CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 661:

Fred Berk bought a plot of land with a cash payment of $40,000 and a mortgage of $50,000. In addition, Berk paid $200 for a title insurance policy. Berk's basis in this land is:

A. $40,000

B. $40,200

C. $90,000

D. $90,200 -

Question 662:

In inventory management, the safety stock will tend to increase if the:

A. Carrying cost increases.

B. Cost of running out of stock decreases.

C. Variability of lead-time increases.

D. Fixed order cost decreases. -

Question 663:

ABC Corp. failed to accrue warranty costs of $50,000 in its December 31, 1992, financial statements. In addition, a $30,000 change from straight-line to accelerated depreciation was made at the beginning of 1993. Both the $50,000 and the $30,000 are net of related income taxes. What amount should ABC report as prior period adjustments in 1993?

A. $0

B. $30,000

C. $50,000

D. $80,000 -

Question 664:

Which of the following would not be considered a significant audit finding that should be included in audit documentation?

A. Retirement of the accounts payable manager and subsequent hiring of a replacement.

B. Discovery of a material sale recorded in the current year that properly belonged in the subsequent year.

C. Determination that there is substantial doubt about the entity's ability to continue as a going concern.

D. Implementation of a new accounting standard to account for a complex and unusual transaction. -

Question 665:

An auditor should trace corporate stock issuances and treasury stock transactions to the:

A. Numbered stock certificates.

B. Articles of incorporation.

C. Transfer agent's records.

D. Minutes of the board of directors. -

Question 666:

Which one of the following is most likely to accompany a reduction in aggregate demand?

A. An increase in the price level.

B. A decrease in employment.

C. An increase in real GDP.

D. A decrease in the unemployment rate. -

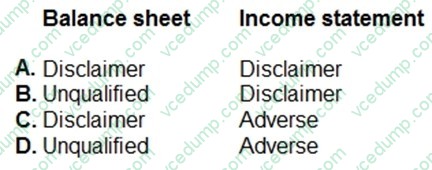

Question 667:

Park, CPA, was engaged to audit the financial statements of ABC Co., a new client, for the year ended December 31, 20X3. Park obtained sufficient audit evidence for all of ABC's financial statement items except ABC's opening inventory. Due to inadequate financial records, Park could not verify ABC's January 1, 20X3, inventory balances. Park's opinion on ABC's 20X3 financial statements most likely will be:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 668:

On January 2, 1989, ABC Co. purchased a machine for $264,000 and depreciated it by the straight-line method using an estimated useful life of eight years with no salvage value. On January 2, 1992, ABC determined that the machine had a useful life of six years from the date of acquisition and will have a salvage value of $24,000. An accounting change was made in 1992 to reflect the additional data. The accumulated depreciation for this machine should have a balance at December 31, 1992, of:

A. $176,000

B. $160,000

C. $154,000

D. $146,000 -

Question 669:

An accountant compiles unaudited financial statements that are not expected to be used by a third party. The accountant may decline to issue a compilation report provided:

A. Each page of the financial statements is clearly marked to restrict its use. II. A written engagement letter is used to document the understanding with the client. III. A written representation letter is obtained from the client's management.

B. Option A

C. Option B

D. Option C

E. Option D -

Question 670:

If the elasticity of demand for a normal good is estimated to be 1.5, then a 10% reduction in its price would cause:

A. Total revenue to fall by 10%.

B. Total revenue to fall by 15%.

C. Quantity demanded to rise by 15%.

D. Demand to decrease by 10%.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.