AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 311:

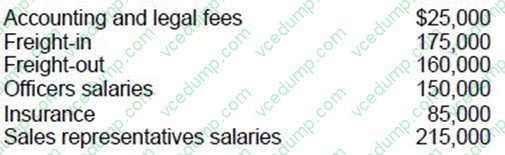

The following costs were incurred by ABC Co., a manufacturer, during 1992:

What amount of these costs should be reported as general and administrative expenses for 1992?

A. $260,000 B. $550,000 C. $635,000 D. $810,000

A. $260,000 Explanation Explanation/Reference:Choice "a" is correct. $260,000. General and administrative "Freight-in" is part of "cost of goods sold." "Freight-out" is a "selling" expense. Sales representative salaries is a selling expense.

Question 312:

The annual financial statements of a publicly held company have been audited, and its interim financial statements have been reviewed. Which of the following is true about the application of professional standards to this review?

A. PCAOB standards apply. B. Statements on Standards for Accounting and Review Services apply. C. Both PCAOB standards and SSARS apply. D. None of the above.

A. PCAOB standards apply. Choice "a" is correct. A review of the interim financial information of a publicly held company is conducted in accordance with PCAOB standards, and it is these standards which should be referenced in the auditor's review report. (Note, however, that the PCAOB has adopted, at least initially, generally accepted auditing standards in this area.) Choices "b" and "c" are incorrect. Statements on Standards for Accounting and Review Services apply to reviews of the financial statements of nonissuers. Choice "d" is incorrect. A review of the interim financial information of a publicly held company is conducted in accordance with PCAOB standards.

Question 313:

Any business firm that has the ability to control the price of the product it sells:

A. Faces a downward-sloping demand curve. B. Does not have any entry or exit barriers in its industry. C. Has a supply curve that is horizontal. D. Has a demand curve that is horizontal.

A. Faces a downward-sloping demand curve. Choice "a" is correct. Any business firm that has the ability to control the price of the product it sells faces a downward-sloping demand curve for the firm. Only the firm in a competitive market is a price-taker facing a horizontal demand curve at the market equilibrium price. Choice "b" is incorrect. Firms in competitive industries have no entry or exit barriers and are price-takers. Choice "c" is incorrect, this is a far-out distractor. Choice "d" is incorrect. Only firms in perfectly competitive markets (price-takers) face horizontal demand curves.

Question 314:

Which of the following factors most likely would cause a CPA to decide not to accept a new audit engagement?

A. The CPA's lack of understanding of the prospective client's internal auditor's computer-assisted audit techniques. B. Management's disregard of its responsibility to maintain an adequate internal control environment. C. The CPA's inability to determine whether related party transactions were consummated on terms equivalent to arm's-length transactions. D. Management's refusal to permit the CPA to perform substantive tests before the year-end.

B. Management's disregard of its responsibility to maintain an adequate internal control environment. Choice "b" is correct. The control environment is the foundation for all other components of internal control. Management's disregard of its responsibility to maintain an adequate internal control environment therefore compromises its ability to provide reasonable assurance regarding reliable financial reporting. The auditor may conclude that the risk of misrepresentation in the financial statements is great enough that an audit should not be conducted. Choice "a" is incorrect. The CPA does not need to understand the internal auditor's techniques in order to accept a new audit engagement. Choice "c" is incorrect. Related party transactions (by definition) are not considered to be arm's-length transactions, and evaluation of such transactions does not affect the CPA's decision regarding acceptance of new clients. Choice "d" is incorrect. Substantive tests are generally performed after year-end, since prior to that time the financial statements have not been finalized.

Question 315:

Which of the following statements is correct concerning an auditor's use of the work of a specialist?

A. The work of a specialist who is related to the client may be acceptable under certain circumstances. B. If an auditor believes that the determinations made by a specialist are unreasonable, only a qualified opinion may be issued. C. If there is a material difference between a specialist's findings and the assertions in the financial statements, only an adverse opinion may be issued. D. An auditor may not use a specialist in the determination of physical characteristics relating to inventories.

A. The work of a specialist who is related to the client may be acceptable under certain circumstances. Choice "a" is correct. The work of a specialist who has a relationship with a client may be acceptable under certain circumstances. If the specialist is related to the client, the auditor should consider performing additional procedures with respect to the specialist's assumptions, methods, or findings to determine that the findings are not unreasonable, or should engage another specialist for that purpose. Choice "b" is incorrect. If the auditor believes the findings are unreasonable, the auditor should apply additional procedures, which may include obtaining the opinion of another specialist. This does not imply that there is a problem with the financial statements, and therefore would not necessarily result in a qualified opinion. Choice "c" is incorrect. If there is a material difference between a specialist's findings and the assertions in the financial statements, and if the specialist's findings are deemed reasonable, either a qualified or an adverse opinion may be issued. (Note that it is also possible that the specialist's findings turn out to be erroneous, in which case an unqualified opinion might be issued.) Choice "d" is incorrect. A specialist may be used to determine the physical characteristics relating to inventory (e.g., quantity on hand or condition).

Question 316:

A CPA wishes to determine how various publicly-held companies have complied with the disclosure requirements in a Statement of Financial Accounting Standards. Which of the following information sources would the CPA most likely consult for this information?

A. AICPA Accounting Trends and Techniques. B. FASB Technical Bulletins. C. AICPA Audit and Accounting Manual. D. FASB Statements of Financial Accounting Concepts.

A. AICPA Accounting Trends and Techniques. Choice "a" is correct. The AICPA's Accounting Trends and Techniques is an annual survey of accounting practices followed in 600 stockholders' annual reports. Choice "b" is incorrect. FASB Technical Bulletins are considered to be a source of established accounting principles that expand upon or further clarify GAAP. They do not provide information regarding how various companies comply with GAAP. Choice "c" is incorrect. AICPA Audit and Accounting Guides are interpretive publications that provide additional guidance regarding the application of auditing standards. They do not provide information regarding how various companies comply with GAAP. Choice "d" is incorrect. FASB Statements of Financial Accounting Concepts establish the objectives and concepts for use by the FASB in developing accounting and reporting standards. They do not provide information regarding how various companies comply with GAAP.

Question 317:

For the next 2 years, a lease is estimated to have an operating net cash inflow of $7,500 per annum, before adjusting for $5,000 per annum tax basis lease amortization, and a 40% tax rate. The present value of an ordinary annuity of $1 per year at 10% for 2 years is $1.74. What is the lease's after-tax present value using a 10% discount factor?

A. $2,610 B. $4,350 C. $9,570 D. $11,310

D. $11,310 Choice "d" is correct. Present value is based on the cash flows of an activity. Amortization is a non-cash expense that is considered only for its tax shield; therefore, the only relevant amounts are the $7,500 operating net cash inflow and the tax paid. After-tax PV $11,310 Choice "a" is incorrect. Amortization expense of $5,000 is a non-cash expense and is not used to compute after-tax present value. It is used to determine the cash paid for taxes. Choice "b" is incorrect. Amortization is a non-cash expense. It is not considered in the calculation, expecpt to the extent it creates a tax shield. The tax shield reduces the amount of taxes paid out by the company. Choice "c" is incorrect. Present value is based on the cash flows of an activity. Amortization is a noncash expense that is considered only for its tax shield; therefore, the only relevant amounts are the $7,500 operating net cash inflow and the tax paid.

Question 318:

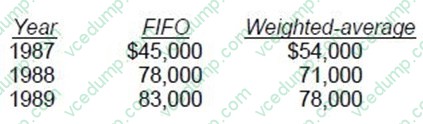

Goddard has used the FIFO method of inventory valuation since it began operations in 1987. Goddard decided to change to the weighted-average method for determining inventory costs at the beginning of 1990. The following schedule shows year-end inventory balances under the FIFO and weighted-average methods:

What amount, before income taxes, should be reported in the 1990 retained earnings statement as the cumulative effect of the change in accounting principle?

A. $5,000 decrease. B. $3,000 decrease. C. $2,000 increase. D. $0.

A. $5,000 decrease. Choice "a" is correct. $5,000 decrease. The cumulative effect of change in accounting principle is determined as of the beginning of the year of change if comparative financial statements are not presented. In this case, the year of change is 1990, so the cumulative effect is the difference in inventory as of the end of 1989. [Note that inventory is a balance sheet item, so the change is based on the balances at the end of the last year the prior method was used. Had this question shown annual income statement amounts of cost of goods sold, we would have had to look at all the past years in the aggregate.] This will allow us to arrive at the adjustment to obtain the amount of retained earnings that would have been reported at the beginning of the period of change if the new accounting principle had been used for all prior periods.

Question 319:

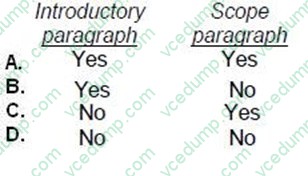

When an auditor qualifies an opinion because of inadequate disclosure, the auditor should describe the nature of the omission in a separate explanatory paragraph and modify the:

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. In a report qualified for inadequate disclosure, the auditor would add an explanatory paragraph and modify the opinion paragraph, but the introductory and scope paragraphs would not be modified. Choices "a", "b", and "c" are incorrect, as per the above explanation.

Question 320:

Dale received $1,000 in 1990 for jury duty. In exchange for regular compensation from her employer during the period of jury service, Dale was required to remit the entire $1,000 to her employer in 1990. In Dale's 1990 income tax return, the $1,000 jury duty fee should be:

A. Claimed in full as an itemized deduction. B. Claimed as an itemized deduction to the extent exceeding 2% of adjusted gross income. C. Deducted from gross income in arriving at adjusted gross income. D. Included in taxable income without a corresponding offset against other income.

C. Deducted from gross income in arriving at adjusted gross income. Choice "c" is correct. The $1,000 jury duty fee that was required to be remitted to the employer may be deducted from gross income in arriving at adjusted gross income. This, in effect, washes out the $1,000 income she will have to report as part of gross income for the jury duty fees paid to her. Choices "a" and "b" are incorrect. The amount remitted is allowed as an adjustment in arriving at AGI, not as an itemized deduction. Choice "d" is incorrect. A corresponding offset is allowed against other income as an adjustment in arriving at AGI.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.