AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 641:

The length of time required to recover the initial cash outlay of a capital project is determined by using the:

A. Discounted cash flow method. B. Payback method. C. Net present value method. D. Accounting rate of return method.

B. Payback method. Choice "b" is correct. The payback method measures the time required to recover the initial investment. Choice "a" is incorrect. Discounted cash flows are used for several methods of capital budgeting; this is a generic term. Choice "c" is incorrect. The NPV method does not measure the length of time required to recover the initial cash outlay. Choice "d" is incorrect. The accounting rate of return does not measure the time to recover the initial investment.

Question 642:

The CFO of a company is concerned about the company's accounts receivable turnover ratio. The company currently offers customers terms of 3/10, net 30. Which of the following strategies would most likely improve the company's accounts receivable turnover ratio?

A. Pledging the accounts receivable to a finance company. B. Changing customer terms to 1/10, net 30. C. Entering into a factoring agreement with a finance company. D. Changing customer terms to 3/20, net 30.

C. Entering into a factoring agreement with a finance company. Choice "c" is correct. The accounts receivable turnover ratio is expressed as Sales / Accounts Receivable. A reduction in accounts receivable would serve to improve (increase) the turnover ratio. Factoring (selling) receivables would serve to reduce the amount of accounts receivable (indicating more rapid collections) thereby increasing (improving) the company's accounts receivable. Choice "a" is incorrect. Pledging accounts receivable does not impact either sales or accounts receivable. There would be no improvement in the accounts receivable turnover ratio. Choice "b" is incorrect. Changing the customer terms from 3/10, net 30 to 1/10, net 30 would actually reduce discount incentives to pay timely. Accounts receivable would likely remain the same or be higher. There would be no improvement in the company's accounts receivable turnover ratio. Choice "d" is incorrect. Changing the customer terms from 3/10, net 30 to 3/20, net 30 would actually reduce incentives to pay timely by increasing the amount of time in which the customer could capitalize on the discount. Accounts receivable would likely remain the same or be higher. There would be no improvement in the company's accounts receivable turnover ratio.

Question 643:

Which of the following controls most likely would give the greatest assurance that securities held as investments are safeguarded?

A. There is no access to securities between the year-end and the date of the auditor's security count. B. Proceeds from the sale of investments are received by an employee who does not have access to securities. C. Investment acquisitions are authorized by a member of the Board of Directors before execution. D. Access to securities requires the signatures and presence of two designated officials.

D. Access to securities requires the signatures and presence of two designated officials. Choice "d" is correct. Requiring the signatures and presence of two designated officials in order to gain access to securities is an internal control that provides assurance regarding the safeguarding of securities. Choice "a" is incorrect. Having no access to securities between the year-end and the date of the auditor's security count would assure that no securities are added or taken away before the auditor counts them, but it would not ensure that securities are safeguarded for the entire year. Choice "b" is incorrect. Proceeds from the sale of investments should be received by an employee who does not have access to securities, but this control does not prevent the theft of investments that are not sold. Choice "c" is incorrect. Requiring authorization from a member of the board of directors before execution assures that investment purchases are approved and consistent with the financial philosophy of the organization (level of financial risk that the company is willing to accept), but this approval does not provide assurance that the assets will be safeguarded.

Question 644:

Dough Distributors has decided to increase its daily muffin purchases by 100 boxes. A box of muffins costs $2 and sells for $3 through regular stores. Any boxes not sold through regular stores are sold through Dough's thrift store for $1. Dough assigns the following probabilities to selling additional boxes:

What is the expected value of Dough's decision to buy 100 additional boxes of muffins?

A. $28 B. $40 C. $52 D. $68

C. $52 Choice "c" is correct. The expected value of a decision is computed by multiplying the probability of each outcome by its value or profit. Each outcome is then added. There is a 60% probability that Dough will sell 60 of the 100 additional boxes through regular stores and that means that Dough would have a 60% chance of making a profit of $20 (60 boxes at a $1 profit ($3 - $2) sold through the regular stores and 40 boxes at a $1 loss ($1 - $2) sold through the thrift stores). There is a 40% probability that Dough will have a profit of $40 (100 boxes at a $1 profit through the regular store sales and zero boxes sold at a loss through the thrift store). Choice "a" is incorrect. The expected value of a decision is computed by multiplying the probability of each outcome by its value or profit. Choice "b" is incorrect. The expected value of a decision is computed by multiplying the probability of each outcome by its value or profit. Choice "d" is incorrect. The expected value of a decision is computed by multiplying the probability of each outcome by its value or profit.

Question 645:

Generally, a merger of two corporations requires:

A. That a special meeting be held and that notice and copy of the merger plan be given to all stockholders of both corporations. B. Unanimous approval of the merger plan by the stockholders of both corporations. C. Unanimous approval of the merger plan by the boards of both corporations. D. That all liabilities owed by the absorbed corporation be paid before the merger.

A. That a special meeting be held and that notice and copy of the merger plan be given to all stockholders of both corporations. Choice "a" is correct. The merger of two corporations requires that a special meeting be held and that notice and copy of the merger plan be given to all stockholders of both companies. A merger generally requires the approval of both the directors and stockholders. Choice "b" is incorrect. While the stockholders' approval is required, in most states a majority vote is required; no state requires a unanimous vote. Choice "c" is incorrect. While the board's approval is required, a majority vote and not a unanimous vote is required. Choice "d" is incorrect. There is no requirement that all liabilities owed by the absorbed corporation be paid before the merger because the merged corporation becomes obligated to pay such liabilities upon the merger.

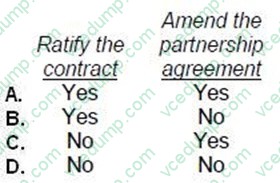

Question 646:

When a partner in a general partnership lacks actual or apparent authority to contract on behalf of the partnership, and the party contracted with is aware of this fact, the partnership will be bound by the contract if the other partners:

A. Option A B. Option B C. Option C D. Option D

B. Option B Choice "b" is correct. "Yes - No." Rule: The authority of partners is governed by agency law. Under agency law, a principal is not bound to the third party unless the agent had actual authority or apparent authority. When the agent has no actual authority and no apparent authority, the principal (in this case the partnership) will only be liable if it chooses to adopt the agreement (i.e., ratify). Rule: Amending the partnership agreement (presumably to grant authority) will not cause the partnership to be bound because authority must exist at the time the contract is made or the partnership must ratify the contract. Choices "a", "c", and "d" are incorrect, per the above rules.

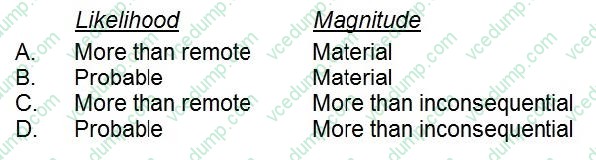

Question 647:

For a nonissuer, a control deficiency would be considered a significant deficiency when the likelihood and magnitude of potential financial statement misstatements are:

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the entity's ability to initiate, authorize, record, process, or report financial data reliably in accordance with GAAP such that there is more than a remote likelihood that a misstatement of the entity's financial statements that is more than inconsequential will not be prevented or detected. Choices "a", "b", and "d" are incorrect, based on theabove.

Question 648:

A change in credit policy has caused an increase in sales, an increase in discounts taken, a decrease in the amount of bad debts, and a decrease in the investment in accounts receivable. Based upon this information, the company's:

A. Average collection period has decreased. B. Percentage discount offered has decreased. C. Accounts receivable turnover has decreased. D. Working capital has increased.

A. Average collection period has decreased. Choice "a" is correct. Average collection period has decreased due to a change in credit policy that has caused: 1. Increase in sales, 2. Increase in discounts taken, 3. Decrease in the amount of bad debt; and 4. Decrease in the investment in accounts receivable Choice "b" is incorrect. Percentage discount offered has probably increased, as discounts taken has increased. Choice "c" is incorrect. Accounts receivable turnover has increased, as sales are up and accounts receivable are down. Choice "d" is incorrect. Change in gross profit and working capital is not determinable from these facts.

Question 649:

Negative confirmation of accounts receivable is less effective than positive confirmation of accounts receivable because:

A. A majority of recipients usually lack the willingness to respond objectively. B. Some recipients may report incorrect balances that require extensive follow-up. C. The auditor cannot infer that all nonrespondents have verified their account information. D. Negative confirmations do not produce audit evidence that is statistically quantifiable.

C. The auditor cannot infer that all nonrespondents have verified their account information. Choice "c" is correct. Negative confirmation of accounts receivable is less effective than positive confirmation of accounts receivable because the auditor cannot infer that all nonrespondents have verified their account information. Choice "a" is incorrect. Both positive and negative confirmations are equally affected by recipients' lack of willingness to respond objectively. Choice "b" is incorrect. Both positive and negative confirms are equally affected by recipients' reporting of incorrect balances. Choice "d" is incorrect. Negative confirmations returned do produce information (e.g., errors noted in accounts) that can be statistically quantifiable.

Question 650:

Which of the following audit procedures would an auditor most likely perform to test controls relating to management's assertion concerning the completeness of sales transactions?

A. Verify that extensions and footings on the entity's sales invoices and monthly customer statements have been recomputed. B. Inspect the entity's reports of prenumbered shipping documents that have not been recorded in the sales journal. C. Compare the invoiced prices on prenumbered sales invoices to the entity's authorized price list. D. Inquire about the entity's credit granting policies and the consistent application of credit checks.

B. Inspect the entity's reports of prenumbered shipping documents that have not been recorded in the sales journal. Choice "b" is correct. Examination of reports of shipments not recorded in the sales journal is an appropriate test of controls to determine whether all sales have been recorded. Choice "a" is incorrect. Verification that extensions and footings on sales invoices and statements have been recomputed by client personnel ensures that independent checks are being performed, but does not address whether all sales transactions have been recorded. Choice "c" is incorrect. Comparison of invoiced prices with the client's authorized price list ensures that the prices charged are authorized, but does not address whether all sales transactions have been recorded. Choice "d" is incorrect. Inquiring about credit policies is an appropriate audit procedure to verify authorization and valuation of sales transactions, not completeness.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.