CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 361:

ABC Corp. has three manufacturing divisions, each of which has been determined to be a reportable segment. In 1989, Clay division had sales of $3,000,000, which was 25% of ABC's total sales, and had operating costs of $1,900,000, as reported to the CFO. In 1989, ABC incurred operating costs of $500,000 that were not directly traceable to any of the divisions. In addition, ABC incurred corporate interest expense of $300,000 in 1989. In reporting segment information, what amount should be shown as Clay's operating profit for 1989?

A. $875,000

B. $900,000

C. $975,000

D. $1,100,000 -

Question 362:

Tennis rackets and tennis balls are:

A. Substitute goods.

B. Independent goods.

C. Inferior goods.

D. Complementary goods. -

Question 363:

To determine whether internal control relative to the revenue cycle of a wholesaling entity is operating effectively in minimizing the failure to prepare sales invoices, an auditor most likely would select a sample of transactions from the population represented by the:

A. Sales order file.

B. Customer order file.

C. Shipping document file.

D. Sales invoice file. -

Question 364:

Which of the following internal controls most likely would assure that all billed sales are correctly posted to the accounts receivable ledger?

A. Daily sales summaries are compared to daily postings to the accounts receivable ledger.

B. Each sales invoice is supported by a prenumbered shipping document.

C. The accounts receivable ledger is reconciled daily to the control account in the general ledger.

D. Each shipment on credit is supported by a prenumbered sales invoice. -

Question 365:

An auditor traced a sample of purchase orders and the related receiving reports to the purchases journal and the cash disbursements journal. The purpose of this substantive audit procedure most likely was to:

A. Identify unusually large purchases that should be investigated further.

B. Verify that cash disbursements were for goods actually received.

C. Determine that purchases were properly recorded.

D. Test whether payments were for goods actually ordered. -

Question 366:

Which of the following matters is an auditor required to communicate to those charged with governance?

A. The basis for his or her assessment of control risk.

B. The process used by management in formulating sensitive accounting estimates.

C. The auditor's preliminary judgments about materiality levels.

D. The justification for performing substantive procedures at interim dates. -

Question 367:

Which of the following conditions or events most likely would cause an auditor to have substantial doubt about an entity's ability to continue as a going concern?

A. Significant related party transactions are pervasive.

B. Usual trade credit from suppliers is denied.

C. Arrearages in preferred stock dividends are paid.

D. Restrictions on the disposal of principal assets are present. -

Question 368:

Investment and property schedules are presented for purposes of additional analysis in an auditor submitted document. The schedules are not required parts of the basic financial statements, but accompany the basic financial statements. When reporting on such additional information, the measurement of materiality is the:

A. Same as that used in forming an opinion on the basic financial statements taken as a whole.

B. Lesser of the individual schedule of investments or schedule of property taken by itself.

C. Greater of the individual schedule of investments or schedule of property taken by itself.

D. Combined total of both the individual schedules of investments and property taken as a whole. -

Question 369:

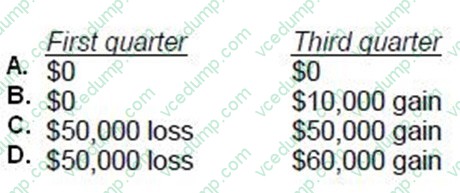

ABC Corp. experienced a $50,000 decline in the market value of its inventory in the first quarter of its fiscal year. ABC had expected this decline to reverse in the third quarter, and in fact, the third quarter recovery exceeded the previous decline by $10,000. ABC's inventory did not experience any other declines in market value during the fiscal year. What amounts of loss and/or gain should ABC report in its interim financial statements for the first and third quarters?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 370:

When do cost leadership strategies fail?

A. Buyers have large amounts of bargaining power in the market.

B. Heavy price competition exists in the market.

C. Buyers become less price sensitive and start to have brand loyalty.

D. New entry firms are able to influence buyers to switch to their product by cutting the price of their product for a period of time in an effort to gain market share and increase profits.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.