CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 961:

Which of the following is a requirement for a small business corporation to elect S corporation status?

A. It has only one class of stock.

B. It has at least one partnership as a shareholder.

C. It has international ownership.

D. It has more than 75 shareholders. -

Question 962:

All of the following are characteristics of the strategic planning process, except the:

A. Emphasis on both the short and long run.

B. Review of the attributes and behavior of the organization's competition.

C. Analysis and review of departmental budgets.

D. Analysis of consumer demand. -

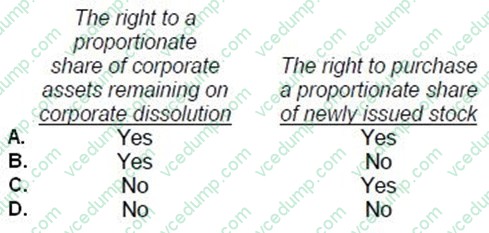

Question 963:

Under the Revised Model Business Corporation Act, when a corporation's bylaws grant stockholders preemptive rights, which of the following rights is(are) included in that grant?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 964:

The selection of the denominator in the return on investment (ROI) formula is critical to the measure's effectiveness. Which denominator is criticized because it combines the effects of operating decisions made at one level of the organization with financing decisions made at another organization level?

A. Total assets available.

B. Total assets employed.

C. Working capital plus other assets.

D. Shareholder's equity. -

Question 965:

In 1990, ABC Co. changed from the individual item approach to the aggregate approach in applying the lower of FIFO cost or market to inventories. The cumulative effect of this change should be reported in ABC's financial statements as a:

A. Retrospective adjustment on the retained earnings statement, with separate disclosure.

B. Component of income from continuing operations, with separate disclosure.

C. Component of income from continuing operations, without separate disclosure.

D. Component of income after continuing operations, with separate disclosure. -

Question 966:

Which of the following would an auditor most likely use in determining the auditor's preliminary judgment about materiality?

A. The anticipated sample size of the planned substantive tests.

B. The entity's annualized interim financial statements.

C. The results of the internal control questionnaire.

D. The contents of the management representation letter. -

Question 967:

A recession can be caused by:

A. An increase in aggregate demand.

B. A decrease in aggregate supply.

C. A decrease in aggregate demand.

D. Both "b" and "c". -

Question 968:

On January 2, 20X5, to better reflect the variable use of its only machine, ABC, Inc. elected to change its method of depreciation from the straight-line method to the units of production method. The original cost of the machine on January 2,

20X3, was $50,000, and its estimated life was 10 years. ABC estimates that the machine's total life is 50,000 machine hours. Machine hours usage was 8,500 during 20X4 and 3,500 during 20X3.

ABC's income tax rate is 30%. ABC should report the accounting change in its 20X5 financial statements as a(n):

A. Cumulative effect of a change in accounting principle of $2,000 in its income statement.

B. Adjustment to beginning retained earnings of $2,000.

C. Cumulative effect of a change in accounting principle of $1,400 in its income statement.

D. None of the above. -

Question 969:

The annual tax depreciation expense on an asset reduces income taxes by an amount equal to:

A. The firm's average tax rate times the depreciation amount.

B. One minus the firm's average tax rate times the depreciation amount.

C. The firm's marginal tax rate times the depreciation amount.

D. One minus the firm's marginal tax rate times the depreciation amount. -

Question 970:

An auditor decides to issue a qualified opinion on an entity's financial statements because a major inadequacy in its computerized accounting records prevents the auditor from applying necessary procedures. The opinion paragraph of the auditor's report should state that the qualification pertains to:

A. A client-imposed scope limitation.

B. A departure from generally accepted auditing standards.

C. The possible effects on the financial statements.

D. Inadequate disclosure of necessary information.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.