AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 831:

The effect of a material transaction that is infrequent in occurrence but not unusual in nature should be presented separately as a component of income from continuing operations when the transaction results in

a:

A. Option A B. Option B C. Option C D. Option D

A. Option A Choice "a" is correct, Yes - Yes. A material transaction that is "infrequent in occurrence" but not "unusual in nature" should be presented separately as a component of "income from continuing operations" when the transaction results in a gain or loss.

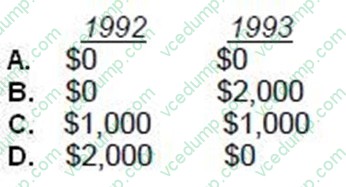

Question 832:

Smith, an individual calendar-year taxpayer, purchased 100 shares of ABC Co. common stock for $15,000 on December 15, 1992, and an additional 100 shares for $13,000 on December 30, 1992. On January 3, 1993, Smith sold the shares purchased on December 15, 1992, for $13,000. What amount of loss from the sale of ABC's stock is deductible on Smith's 1992 and 1993 income tax returns?

A. Option A B. Option B C. Option C D. Option D

A. Option A Choice "a" is correct. In 1992, no sale of stock occurred so there would be no loss. In 1993, there is a $2,000 loss realized ($15,000 basis less $13,000 received), but it is not deductible because it is a wash sale. A wash sale occurs when a taxpayer sells stock at a loss and invests in substantially identical stock within 30 days before or after the sale. In this case, Smith reinvested in an additional 100 shares four days prior to selling 100 shares of the same stock at a loss. The $2,000 disallowed loss would, however, increase the basis of the new shares by $2,000. Choice "b" is incorrect. The $2,000 loss realized in 1993 is disallowed under the wash sale rules. Choice "c" is incorrect. In 1992, there is no loss since no shares were sold. In 1993, the $2,000 loss is disallowed under the wash sale rules. Choice "d" is incorrect. In 1992, there is no possible loss since no shares were sold.

Question 833:

A statement of cash flows for a development stage enterprise:

A. Is the same as that of an established operating enterprise and, in addition, shows cumulative amounts from the enterprise's inception. B. Shows only cumulative amounts from the enterprise's inception. C. Is the same as that of an established operating enterprise, but does not show cumulative amounts from the enterprise's inception. D. Is not presented.

A. Is the same as that of an established operating enterprise and, in addition, shows cumulative amounts from the enterprise's inception. Rule: Development stage enterprises should present financial statements in accordance with GAAP and make additional disclosures such as cumulative amounts from inception for: net losses, deficits, sales, expenses, and cash flows and supplementary data. Choice "a" is correct, per the rule shown above. Choice "b" is incorrect. Current amounts are shown as well as cumulative amounts. Choice "c" is incorrect. Cumulative amounts from inception are shown. Choice "d" is incorrect. A statement of cash flows is required.

Question 834:

An auditor would most likely verify the interest earned on bond investments by:

A. Vouching the receipt and deposit of interest checks. B. Confirming the bond interest rate with the issuer of the bonds. C. Recomputing the interest earned on the basis of face amount, interest rate, and period held. D. Testing the internal controls over cash receipts.

C. Recomputing the interest earned on the basis of face amount, interest rate, and period held. Choice "c" is correct. Recomputing the interest earned is the most likely method of auditing interest earned on bond investments. Choice "a" is incorrect. Vouching cash receipts would only verify the recording of checks received. This may not be the same as interest earned, since interest is accrued between cash payment dates. Choice "b" is incorrect. Confirmation of the bond interest rate with the issuer is not sufficient, as the rate still needs to be applied based on face amount and period held. Choice "d" is incorrect. Internal control testing of cash receipts would not provide evidence that earned interest was properly recorded, since interest is accrued between cash payment dates.

Question 835:

Which of the following fraudulent activities most likely could be perpetrated due to the lack of effective internal controls in the revenue cycle?

A. Merchandise received is not promptly reconciled to the outstanding purchase order file. B. Obsolete items included in inventory balances are rarely reduced to the lower of cost or market value. C. The write-off of receivables by personnel who receive cash permits the misappropriation of cash. D. Fictitious transactions are recorded that cause an understatement of revenue and overstatement of receivables.

C. The write-off of receivables by personnel who receive cash permits the misappropriation of cash. Choice "c" is correct. The function of cash receipts is part of the treasurer's department and should be separate from the role of writing off receivables. Failure to separate the recordkeeping function from the custodial function allows an individual to misappropriate cash and then cover up the theft by writing off the related receivable balance. Choice "a" is incorrect. Internal controls in the revenue cycle typically relate to sales, receivables, and cash, not to the purchase and receipt of goods. Choice "b" is incorrect. Internal controls in the revenue cycle typically relate to sales, receivables, and cash, not to inventory valuation. Choice "d" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same; either both would be overstated (the most likely case) or both would be understated.

Question 836:

Unless there is an agreement to the contrary, the voting power of members in a limited liability company is determined by:

A. Each member's salary. B. Each member's share of profits. C. When the member was admitted to the company. D. Each member's capital contribution.

D. Each member's capital contribution. Choice "d" is correct. Rule: Absent an agreement otherwise, all members generally participate in management, and their voting strength is determined in proportion to ownership interest. This is calculated by comparing each member's capital contribution to that of the other members. Choices "a", "b", and "c" are incorrect, per the above rule.

Question 837:

When auditing an entity's financial statements in accordance with Government Auditing Standards, an auditor should prepare a written report of the audit: A. Identification of the causes of performance problems and recommendations for actions to improve operations.

B. Understanding of internal control and assessment of control risk.

C. Field work and procedures that substantiated the auditor's specific findings and conclusions.

D. Opinion on the entity's attainment of the goals and objectives specified by applicable laws and regulations.

Correct Answer. B

B Choice "b" is correct. Government Auditing Standards require that the auditor issue a written report on internal control in all audits. As part of this reporting requirement, the auditor must describe the scope of the auditor's work in obtaining an understanding of internal control and his or her assessment of control risk. Choice "a" is incorrect. In the report, the auditor would identify significant deficiencies (reportable conditions) and material weaknesses (not performance problems) found in the examination of the entity's internal control. Choice "c" is incorrect. A report on fieldwork and procedures that substantiated the auditor's specific findings and conclusions would not be prepared as part of a GAGAS audit. Choice "d" is incorrect. The objective of the audit of the financial statements is to provide an opinion on the financial statements, not on the entity's attainment of goals and objectives.

Question 838:

Before applying substantive tests to the details of asset accounts at an interim date, an auditor should assess:

A. Control risk at a low level. B. Inherent risk at a high level. C. The difficulty in controlling the incremental audit risk. D. Materiality for the accounts tested as insignificant.

C. The difficulty in controlling the incremental audit risk. Choice "c" is correct. Before performing substantive tests at an interim date, the auditor must assess the difficulty in controlling the incremental audit risk from the interim date (on which the substantive procedures are performed) to the year-end date (on which an opinion is rendered). Choice "a" is incorrect. The auditor would not have to assess control risk at a low level in order to perform substantive tests at interim. It may simply be more efficient to perform a substantive audit. As long as the balances tested at interim are reasonably predictable with respect to amount, relative significance and composition, the account may be tested at interim. Choice "b" is incorrect. Generally, inherent risk should be low in order to test substantively at interim. Choice "d" is incorrect. If the materiality level for those accounts to be tested is insignificant, then the auditor probably would not perform any substantive testing, since it is unlikely that a material error exists in an insignificant balance.

Question 839:

During 1990, ABC Company's current assets increased by $120, current liabilities decreased by $50, and net working capital:

A. Increased by $70. B. Decreased by $170. C. Increased by $170. D. Decreased by $70.

C. Increased by $170. Explanation Explanation/Reference:Choice "c" is correct. Net working capital is the difference between current assets and current liabilities. Because current assets went up $120 and current liabilities down by $50, the net effect is an increase in net working capital of $170. Therefore, working capital has increased $170,000. Choices "a", "b", and "d" are incorrect, per the above calculation.

Question 840:

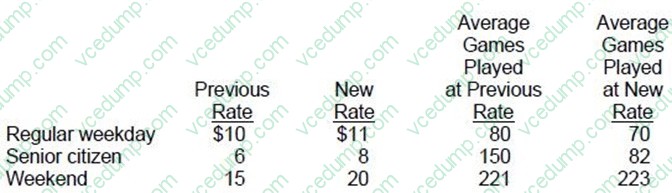

ABC Golf Course has raised green fees to a nine-hole game due to an increase in demand.

Which of the following is correct?

A. The regular weekday and weekend demand is inelastic. B. The regular weekday and weekend demand is elastic. C. The senior citizen and weekend demand is inelastic. D. The senior citizen demand is elastic and weekend demand is inelastic.

D. The senior citizen demand is elastic and weekend demand is inelastic. Choice "d" is correct. Demand is elastic if a decline in price (P) results in an increase in total revenue (TR); or if an increase in P results in a decline in TR. On the other hand, if demand is inelastic, a decline in P will result in a decline in TR or an increase in P will result in an increase in TR. First, the total revenues at both the new and the previous rate must be computed. The (new or previous) rate* average games played (AGP) = the total revenue. As a result, TR at the previous rate (PR) is 800 for regular weekday (RW), 900 for senior citizen (SC), and 3315 for the weekend (WE). TR at the new rate (NR) is 770 for RW, 656 for SC, and 4460 for WE. So, demand for RW and SC is elastic because the increase in P results in a decline in total revenue. The demand for WE is inelastic because the increase in P results in an increase in TR. As a result, choices "a", "b", and "c" are incorrect. Note: if TR remains constant after a change in P, the demand is unit elastic.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.