CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 811:

ABC Manufacturing Corporation uses the standard Economic Order Quantity (EOQ) model. If the EOQ for Product A is 200 units and ABC maintains a 50-unit safety stock for the item, what is the average inventory of Product A?

A. 250 units.

B. 150 units.

C. 125 units.

D. 100 units. -

Question 812:

In auditing a client's retained earnings account, an auditor should determine whether there are any restrictions on retained earnings that result from loans, agreements, or state law. This procedure is designed to corroborate management's financial statement assertions with respect to:

A. Transactions and events.

B. Account balances.

C. Presentation and disclosure.

D. Audit risk and materiality. -

Question 813:

The imputed interest rate used in the residual income approach to performance evaluation can best be described as the:

A. Historical weighted average cost of capital for the company.

B. Target return on investment set by the company's management.

C. Average return on investments for the company over the last several years.

D. Marginal after-tax cost of capital on new equity capital. -

Question 814:

During a recession:

A. Output (real GDP) will be increasing.

B. The natural rate of unemployment will increase dramatically.

C. Potential output will exceed actual output.

D. Actual output will exceed potential output. -

Question 815:

If demand is price elastic:

A. An increase in price will result in a decline in total revenue.

B. An increase in price will result in a decline the quantity demanded that is less than the increase in price.

C. An increase in price will result in an increase in total revenue.

D. An increase in price will have no effect on total revenue. -

Question 816:

During 2001, Adler had the following cash receipts:

What is the total amount that must be included in gross income on Adler's 2001 income tax return?

A. $18,000

B. $18,400

C. $19,500

D. $19,900 -

Question 817:

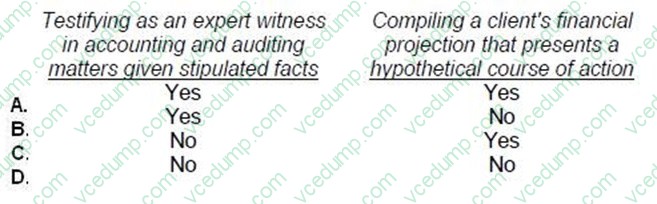

A CPA in public practice is required to comply with the provisions of the Statements on Standards for Attestation Engagements (SSAE) when:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 818:

ABC Industries is the leader in its market for producing high-quality cat food for cats that require special diets. While it has been able to sustain competitive advantage for years, ABC's management has implemented a strategic framework that focuses on why the firm has been so successful in its market. ABC Industries has implemented which type of strategic framework?

A. Industry structure analysis.

B. Core competencies analysis.

C. Segmentation analysis.

D. None of the above. -

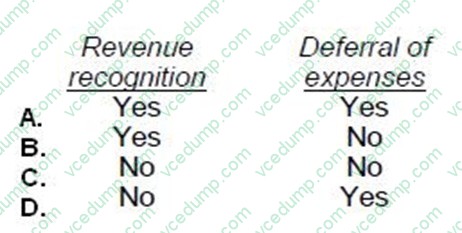

Question 819:

A development stage enterprise should use the same generally accepted accounting principles that apply to established operating enterprises for: A. Option A

B. Option B

C. Option C

D. Option D

Correct Answer. A -

Question 820:

Strategic planning, as practiced by most modern organizations, includes all of the following, except:

A. Top-level management participation.

B. Strategies that will help in achieving long-range goals.

C. Analysis of the current month's actual variances from budget.

D. Identification of long-term key variables including external influences.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.