets. Choice "b" is incorrect. Recomputing calculations might provide evidence about depreciation, and obtaining management representations might provide evidence about commitments with respect to fixed assets, but neither procedure provides specific evidence about fixed asset additions. Choice "c" is incorrect. Observing operating activities and comparing balances to prior years might provide evidence that depreciation expense was properly recorded, but does not provide evidence supporting additions. Choice "d" is incorrect. Inquiry alone is not as persuasive as direct personal observation.

Question 456:

Which of the following audit procedures is best for identifying unrecorded trade accounts payable?

A. Reviewing cash disbursements recorded subsequent to the balance sheet date to determine whether the related payables apply to the prior period. B. Investigating payables recorded just prior to and just subsequent to the balance sheet date to determine whether they are supported by receiving reports. C. Examining unusual relationships between monthly accounts payable balances and recorded cash payments. D. Reconciling vendors' statements to the file of receiving reports to identify items received just prior to the balance sheet date.

A. Reviewing cash disbursements recorded subsequent to the balance sheet date to determine whether the related payables apply to the prior period. Choice "a" is correct. When performing a search for unrecorded payables, an auditor most likely would examine cash disbursements recorded after the balance sheet date to determine whether the payables related to the prior period have been included in the accounts payable trial balance. Choice "b" is incorrect. Investigating payables already recorded does not provide any evidence concerning unrecorded payables. Choice "c" is incorrect. While a high level of cash payments compared with a low level of payable balances may be indicative of unrecorded payables, comparing these amounts would not be the most effective method for identifying unrecorded payables. Choice "d" is incorrect. Comparing vendor statements to receiving reports is an audit step not involving the accounts payable balances; this step, therefore, provides no information about accounts payable.

Question 457:

Which of the following tests of controls most likely would help assure an auditor that goods shipped are properly billed?

A. Scan the sales journal for sequential and unusual entries. B. Examine shipping documents for matching sales invoices. C. Compare the accounts receivable ledger to daily sales summaries. D. Inspect unused sales invoices for consecutive prenumbering.

B. Examine shipping documents for matching sales invoices. Choice "b" is correct. Tracing from a sample of shipping documents to matching sales invoices would provide support for the completeness assertion for billing. Choice "a" is incorrect. Scanning the sales journal for sequential and unusual entries tests the completeness and existence assertions for sales, but would not provide assurance that shipped goods were properly billed. Choice "c" is incorrect. Comparing the accounts receivable ledger to the daily sales summary helps ensure that all sales were recorded as receivables and all receivables were recorded as sales, but it does not provide assurance that shipped goods were properly billed. Choice "d" is incorrect. Inspecting the consecutive numbering of unused sales invoices might identify fictitious sales, but it would not ensure that goods that have been shipped were properly billed.

Question 458:

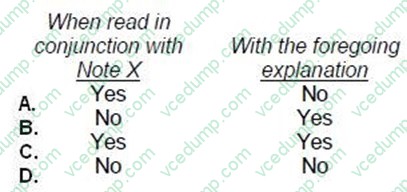

Which of the following phrases should be included in the opinion paragraph when an auditor expresses a qualified opinion?

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. No - No. A qualified opinion phrase is, "in our opinion, except for [of problem] as discussed in the preceding paragraph . . ." Choice "a" is incorrect, as "when read in conjunction with Note X" is not a phrase included in the opinion paragraph of a qualified opinion. Choice "b" is incorrect, as "with the foregoing " is not a phrase included in the opinion paragraph of a qualified opinion. Choice "c" is incorrect. Neither phrase is included in the opinion paragraph of a qualified opinion. (This is why it's important to memorize the qualifying phrases as well as the standard independent auditor's report.)

Question 459:

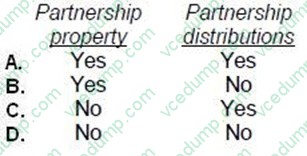

Unless the partnership agreement prohibits it, a partner in a general partnership may validly assign rights to:

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. Rules: A partner has no right to assign an interest in partnership property because a partner's rights in partnership property are limited to using the property for partnership purposes. However, a partner does have a right to assign her interest in partnership distributions. The assignee does not become a partner, but merely has a right to receive whatever distributions the assignor would have received. Choices "a", "b", and "d" are incorrect, per the above rules.

Question 460:

ABC Co. changed from the cash basis of accounting to the accrual basis of accounting during 1994. The cumulative effect of this change should be reported in ABC's 1994 financial statements as a:

A. Prior period adjustment resulting from the correction of an error. B. Prior period adjustment resulting from the change in accounting principle. C. Component of income before extraordinary item. D. Component of income after extraordinary item.

A. Prior period adjustment resulting from the correction of an error. Choice "a" is correct. The cash basis for financial reporting is not a generally accepted accounting basis of accounting (GAAP); therefore, it is an error. Correction of an error from a prior period is a reported as prior period adjustment to retained earnings. Choice "b" is incorrect. Cash basis reporting is not an accounting principle under accrual accounting principles. Thus, the change from cash basis is not reported as a change in accounting principle. In addition, changes in accounting principle are not prior period adjustments; instead, they are treated retrospectively. Choices "c" and "d" are incorrect. Correction of prior period errors has no effect on the current year's income statement.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.