AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

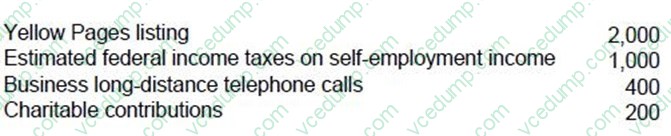

Question 271:

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich's cash disbursements were as follows:

What amount should Rich report as net self-employment income?

A. $15,100 B. $14,900 C. $14,100 D. $13,900

A. $15,100 Explanation Explanation/Reference:Choice "a" is correct. Deductions to arrive at net self-employed income include all necessary and ordinary expenses connected with the business. Estimated federal income tax payments are not an expense. Charitable contributions by an individual are only deductible as an itemized deduction on Schedule A. This assumes the contribution was not made with the "expectation of commensurate financial return." Choice "b" is incorrect. Charitable contributions are an itemized deduction unless there is an expectation of commensurate financial return. Choice "c" is incorrect. Federal income taxes paid are not a deductible expense. Choice "d" is incorrect. Charitable contributions are an itemized deduction unless there is an expectation of commensurate financial return. Federal income taxes paid are not a deductible expense.

Question 272:

This question will represent a statement, question, excerpt, or comment taken from various parts of an auditor's documentation file. Letter choices A-P represent a list of the likely sources of the statement, question, excerpt, or comment.

Select, as the best answer for each item, the most likely source. Select only one source for each item.

Was the difference of opinion on the accrued pension liabilities that existed between the engagement personnel and the actuarial specialist resolved in accordance with firm policy and appropriately documented?

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements. B. Auditor's communications on significant deficiencies in internal control. C. Audit inquiry letter to legal counsel. D. Lawyer's response to audit inquiry letter. E. Communication from those charged with governance to the auditor. F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies in internal control). G. Report on the application of accounting principles. H. Auditor's engagement letter. I. Letter for underwriters. J. Accounts receivable confirmation request. K. Request for bank cutoff statement. L. Explanatory paragraph of an auditor's report on financial statements. M. Partner's engagement review notes. N. Management representation letter. O. Successor auditor's communication with predecessor auditor. P. Predecessor auditor's communication with successor auditor.

M Choice "M" is correct. The engagement partner has ultimate responsibility for the performance of the audit and the preparation of the report. He or she would therefore want to ensure that any differences of opinion between engagement personnel and a specialist were resolved in accordance with firm policy and were appropriately documented.

Question 273:

Which of the following should be disclosed for each reportable operating segment of an enterprise?

A. Option A B. Option B C. Option C D. Option D

A. Option A Choice "a" is correct. For each reportable segment of an enterprise, both profit or loss and total assets should be disclosed. In disclosure questions, if you are not sure, disclose the most rather than the least. Choice "b" is incorrect. For each reportable segment of an enterprise, both profit or loss and total assets should be disclosed. Choice "c" is incorrect. For each reportable segment of an enterprise, both profit or loss and total assets should be disclosed. Choice "d" is incorrect. For each reportable segment of an enterprise, both profit or loss and total assets should be disclosed.

Question 274:

An auditor most likely would express an unqualified opinion and would not add explanatory language to the report if the auditor:

A. Wishes to emphasize that the entity had significant transactions with related parties. B. Concurs with the entity's change in its method of computing depreciation. C. Discovers that supplementary information required by FASB has been omitted. D. Believes that there is a probable likelihood of a material loss resulting from an uncertainty that is sufficiently supported and disclosed.

D. Believes that there is a probable likelihood of a material loss resulting from an uncertainty that is sufficiently supported and disclosed. Choice "d" is correct. An auditor most likely would express an unqualified opinion and would not add explanatory language to the report if the auditor believes that there is a probable likelihood of a material loss resulting from an uncertainty that is sufficiently supported and disclosed. Choice "a" is incorrect. Emphasis of a matter, such as the existence of significant transactions with related parties, may result in an additional explanatory paragraph appended to an otherwise unqualified opinion. Choice "b" is incorrect. A change in accounting principle does result in an additional explanatory paragraph appended to an otherwise unqualified opinion. Choice "c" is incorrect. Omission of supplemental information required by GAAP does result in an additional explanatory paragraph appended to an otherwise unqualified opinion.

Question 275:

When does competition not become an even stronger force impacting the profitability of a firm?

A. The market consists of several equal-sized firms. B. Customers do not have strong brand preferences. C. The market is fast-growing. D. The costs of exiting the market exceed the costs of continuing to operate.

C. The market is fast-growing. Choice "c" is correct, as it is not a factor that would cause market competitiveness to be even stronger. Choices "a", "b", and "d" are incorrect because they are all reasons that competition becomes an even stronger force that impacts the firm's profitability. The following are situations that would cause competition to be an even stronger force impacting the profitability of a firm: ?The market is not growing fast. ?There are several equal-sized firms in the market. ?Customers do not have strong brand preferences. ?The costs of exiting the market exceed the costs of continuing to operate. ?Some firms profit from making certain moves to increase market share. ?The various firms in the market use different types of strategic plans.

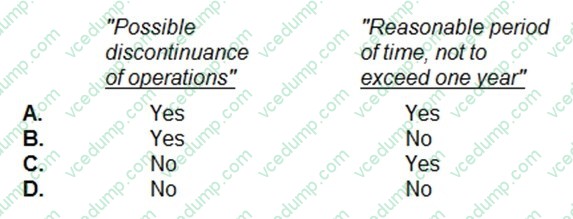

Question 276:

Kane, CPA, concludes that there is substantial doubt about ABC Co.'s ability to continue as a going concern for a reasonable period of time. If ABC's financial statements adequately disclose its financial difficulties, Kane's auditor's report is required to include an explanatory paragraph that specifically uses the phrase(s):

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. If, after considering identified conditions and events and management's plans, the auditor concludes that substantial doubt about the entity's ability to continue as a going concern for a reasonable period of time remains, the audit report should include an explanatory paragraph (following the opinion paragraph) to reflect that conclusion. This conclusion should be expressed through the use of the phrase "substantial doubt about its (the entity's) ability to continue as a going concern" [or similar wording that includes the terms "substantial doubt" and "going concern"]. The "reasonable period...not to exceed one year" is inherent in the definition of going concern and is not explicitly stated in the audit report. The phrase "possible discontinuation of operations" may be included in the going concern disclosure but is not specifically required. Choices "a", "b", and "c" are incorrect, as per the above explanation.

Question 277:

Proper authorization of write-offs of uncollectible accounts should be approved in which of the following departments?

A. Accounts receivable. B. Credit. C. Accounts payable. D. Treasurer.

D. Treasurer. Choice "d" is correct. Proper authorization of write-offs of uncollectible accounts are approved by the treasurer, who is not involved in the record-keeping function or the initiation of the write-off. Choice "a" is incorrect. Proper segregation of duties requires that the authorization of the write-off be performed by individuals not involved with the accounts receivable department that records the original transactions. Choice "b" is incorrect. The credit department should grant credit and approve credit limits before the sale is made. If the credit department also approved the write-offs of accounts, there would be a lack of appropriate segregation of duties. Choice "c" is incorrect. Even though the accounts payable department is independent of the accounts receivable department, they are not particularly knowledgeable regarding the customers and therefore would not be the best candidates for authorizing the write-offs of accounts receivable.

Question 278:

In general, which of the following statements is correct with respect to a limited partnership?

A. A limited partner has the right to obtain from the general partner(s) financial information and tax returns of the limited partnership. B. A limited partnership can be formed with limited liability for all partners. C. A limited partner may not also be a general partner at the same time. D. A limited partner may hire employees on behalf of the partnership.

A. A limited partner has the right to obtain from the general partner(s) financial information and tax returns of the limited partnership. Choice "a" is correct. A limited partner has rights similar to those of a corporate shareholder; he must be allowed to review financial and tax information of the limited partnership. Choice "b" is incorrect. A limited partnership must have one or more general partners, whose liability is unlimited. Choice "c" is incorrect. One may be both a general and a limited partner simultaneously. Such a person has all of the rights and liabilities of both a limited partner and a general partner. Choice "d" is incorrect. A limited partner has no management authority, rather he is a passive investor, like a corporate shareholder.

Question 279:

Which of the following statements regarding the existence of substitute products is correct?

A. The impact of substitutes will have more of an effect on the competitive environment of a firm if the substitutes are difficult for customers to obtain. B. When the cost of buyers switching to new products is high, the effect of substitutes on the competitive environment of a firm is high. C. If few substitutes exist, buyers have little choice of products and may be willing to pay a higher price for the products that are available. D. If few substitutes exist, buyers may have a limit on the maximum price that they are willing to pay and may choose to not purchase the firm's product if the price is too high.

C. If few substitutes exist, buyers have little choice of products and may be willing to pay a higher price for the products that are available. Choice "c" is correct. If few substitutes exist, buyers have little choice of products and may be willing to pay a higher price for the products that are available. Choice "a" is incorrect. The impact of substitutes will have more of an effect on the competitive environment of a firm if the substitutes are readily available to consumers (not difficult to obtain). Choice "b" is incorrect. When the cost of buyers switching to new products is low (not high), the effect of substitutes on the competitive environment of a firm is high. Choice "d" is incorrect. If many (not few) substitutes exist, buyers may have a limit on the maximum price that they are willing to pay and may choose to not purchase the firm's product if the price is too high.

Question 280:

The movement along the demand curve from one price-quantity combination to another is called a(n):

A. Change in demand. B. Shift in the demand curve. C. Change in the quantity demanded. D. Increase in demand.

C. Change in the quantity demanded. Choice "c" is correct. References to the change in quantity demanded refer to a single demand curve, which is downward sloping to the right. Changes in the quantity demanded result from changes in price. Choices "a", "b", and "d" are incorrect. All refer to changes in the demand curve itself, like an outward shift from curve D - D to D1 - D1.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.