AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 371:

According to the FASB conceptual framework, what does the concept of reliability in financial reporting include?

A. Effectiveness. B. Certainty. C. Precision. D. Neutrality.

D. Neutrality. Choice "d" is correct. The concept of reliability in financial reporting includes; neutrality, representational faithfulness and verifiability. Choices "a", "b", and "c" are incorrect, per the above.

Question 372:

If the Federal Reserve wanted to implement an expansionary monetary policy, which one of the following actions would the Federal Reserve take?

A. Raise the reserve requirement and the discount rate. B. Purchase additional U.S. government securities and lower the discount rate. C. Raise the discount rate and sell U.S. government securities. D. Lower the discount rate and raise the reserve requirement.

B. Purchase additional U.S. government securities and lower the discount rate. Choice "b" is correct. Fed purchases of government securities increase the money supply (putting money into circulation), and lowering the discount rate encourages borrowing by member banks and increases the money supply. Hence, these measures would help implement an expansionary monetary policy. Choice "a" is incorrect. Raising the reserve requirement and the discount rate would have the opposite effect of decreasing the money supply. Choice "c" is incorrect. Raising the discount rate and selling government securities would reduce the money supply. Choice "d" is incorrect. Raising the reserve requirement would decrease the money supply, but lowering the discount rate would increase the money supply.

Question 373:

Which of the following procedures would an auditor most likely perform in auditing the statement of cash flows?

A. Compare the amounts included in the statement of cash flows to similar amounts in the prior year's statement of cash flows. B. Reconcile the cutoff bank statements to verify the accuracy of the year-end bank balances. C. Vouch all bank transfers for the last week of the year and first week of the subsequent year. D. Reconcile the amounts included in the statement of cash flows to the other financial statements' balances and amounts.

D. Reconcile the amounts included in the statement of cash flows to the other financial statements' balances and amounts. Choice "d" is correct. To audit the statement of cash flows, the auditor reconciles the amounts on the statement to amounts on other financial statements. Choice "a" is incorrect. Comparison of amounts on the cash flow statement with those of the previous period is an analytical procedure that is not commonly used to audit the statement of cash flows, since sources and uses of cash in the current year are not necessarily predictable based on sources and uses from the prior year. Choice "b" is incorrect. Reconciling the cutoff bank statement is a procedure used to audit the cash balance, rather than the statement of cash flows. Choice "c" is incorrect. Vouching all bank transfers is a procedure used to audit the cash balance, rather than the statement of cash flows.

Question 374:

Which one of a firm's sources of new capital usually has the lowest after tax cost?

A. Retained earnings. B. Bonds. C. Preferred stock. D. Common stock.

B. Bonds. Choice "b" is correct. Because debt is a cheaper source of financing than equity, bonds will be the cheapest form of financing. In addition, the company issuing bonds receives a tax deduction for interest paid. This further reduces the cost of bond financing. Choices "a", "c", and "d" are incorrect, perabove.

Question 375:

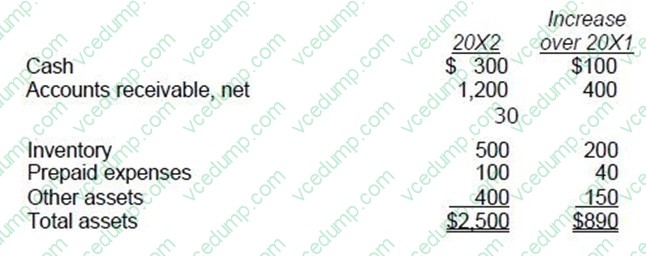

At December 31, 20X2, ABC Co. had the following balances in selected asset accounts:

ABC also had current liabilities of $1,000 at December 31, 20X2, and net credit sales of $7,200 for the year then ended.

What is ABC's acid-test ratio at December 31, 20X2?

A. 1.5 B. 1.6 C. 2.0 D. 2.1

A. 1.5 Choice "a" is correct. The acid-test ratio is calculated by taking the current assets excluding inventory and prepaid expenses and dividing by current liabilities. In this case, cash and accounts receivable ($300 + $1,200 = $1,500) are divided by current liabilities ($1,000), resulting in a ratio of $1,500/$1,000, or 1.5. Choice "b" is incorrect. The numerator in the acid-test ratio formula includes only cash and accounts receivable. It would not include prepaid expenses. Choice "c" is incorrect. The numerator in the acid-test ratio formula includes only cash and accounts receivable. It would not include inventory. Choice "d" is incorrect. The numerator in the acid-test ratio formula includes only cash and accounts receivable. It would not include inventory and prepaid expenses.

Question 376:

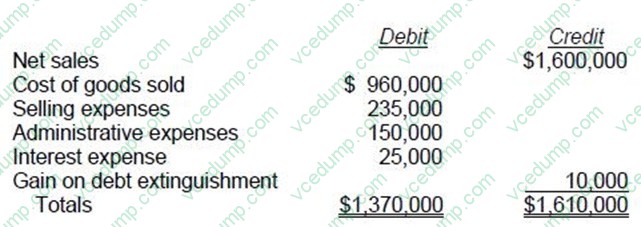

ABC Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as follows:

ABC's income tax rate is 30%. The gain on debt extinguishment is considered a usual and recurring part of ABC's operations. ABC prepares a multiple-step income statement for 1988. Income from operations before income tax is:

A. $190,000 B. $200,000 C. $230,000 D. $240,000

D. $240,000 Choice "d" is correct. $240,000 The gain on debt extinguishment does not meet the unusual and infrequent criteria of APB 30 to be treated as an extraordinary item (per SFAS No. 145, extinguishments of debt are no longer automatically extraordinary), so it is included as part of income from continuing operations.

Question 377:

The president of a company has signed a $10 million contract with a construction company to build a new corporate office. Which of the following corporate documents sets forth the scope of authority under which this transaction is governed?

A. Certificate of Incorporation. B. Charter. C. Bylaws. D. Proxy statement.

C. Bylaws. Choice "c" is correct. The bylaws usually contain the rules for running the corporation. Choices "a" and "b" are incorrect. These are possible choices, but not as good an answer as "c". A corporation's articles of incorporation (called a charter in a few states) must set out certain information relevant to formation of the corporation, but it may include any other information that it is not illegal. However, usually details about intracorporate power are set out in bylaws rather than in the articles or charter. Choice "d" is incorrect. A proxy statement is a request to shareholders to allow their shares to be voted by a specified person in a specified way. It has nothing to do with a corporate president's authority.

Question 378:

Which of the following best describes a CPA's engagement to report on a nonissuer's internal control over financial reporting?

A. An attestation engagement to examine and report on management's written assertions about the effectiveness of its internal control. B. An audit engagement to render an opinion on the entity's internal control. C. A prospective engagement to project, for a period of time not to exceed one year, and report on the expected benefits of the entity's internal control. D. A consulting engagement to provide constructive advice to the entity on its internal control.

A. An attestation engagement to examine and report on management's written assertions about the effectiveness of its internal control. Choice "a" is correct. An engagement to report on an entity's internal control is best described as an attestation engagement to examine and report on management's written assertions about the effectiveness of its internal control. Choice "b" is incorrect. An audit involves expressing (or disclaiming) an opinion on historical financial statements. An engagement to report on internal control is an attestation engagement and not an audit. Thus, the engagement is covered under the attestation standards rather than GAAS. Choice "c" is incorrect. A prospective engagement is not appropriate for a report on internal control. In fact, the CPA's report includes an "inherent limitations" paragraph stating that projections of the internal control evaluation to the future are risky, since conditions or the degree of compliance may change. Choice "d" is incorrect. In a consulting engagement, the practitioner develops findings, conclusions, and recommendations, but does not report on an assertion that is the responsibility of another party. When a CPA reports on an entity's internal control, he or she is in effect reporting on management's assertion.

Question 379:

A planned volume variance in the first quarter, which is expected to be absorbed by the end of the fiscal period, ordinarily should be deferred at the end of the first quarter if it is:

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. Yes - Yes. Rule: Volume variances that are planned or expected to be absorbed by the end of the year should be deferred at interim whether favorable or unfavorable.

Question 380:

Which of the following documents would most likely contain specific rules for the management of a business corporation?

A. Articles of incorporation. B. Bylaws. C. Certificate of authority. D. Shareholders' agreement.

B. Bylaws. Choice "b" is correct. The bylaws are adopted by the incorporators or directors, are not required to be filed, and generally will contain rules desired regarding the operation of the corporation. Choice "a" is incorrect. Articles of incorporation are filed with the state and contain information regarding the formation of the corporation. Choice "c" is incorrect. A certificate of authority is filed with the foreign state that a business wishes to do business in and with permission from that state. Choice "d" is incorrect. A shareholder agreement is a contract between shareholders for any rights or duties agreed upon between the parties.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.