CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 801:

An independent auditor asked a client's internal auditor to assist in preparing a standard financial institution confirmation request for a payroll account that had been closed during the year under audit. After the internal auditor prepared the form, the controller signed it and mailed it to the bank. What was the major flaw in this procedure?

A. The internal auditor did not sign the form.

B. The form was mailed by the controller.

C. The form was prepared by the internal auditor.

D. The account was closed, so the balance was zero. -

Question 802:

Which of the following is incorrect with regard to value chain analysis?

A. Value chain analysis must be used in conjunction with the strategic plan of the organization.

B. Value chain analysis is critical to assessing the competitive advantage of a firm.

C. Value chain analysis is a strategic tool that assists the firm in determining how important the perceived value of the buyers is with respect to the market the firm operates in.

D. The value chain starts with the firm and goes all the way through to the end users of the product. -

Question 803:

Of the following items, the one item that would not be considered in evaluating the adequacy of the budgeted annual operating income for a company is:

A. Return on assets.

B. Long-range profit objectives.

C. Industry average for earnings on sales.

D. Internal rate of return. -

Question 804:

ABC, Inc. is interested in measuring its overall cost of capital and has gathered the following data. Under the terms described below, the company can sell unlimited amounts of all instruments.

?ABC can raise cash by selling $1,000, 8 percent, 20-year bonds with annual interest payments. In selling the issue, an average premium of $30 per bond would be received, and the firm must pay floatation costs of $30 per bond. The after-tax cost of funds is estimated to be 4.8 percent. ?ABC can sell 8 percent preferred stock at par value, $105 per share. The cost of issuing and selling the preferred stock is expected to be $5 per share. ?ABC' common stock is currently selling for $100 per share. The firm expects to pay cash dividends of $7 per share next year, and the dividends are expected to remain constant. The stock will have to be underpriced by $3 per share, and floatation costs are expected to amount to $5 per share. ?ABC expects to have available $100,000 of retained earnings in the coming year; once these retained earnings are exhausted, the firm will use new common stock as the form of common stock equity financing. ?ABC' preferred capital structure is: Long-term debt 30% Preferred stock 20 Common stock 50

If ABC, Inc. needs a total of $1,000,000, the firm's weighted-average cost of capital would be:

A. 6.8 percent.

B. 4.8 percent.

C. 6.5 percent.

D. 9.1 percent. -

Question 805:

The ABC Corporation is considering the acquisition of a new machine. The machine can be purchased for $90,000; it will cost $6,000 to transport to ABC's plant and $9,000 to install. It is estimated that the machine will last 10 years, and it is expected to have an estimated salvage value of $5,000. Over its 10-year life, the machine is expected to produce 2,000 units per year with a selling price of $500 and combined material and labor costs of $450 per unit. Federal tax regulations permit machines of this type to be depreciated using the straight-line method over 5 years with no estimated salvage value. ABC has a marginal tax rate of 40 percent.

What is the net cash flow for the tenth year of the project that ABC Corporation should use in a capital budgeting analysis?

A. $81,000

B. $68,400

C. $63,000

D. $60,000 -

Question 806:

All of the following are the rates used in net present value analysis, except for the:

A. Cost of capital.

B. Hurdle rate.

C. Discount rate.

D. Accounting rate of return. -

Question 807:

The articles of organization for a limited liability company must contain everything, except the following:

A. The name of the entity that includes some indication it is a LLC.

B. The name and address of the registered agent.

C. Number of shares authorized and issued.

D. If the company is to be manager managed, a statement to that effect. -

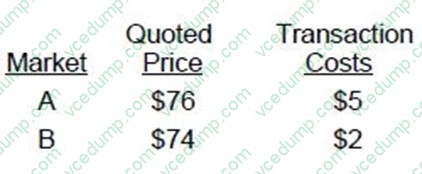

Question 808:

There are multiple active markets for a financial asset with different observable market prices:

There is no principal market for the financial asset. What is the fair value of the asset?

A. $71

B. $72

C. $74

D. $76 -

Question 809:

When applying value chain analysis, a firm asks it accounting department to perform an analysis of the sources of profits and costs of activities that exist within the firm. The firm is performing which form of value chain analysis?

A. Internal differentiation analysis.

B. Internal costs analysis.

C. Vertical linkage analysis.

D. None of the above. -

Question 810:

ABC Industries limits its operations to exports to foreign countries. What can be said about ABC's exposures to exchange rate risk?

A. ABC is subject to potential transaction, economic and translation exposures to exchange rate risk.

B. ABC is subject to potential transaction and economic exposures to exchange rate risk.

C. ABC is subject to economic and translation exposures to exchange rate risk.

D. ABC is subject transaction and translation exposures to exchange rate risk.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.