CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 281:

What are the Statements of Financial Accounting Concepts intended to establish?

A. Generally accepted accounting principles in financial reporting by business enterprises.

B. The meaning of "Present fairly in accordance with generally accepted accounting principles."

C. The objectives and concepts for use in developing standards of financial accounting and reporting.

D. The hierarchy of sources of generally accepted accounting principles. -

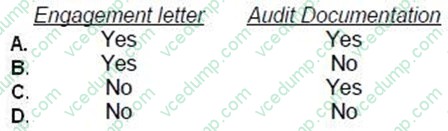

Question 282:

A successor auditor should request the new client to authorize the predecessor auditor to allow a review of the predecessor's:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 283:

Which of the following statements represents a quality control requirement under Government Auditing Standards?

A. A CPA who conducts government audits is required to undergo an annual external quality control review when an appropriate internal quality control system is not in place.

B. A CPA seeking to enter into a contract to perform an audit should provide the CPA's most recent external quality control review report to the party contracting for the audit.

C. An external quality control review of a CPA's practice should include a review of the audit documentation for each government audit performed since the prior external quality control review.

D. A CPA who conducts government audits may not make the CPA's external quality control review report available to the public. -

Question 284:

A basic determinant of the elasticity of demand for a normal good is the:

A. Length of time producers have to respond to market changes.

B. Number of substitutes available for the product.

C. Number of sellers of the product.

D. Number of complements available for the product. -

Question 285:

Sam, CPA, is one of the partners in a limited liability partnership with other CPAs. Sam avoids personal liability for:

A. The wrongful acts of employees acting under his supervision.

B. His own negligent acts.

C. The malpractice of his partners regarding errors and omissions.

D. The negligent actions of his subordinates under his direct control. -

Question 286:

Which of the following categories is included in generally accepted auditing standards?

A. Standards of review.

B. Standards of planning.

C. Standards of fieldwork.

D. Standards of evidence. -

Question 287:

ABC Corp. is an accrual-basis calendar-year corporation with 100,000 shares of voting common stock issued and outstanding as of December 28, 1996. On Friday, December 29, 1996, XYZ surrendered 2,000 shares of ABC stock to ABC in exchange for $33,000 cash. XYZ had no direct or indirect interest in ABC after the stock surrender. Additional information follows:

What amount of income did XYZ recognize from the stock surrender?

A. $33,000 dividend.

B. $25,000 dividend.

C. $18,000 capital gain.

D. $17,000 capital gain. -

Question 288:

In a competitive market, an increase in the minimum wage will likely have the following effects:

A. Firms currently paying above the new minimum wage would generally raise their pay rates (although the new minimum wage creates a new floor for employee wage bargaining purposes).

B. Firms paying at the current minimum wage rate would generally be unaffected if the marginal revenue produced by the lowest paid workers does not exceed the new higher cost of the worker. Many firms would thus be forced to work more efficiently.

C. Total employment will likely decrease in affected industries and generate unemployment. Employers will demand a smaller number of workers while a larger number of workers will be attracted by the higher wage.

D. If a marginally more expensive form of capital is available to substitute for labor (e.g., due to technological advances), firms will reduce their use of labor. -

Question 289:

Gillie, Taft, and Dall are partners in an architectural firm. The partnership agreement is silent about the payment of salaries and the division of profits and losses. Gillie works full-time in the firm, and Taft and Dall each work half time. Taft invested $120,000 in the firm, and Gillie and Dall invested $60,000 each. Dall is responsible for bringing in 50% of the business, and Gillie and Taft 25% each. How should profits of $120,000 for the year be divided?

A. Gillie $60,000, Taft $30,000, Dall $30,000.

B. Gillie $40,000, Taft $40,000, Dall $40,000.

C. Gillie $30,000, Taft $60,000, Dall $30,000.

D. Gillie $30,000, Taft $30,000, Dall $60,000. -

Question 290:

In the first audit of a client, an auditor was not able to gather sufficient evidence about the consistent application of accounting principles between the current and prior year, as well as the amounts of assets or liabilities at the beginning of the current year. This was due to the client's record retention policies. If the amounts in question could materially affect current operating results, the auditor would:

A. Be unable to express an opinion on the current year's results of operations and cash flows.

B. Express a qualified opinion on the financial statements because of a client-imposed scope limitation.

C. Withdraw from the engagement and refuse to be associated with the financial statements.

D. Specifically state that the financial statements are not comparable to the prior year due to an uncertainty.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.