CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 321:

In which case would the accountant be least likely to perform a review of interim financial information under PCAOB (auditing) standards?

A. Quarterly reports are required to be filed with the SEC.

B. Selected quarterly financial data is included in an annual report.

C. Quarterly financial data is included in the financial statements of a nonissuer.

D. The accountant is performing an initial audit of financial statements that include selected quarterly data. -

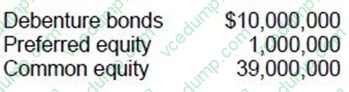

Question 322:

ABC Corporation has the following capital structure:

The financial leverage of ABC Corp. would increase as a result of:

A. Issuing common stock and using the proceeds to retire preferred stock.

B. Issuing common stock and using the proceeds to retire debenture bonds.

C. Financing its future investments with a higher percentage of bonds.

D. Financing its future investments with a higher percentage of equity funds. -

Question 323:

Management of ABC Industries plans to disclose an uncertainty as follows:

The Company is a defendant in a lawsuit alleging infringement of certain patent rights and claiming damages. Discovery proceedings are in progress. The ultimate outcome of the litigation cannot presently be determined. Accordingly, no

provision for any liability that may result upon adjudication has been made in the accompanying financial statements.

The auditor is satisfied that sufficient audit evidence supports management's assertions about the nature and disclosure of the uncertainty. What type of opinion should the auditor express under these circumstances?

A. Unqualified without an explanatory paragraph.

B. "Subject to" qualified.

C. "Except for" qualified.

D. Disclaimer of opinion. -

Question 324:

Which of the following statements is the best definition of real property?

A. Real property is only land.

B. Real property is all tangible property including land.

C. Real property is land and intangible property in realized form.

D. Real property is land and everything permanently attached to it. -

Question 325:

Which one of the following provides a spontaneous source of financing for a firm?

A. Accounts payable.

B. Accounts receivable.

C. Debentures.

D. Preferred stock. -

Question 326:

The concept of materiality would be least important to an auditor when considering the:

A. Adequacy of disclosure of a client's illegal act.

B. Discovery of weaknesses in a client's internal control.

C. Effects of a direct financial interest in the client on the CPA's independence.

D. Decision whether to use positive or negative confirmations of accounts receivable. -

Question 327:

Which of the following methods is designed to measure transaction exposure in terms of the maximum one day loss related to holdings denominated in foreign currency?

A. Measurement of currency variability. II. Measurement of currency correlations. III. Value at risk.

B. I only.

C. II only.

D. III only.

E. I, II, and III. -

Question 328:

A company obtained a short-term bank loan of $500,000 at an annual interest rate of eight percent. As a condition of the loan, the company is required to maintain a compensating balance of $100,000 in its checking account. The checking account earns interest at an annual rate of three percent. Ordinarily, the company maintains a balance of $50,000 in its account for transaction purposes. What is the effective interest rate of the loan?

A. 7.77 percent.

B. 8.50 percent.

C. 9.44 percent.

D. 8.56 percent. -

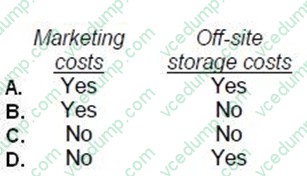

Question 329:

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 330:

ABC Co. is considering the acquisition of a new, more efficient press. The cost of the press is $360,000, and the press has an estimated six-year life with zero salvage value. ABC uses straightline depreciation for both financial reporting and income tax reporting purposes and has a 40 percent corporate income tax rate. In evaluating equipment acquisitions of this type, ABC uses a goal of a four-year payback period. To meet ABC's desired payback period, the press must produce a minimum annual before-tax, operating cash savings of:

A. $90,000

B. $110,000

C. $114,000

D. $150,000

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.