CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 951:

ABC sells to retail stores on credit terms of 2/10, net 30. Daily sales average 150 units at a price of $300 each. Assuming that all sales are on credit and 60 percent of customers take the discount and pay on Day 10 while the rest of the customers pay on Day 30, the amount of Jackson's accounts receivable is:

A. $990,000

B. $900,000

C. $810,000

D. $450,000 -

Question 952:

How should the effect of a change in accounting estimate be accounted for?

A. By restating amounts reported in financial statements of prior periods.

B. By reporting pro forma amounts for prior periods.

C. As a prior period adjustment to beginning retained earnings.

D. In the period of change and future periods if the change affects both. -

Question 953:

In analyzing a company's financial statements, which financial statement would a potential investor primarily use to assess the company's liquidity and financial flexibility?

A. Balance sheet.

B. Income statement.

C. Statement of retained earnings.

D. Statement of cash flows. -

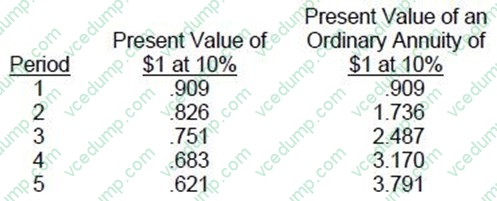

Question 954:

In order to increase production capacity, ABC Industries is considering replacing an existing production machine with a new technologically improved machine effective January 1, 1997. The following information is being considered by ABC Industries.

?The new machine would be purchased for $160,000 in cash. Shipping, installation, and testing would cost an additional $30,000.

?The new machine is expected to increase annual sales by 20,000 units at a sales price of $40 per unit. Incremental operating costs are comprised of $30 per unit in variable costs and total fixed costs of $40,000 per year.

?The investment in the new machine will require an immediate increase in working capital of $35,000. ?ABC uses straight-line depreciation for financial reporting and tax reporting purposes. The new machine has an estimated useful life of

five years and zero salvage value. ?ABC is subject to a 40 percent corporate income tax rate. ABC uses the net present value method to analyze investments and will employ the following factors and rates.

ABC Industries' discounted annual depreciation tax shield for the year 1997 would be:

A. $13,817

B. $15,200

C. $16,762

D. $20,725 -

Question 955:

Fanny and John each own and manage their own companies. Fanny's business is manufacturing freight boxes of all types, and John's business is selling freight boxes to different industries. They decide to combine their expertise and knowledge to produce and sell freight boxes specifically designed for the new airline company that just formed in their city. Which of the following best describes the business formed by the parties?

A. A general partnership.

B. A limited liability partnership.

C. A sole proprietorship.

D. A joint venture. -

Question 956:

ABC Corporation had income before taxes of $60,000 for the year 1991. Included in this amount was depreciation of $5,000, a charge of $6,000 for the amortization of bond discounts, and $4,000 for interest expense. The estimated cash flow for the period is:

A. $66,000

B. $49,000

C. $71,000

D. $65,000 -

Question 957:

FASB Interpretations of Statements of Financial Accounting Standards have the same authority as the FASB:

A. Statements of Financial Accounting Concepts.

B. Emerging Issues Task Force Consensus.

C. Technical Bulletins.

D. Statements of Financial Accounting Standards. -

Question 958:

Gearty and Duffy, certified public accountants, have been engaged to perform a single audit of Sleepy Knoll Township, a local government receiving substantial federal financial assistance for community development and housing assistance. A single audit represents:

A. An audit of annual activity of only federal financial assistance programs over the course of the town's fiscal year.

B. An inception to date audit of only federal financial assistance programs over the course of the grant year specified by the grant award.

C. An audit of the township's financial statements and of compliance with federal regulations relating to federal financial assistance as prescribed by the Single Audit Act and OMB Circular A-133.

D. An audit of the township's financial statements and the fair presentation of the revenues derived from federal financial assistance. -

Question 959:

When auditing an entity's financial statements in accordance with Government Auditing Standards (the Yellow Book), an auditor is required to report on:

A. Noteworthy accomplishments of the program. II. The scope of the auditor's testing of internal controls.

B. I only.

C. II only.

D. Both I and II.

E. Neither I nor II. -

Question 960:

A transaction that is unusual, but not infrequent, should be reported separately as a(an):

A. Extraordinary item, net of applicable income taxes.

B. Extraordinary item, but not net of applicable income taxes.

C. Component of income from continuing operations, net of applicable income taxes.

D. Component of income from continuing operations, but not net of applicable income taxes.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.