CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 151:

Which of the following factors is inherent in a firm's operations if it utilizes only equity financing?

A. Financial risk.

B. Business risk.

C. Interest rate risk.

D. Marginal risk. -

Question 152:

Which of the following is not true about accounting estimates?

A. Accounting estimates measure the effects of past transactions or events that cannot be determined in a timely cost-effective manner.

B. Accounting estimates measure the effects of the present status of an asset or liability.

C. An accounting estimate is an approximation of an account pending the outcome of a future event.

D. An accounting estimate is an approximation of past events that can be determined on a timely cost- effective basis. -

Question 153:

In 1992, hail damaged several of ABC Co.'s vans. Hailstorms had frequently inflicted similar damage to ABC's vans. Over the years, ABC had saved money by not buying hail insurance and either paying for repairs, or selling damaged vans and then replacing them. In 1992, the damaged vans were sold for less than their carrying amount. How should the hail damage cost be reported in ABC's 1992 financial statements?

A. The actual 1992 hail damage loss as an extraordinary loss, net of income taxes.

B. The actual 1992 hail damage loss in continuing operations, with no separate disclosure.

C. The expected average hail damage loss in continuing operations, with no separate disclosure.

D. The expected average hail damage loss in continuing operations, with separate disclosure. -

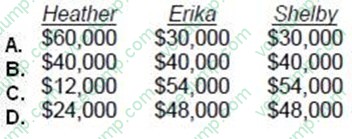

Question 154:

Heather, Erika, and Shelby are members in ABC LLC. Heather works 40 hours per week and Erika and Shelby work 20 hours per week. Heather contributed $30,000 to the LLC and Erika and Shelby contributed $60,000 each. Erika and Shelby have each originated 45% of the LLC's business and Heather has originated the other 10%. Absent an agreement to the contrary, how will the LLC's $120,000 profits be divided among the members?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 155:

Conner purchased 300 shares of Zinco stock for $30,000 in 1980. On May 23, 1994, Conner sold all the stock to his daughter Alice for $20,000, its then fair market value. Conner realized no other gain or loss during 1994. On July 26, 1994,

Alice sold the 300 shares of Zinco for $25,000.

What was Alice's recognized gain or loss on her sale?

A. $0

B. $5,000 long-term gain.

C. $5,000 short-term loss.

D. $5,000 long-term loss. -

Question 156:

Which of the following best describes the responsibility of the auditor to report significant deficiencies and material weaknesses in an attest engagement to examine the effectiveness of a nonissuer's internal control?

A. The auditor must communicate both significant deficiencies and material weaknesses.

B. The auditor must communicate material weaknesses, but need not disclose significant deficiencies.

C. The auditor must communicate significant deficiencies, but need not separately identify material weaknesses.

D. Neither significant deficiencies nor material weaknesses are required to be communicated. -

Question 157:

While auditing the financial statements of a nonissuer, a CPA was requested to change the engagement to a review in accordance with Statements on Standards for Accounting and Review Services (SSARS) because of a scope limitation. If the CPA believes the client's request is reasonable, the CPA's review report should:

A. Refer to the scope limitation that caused the change. II. Describe the auditing procedures that have already been applied.

B. I only.

C. II only.

D. Both I and II.

E. Neither I nor II. -

Question 158:

On December 31, 1989, a building owned by ABC Corp. was totally destroyed by fire. The building had fire insurance coverage up to $500,000. Other pertinent information as of December 31, 1989 follows:

During January 1990, before the 1989 financial statements were issued, ABC received insurance proceeds of $500,000. On what amount should ABC base the determination of its loss on involuntary conversion?

A. $520,000

B. $530,000

C. $550,000

D. $560,000 -

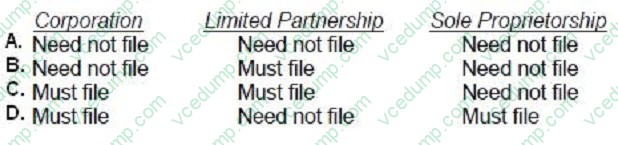

Question 159:

Formation of which of the following types of business does not require the filing of documents with the state?

A. Option A

B. Option B

C. Option C

D. Option D -

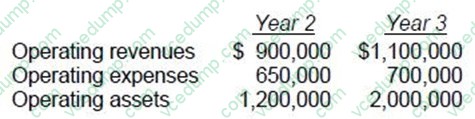

Question 160:

ABC, Inc. made some changes in operations and provided the following information:

What percentage represents the return on investment for year 3?

A. 28.57%

B. 25%

C. 20.31%

D. 20%

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.