CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 821:

Which of the following internal control procedures most likely addresses the completeness assertion for inventory?

A. Work in process account is periodically reconciled with subsidiary records.

B. Employees responsible for custody of finished goods do not perform the receiving function.

C. Receiving reports are prenumbered and periodically reconciled.

D. There is a separation of duties between payroll department and inventory accounting personnel. -

Question 822:

As a company becomes more conservative in its working capital policy, it would tend to have a(n):

A. Decrease in its acid-test ratio.

B. Increase in the ratio of current assets to units of output.

C. Increase in funds invested in common stock and a decrease in funds invested in marketable securities.

D. Decrease in its level of permanent working capital. -

Question 823:

Which of the following procedures would an auditor most likely perform in obtaining evidence about subsequent events?

A. Determine that changes in employee pay rates after year-end were properly authorized.

B. Recompute depreciation charges for plant assets sold after year-end.

C. Inquire about payroll checks that were recorded before year-end but cashed after year-end.

D. Investigate changes in long-term debt occurring after year-end. -

Question 824:

When an accountant issues to an underwriter a comfort letter containing comments on data that have not been audited, the underwriter most likely will receive:

A. Negative assurance on capsule information.

B. Positive assurance on supplementary disclosures.

C. A limited opinion on "pro forma" financial statements.

D. A disclaimer on prospective financial statements. -

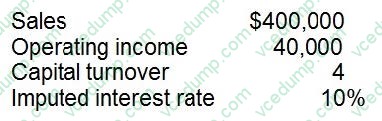

Question 825:

The following selected data pertain to the Darwin Division of ABC Co. for 1994:

What was Darwin's 1994 residual income?

A. $0

B. $4,000

C. $10,000

D. $30,000 -

Question 826:

In testing controls over cash disbursements, an auditor most likely would determine that the person who signs checks also:

A. Reviews the monthly bank reconciliation.

B. Returns the checks to accounts payable.

C. Is denied access to the supporting documents.

D. Is responsible for mailing the checks. -

Question 827:

This question will represent a statement, question, excerpt, or comment taken from various parts of an auditor's documentation file. Letter choices A-P represent a list of the likely sources of the statement, question, excerpt, or comment.

Select, as the best answer for each item, the most likely source. Select only one source for each item.

Our audit is designed to provide reasonable assurance of detecting misstatements that, in our judgment, could have a material effect on the financial statements taken as a whole. Consequently, our audit will not necessarily detect all

misstatements that exist due to error, fraudulent financial reporting, or misappropriation of assets.

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements.

B. Auditor's communications on significant deficiencies in internal control.

C. Audit inquiry letter to legal counsel.

D. Lawyer's response to audit inquiry letter.

E. Communication from those charged with governance to the auditor.

F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies in internal control).

G. Report on the application of accounting principles.

H. Auditor's engagement letter.

I. Letter for underwriters.

J. Accounts receivable confirmation request. K. Request for bank cutoff statement. L. Explanatory paragraph of an auditor's report on financial statements. M. Partner's engagement review notes. N. Management representation letter. O. Successor auditor's communication with predecessor auditor. P. Predecessor auditor's communication with successor auditor. -

Question 828:

Which of the following would most likely cause real GDP to increase the most:

A. A rise in interest rates and a rise in input costs.

B. A fall in interest rates and a fall in input costs.

C. A rise in wealth and a rise in interest rates.

D. A rise in consumer confidence and a fall in government spending. -

Question 829:

When single-year financial statements are presented, an auditor ordinarily would express an unqualified opinion in an unmodified report if the:

A. Auditor is unable to obtain audited financial statements supporting the entity's investment in a foreign affiliate.

B. Entity declines to present a statement of cash flows with its balance sheet and related statements of income and retained earnings.

C. Auditor wishes to emphasize an accounting matter affecting the comparability of the financial statements with those of the prior year.

D. Prior year's financial statements were audited by another CPA whose report, which expressed an unqualified opinion, is not presented. -

Question 830:

Which of the following matters most likely would be included in a management representation letter?

A. An assessment of the risk factors concerning the misappropriation of assets.

B. An evaluation of the litigation that has been filed against the entity.

C. A confirmation that the entity has complied with contractual agreements.

D. A statement that all material internal control weaknesses have been corrected.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.