CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 671:

In a decision analysis situation, which one of the following costs is generally not relevant to the decision?

A. Incremental cost.

B. Avoidable cost.

C. Historical cost.

D. Opportunity cost. -

Question 672:

On January 1, 20X1, ABC Corp. purchased a machine having an estimated useful life of 10 years and no salvage. The machine was depreciated by the double declining balance method for both financial statement and income tax reporting. On January 1, 20X6, ABC changed to the straight-line method for financial statement reporting but not for income tax reporting. Accumulated depreciation at December 31, 20X5, was $560,000. If the straight-line method had been used, the accumulated depreciation at December 31, 20X5, would have been $420,000. ABC's enacted income tax rate for 20X6 and thereafter is 30%. The amount shown in the 20X6 income statement for the cumulative effect of changing to the straight-line method should be:

A. $98,000 debit.

B. $98,000 credit.

C. $140,000 credit.

D. $0. -

Question 673:

Ordinarily, the predecessor auditor permits the successor auditor to review the predecessor's audit documentation relating to:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 674:

The standard report issued by an accountant after reviewing the financial statements of a nonissuer should state that:

A. A review is limited to presenting in the form of financial statements information that is the representation of management.

B. A review consists of inquiries of company personnel and analytical procedures applied to financial data.

C. The accountant does not express an opinion or any other form of assurance on the financial statements.

D. The accountant did not obtain an understanding of the entity's internal control or assess control risk. -

Question 675:

Which of the following statements is not true of the test data approach to testing an accounting system?

A. Test data are processed by the client's computer programs under the auditor's control.

B. The test data need consist of only those valid and invalid conditions that interest the auditor.

C. Only one transaction of each type need be tested.

D. The test data must consist of all possible valid and invalid conditions. -

Question 676:

ABC Corp. was a development stage enterprise from its inception on September 1, 1987 to December 31, 1988. The following information was taken from ABC's accounting records for the above period:

For the period September 1, 1987 to December 31, 1988, what amount should ABC report as net loss?

A. $ 50,000 B. $150,000

C. $350,000

D. $450,000 -

Question 677:

On January 2, 1991, ABC, Inc. agreed to pay its former president $300,000 under a deferred compensation arrangement. ABC should have recorded this expense in 1990 but did not do so. ABC's reported income tax expense would have been $70,000 lower in 1990 had it properly accrued this deferred compensation in its December 31,1991, financial statements, ABC should adjust the beginning balance of its retained earnings by a:

A. $230,000 credit.

B. $230,000 debit.

C. $300,000 credit.

D. $370,000 debit. -

Question 678:

The collection of accounts receivable can be accelerated by the use of:

A. Turnaround documents.

B. A lockbox system.

C. Bank drafts.

D. Remittance advices. -

Question 679:

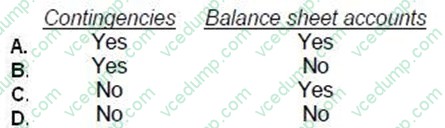

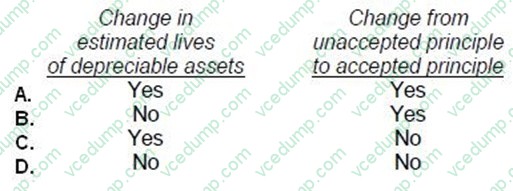

Which of the following should be reported as a prior period adjustment?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 680:

Lake, CPA, is auditing the financial statements of ABC Co. ABC uses the XYZ, Inc. to process its payroll transactions. XYZ's financial statements are audited by Cope, CPA, who recently issued a report on XYZ's internal control structure. Lake is considering Cope's report on XYZ's internal control structure in assessing control risk on the ABC engagement. What is Lake's responsibility concerning making reference to Cope as a basis, in part, for Lake's own opinion?

A. Lake may refer to Cope only if Lake is satisfied as to Cope's professional reputation and independence.

B. Lake may refer to Cope only if Lake relies on Cope's report in restricting the extent of substantive tests.

C. Lake may refer to Cope only if Lake's report indicates the division of responsibility.

D. Lake may not refer to Cope under the circumstances above.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.