AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 351:

ABC Company's bank requires a compensating balance of 20 percent on a $100,000 loan. If the stated interest on the loan is 7 percent, what is the effective cost of the loan?

A. 7.00 percent. B. 8.18 percent. C. 8.40 percent. D. 8.75 percent.

D. 8.75 percent. Choice "d" is correct. Total interest for the loan is $100,000 ?7% or $7,000. The effective amount received is $80,000 after the 20% compensating balance. The effective interest is $7,000 / $80,000 = 8.75%. Choices "a", "b", and "c" are incorrect, per the above calculation.

Question 352:

Economic fluctuations (or business cycles) are best described as:

A. Long run increases in a nation's standard of living. B. Changes in the profits of a given firm from one year to the next. C. Fluctuations of equal duration and equal severity in the level of economic activity over time. D. Fluctuations in the level of economic activity, relative to a long-term growth trend.

D. Fluctuations in the level of economic activity, relative to a long-term growth trend. Choice "d" is correct. By the definition of business cycles. Choice "a" is incorrect. This is economic growth. Choice "b" is incorrect. Business cycles refer to overall economic activity not the activity of one firm. Choice "c" is incorrect. Business cycles are not predictable and are not of equal duration nor of equal severity.

Question 353:

Which of the following statements is correct concerning an auditor's required communication with those charged with governance?

A. This communication is required to occur before the auditor's report on the financial statements is issued. B. This communication should include management changes in the application of significant accounting policies. C. Any significant matter communicated to those charged with governance also should be communicated to management. D. Significant audit adjustments proposed by the auditor and recorded by management need not be communicated to those charged with governance.

B. This communication should include management changes in the application of significant accounting policies. Choice "b" is correct. The auditor should determine that those charged with governance are informed about the initial selection of and changes in significant accounting policies or their application. Choice "a" is incorrect. The communication is incidental to the audit; accordingly, it is not required to occur before the issuance of the auditor's report as long as the communication occurs on a timely basis. (Note, however, that for audits of issuers, the communication must be made before the auditor's report is filed with the SEC.) Choice "c" is incorrect. Communication with management is not required. Choice "d" is incorrect. Unless all those charged with governance are also involved with managing the entity, the auditor should inform those charged with governance about adjustments that could, either individually or in the aggregate, have a significant effect on the entity's financial reporting process, regardless of whether the adjustment was recorded.

Question 354:

A stockholder's right to inspect books and records of a corporation will be properly denied if the purpose of the inspection is to:

A. Commence a stockholder's derivative suit. B. Obtain stockholder names for a retail mailing list. C. Solicit stockholders to vote for a change in the board of directors. D. Investigate possible management misconduct.

B. Obtain stockholder names for a retail mailing list. Choice "b" is correct. In general, a shareholder has a right to inspect the books and records of a corporation for purposes related to the stockholder's interest in the corporation. This right will be denied where the purpose is not reasonably related to their status as a shareholder. Obtaining stockholder names to create a retail mailing list is a personal purpose. Choices "a", "c", and "d" are incorrect. The following reasons for shareholders to inspect the books of the corporation are reasonably related to their status as shareholders: A. To commence a stockholder's derivative suit. C. To solicit stockholders to vote for a change in the board of directors. D. To investigate possible management misconduct.

Question 355:

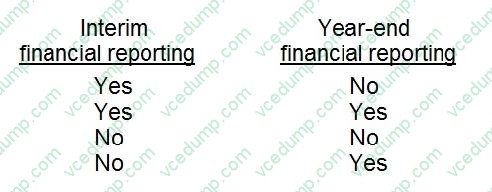

Advertising costs may be accrued or deferred to provide an appropriate expense in each period for: A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer. B

B Choice "b" is correct. Yes - Yes. Advertising costs may be accrued or deferred to provide an appropriate expense in each period for both "interim" and "year-end" financial reporting.

Question 356:

An increase in the minimum wage:

A. Will move employers down the labor demand curve, causing the quantity of labor demanded to fall. II. Is likely to increase the supply of labor, as more people will be willing to work for the higher wage. B. Only I. C. Only II. D. Both I and II. E. Neither I nor II.

D. Both I and II. Choice "d" is correct; neither statement I nor statement II are correct. Statement I is incorrect, as an increase in the minimum wage will move employers up, not down, the labor demand curve, causing the quantity of labor demanded to fall. Statement II is incorrect, as an increase in the minimum wage leads to a decrease in the quantity demanded of labor and an increase in the quantity supplied of labor. It does not increase the supply of labor, only the quantity supplied of labor. Choices "a", "b", and "c" are incorrect, per the above.

Question 357:

In planning and controlling capital expenditures, the most logical sequence is to begin with:

A. Analyzing capital addition proposals. B. Analyzing and evaluating all promising alternatives. C. Identifying capital addition projects and other capital needs. D. Developing capital budgets.

C. Identifying capital addition projects and other capital needs. Choice "c" is correct. The most logical sequence in planning and controlling capital expenditures is to begin with identifying capital addition projects and other capital needs. Choice "a" is incorrect. Analyzing capital addition proposals omits other capital needs. Choice "b" is incorrect. Analyzing and evaluating all promising alternatives is beyond the scope of planning and controlling capital expenditures. Choice "d" is incorrect. Developing capital budgets is the same as planning and controlling capital expenditures.

Question 358:

A company has total costs of $100,000, of which 40% is variable costs. What is the operating leverage?

A. .40 B. .60 C. 1.5 D. 2.5

C. 1.5 Choice "c" is correct. A shortcut computation for operating leverage is the ratio of fixed costs to variable costs. If total cost is $100,000 and variable cost is 40% of total costs (or $40,000), then fixed costs must be 60% (or $60,000). Operating leverage is then calculated as follows: $60,000/$40,000 = 1.5 Choice "a" is incorrect. .4 is obtained by dividing $100,000 into the variable cost of $40,000. Choice "b" is incorrect. .6 is obtained by dividing total costs into fixed costs. Choice "d" is incorrect. 2.5 is obtained by dividing total costs by variable costs.

Question 359:

Which of the following sales should be reported as a capital gain?

A. Sale of equipment. B. Real property subdivided and sold by a dealer. C. Sale of inventory. D. Government bonds sold by an individual investor.

D. Government bonds sold by an individual investor. Choice "d" is correct. Government bonds held by an individual investor are considered capital assets in the hands of the investor. When these types of security investments are sold, the resulting gain or loss is reported as capital. Choice "a" is incorrect. In this case, we must assume that the BEST answer is option "d" (as that option would ALWAYS result in capital gain or loss treatment) and that the examiners are assuming that the equipment is depreciable equipment that has been used in a business for over one year. [If the equipment had been considered a personal asset by the examiners and had sold for a gain, it would also be a capital asset that sold for a capital gain, and there would be two correct answers. Remember that the correct answer is the option that best answers the question.] Depreciable equipment used in a business and held for over one year falls under the category of Section 1245 property. When Section 1245 assets are sold at a gain, all the accumulated depreciation on the asset is recaptured as ordinary income (the same category as the depreciation expense was deducted against), and any remaining gain (typically, in practice, this is not the case, though, as the asset would have had to sell for an amount greater than its purchase price) is capital gain under Code Section 1231. [Note that Section 1245 applies only to gains. If the asset had sold for a loss, the loss would have been ordinary under Section 1231.] Choice "b" is incorrect. Real property sold by a dealer is considered inventory and results in ordinary income or ordinary losses upon sale. Inventory is not a capital asset and is not afforded the capital gain benefits. Choice "c" is incorrect. Inventory is not a capital asset and is not afforded the capital gain benefits. The sale of inventory results in ordinary income or loss (e.g., gross profit on sales) being reported on the tax return, as inventory is an asset held for sale in the ordinary course of business.

Question 360:

Which of the following matters is covered in a typical comfort letter?

A. Negative assurance concerning whether the entity's internal controls operated as designed during the period being audited. B. An opinion regarding whether the entity complied with laws and regulations under Government Auditing Standards and the Single Audit Act of 1984. C. Positive assurance concerning whether unaudited condensed financial information complied with generally accepted accounting principles. D. An opinion as to whether the audited financial statements comply in form with the accounting requirements of the SEC.

D. An opinion as to whether the audited financial statements comply in form with the accounting requirements of the SEC. Choice "d" is correct. In a typical comfort letter, the accountants express an opinion (i.e., positive assurance) concerning the financial statements' compliance (as to form) with the pertinent accounting requirements of the SEC. Choice "a" is incorrect. No assurance is generally provided in a comfort letter regarding the operation of an entity's internal control. Choice "b" is incorrect. A typical comfort letter is addressed to the underwriters of the securities. Government Auditing Standards and the Single Audit Act are not applicable to a comfort letter related to the issuance of securities. Choice "c" is incorrect. Negative assurance (not positive) is typically provided regarding unaudited condensed financial information.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.