AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 161:

Unless otherwise provided in a general partnership agreement, which of the following statements is correct when a partner dies?

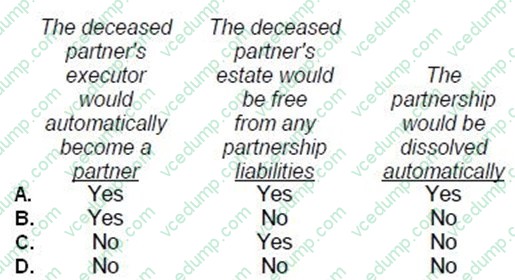

A. Option A B. Option B C. Option C D. Option D

D. Option D Choice "d" is correct. "No - No - No." Upon the death of a general partner: Rule: A partner's death is an event of dissociation. Where a partner dissociates, the partner's right to participate in the management ceases; the partner's executor does not take the partner's place. Rule: The partner's estate remains liable for the partner's obligations to the partnership and has a right to the deceased partner's share of distributions. Rule: Under the Revised Uniform Partnership Act, a partnership does not automatically dissolve on the death of a partner; rather it will dissolve only if 90 days pass and the remaining partners do not wish to continue the partnership. Choices "a", "b", and "c" are incorrect, per the above rules.

Question 162:

The optimal capitalization for an organization usually can be determined by the:

A. Maximum degree of financial leverage (DFL). B. Maximum degree of total leverage (DTL). C. Lowest total weighted-average cost of capital (WACC). D. Intersection of the marginal cost of capital and the marginal efficiency of investment.

C. Lowest total weighted-average cost of capital (WACC). Choice "c" is correct. The optimal capitalization for an organization usually can be determined by the lowest total weighted-average cost of capital (WACC). Capitalization at WACC serves to maximize shareholder's equity. Choice "a" is incorrect. The degree of financial leverage relates to the risk assumed by a firm using fixed debt service costs to finance operations not comprehensively to capital structure. Choice "b" is incorrect. The degree of total leverage relates the risk assumed by a firm using a combination of both debt services costs to finance operations and fixed costs to operate the business, not comprehensively to capital structure. Choice "d" is incorrect. The intersection of the marginal cost of capital and the marginal efficiency of investment does not indicate optimal capitalization.

Question 163:

According to the FASB conceptual framework, which of the following is an essential characteristic of an asset?

A. The claims to an asset's benefits are legally enforceable. B. An asset is tangible. C. An asset is obtained at a cost. D. An asset provides future benefits.

D. An asset provides future benefits. Explanation Explanation/Reference:Choice "d" is correct. An asset provides future benefits. Rule: According to the FASB conceptual framework, assets are probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events.

Question 164:

In an attest engagement, use of the accountant's report should be restricted to specified parties in all of the following situations, except:

A. When the criteria used to evaluate the subject matter are appropriate for only a limited number of parties. B. When reporting on an assertion about the subject matter instead of reporting directly on the subject matter. C. When reporting directly on the subject matter and a written assertion has not been provided. D. When reporting on an agreed-upon procedures engagement.

B. When reporting on an assertion about the subject matter instead of reporting directly on the subject matter. Choice "b" is correct. There is no requirement that the accountant's report be restricted to specified parties when reporting on an assertion about the subject matter instead of reporting directly on the subject matter. Choice "a" is incorrect, since use of the accountant's report should be restricted to specified parties when the criteria used to evaluate the subject matter are appropriate for only a limited number of parties. Choice "c" is incorrect, since use of the accountant's report should be restricted to specified parties when reporting directly on the subject matter and a written assertion has not been provided. Choice "d" is incorrect, since use of the accountant's report should be restricted to specified parties when reporting on an agreed-upon procedures engagement.

Question 165:

In performing an audit in accordance with Generally Accepted Government Auditing Standards (the "Yellow Book"), the auditor:

A. Accepts less responsibility in conducting fieldwork than is accepted in a GAAS audit, since the specific requirements of the Generally Accepted Government Auditing Standards reduce required professional judgment. B. Accepts shared responsibility with Federal Inspectors General, who are equally responsible for compliance evaluation, control, and reporting. C. Accepts greater reporting responsibilities than accepted under a GAAS audit, since the auditor must report on compliance with laws, rules, and regulations, violations of which may affect financial statement amounts, and on the organization's internal control over financial reporting. D. Accepts equal reporting responsibilities with that accepted under GAAS audits, since compliance evaluation and reporting have implied financial statement implications and require expanded treatment as a material contingency.

C. Accepts greater reporting responsibilities than accepted under a GAAS audit, since the auditor must report on compliance with laws, rules, and regulations, violations of which may affect financial statement amounts, and on the organization's internal control over financial reporting. Choice "c" is correct. An auditor's reporting requirements under Generally Accepted Government Auditing Standards (GAGAS or the Yellow Book) are expanded to include reports on the audited entity's compliance with laws, rules, and regulations that have a material impact on the financial statements and on internal controls over financial reporting. Rule: Reporting responsibilities under GAGAS are expanded to include: 1. Reports on compliance with laws, rules, and regulations, violations of which may affect financial statement amounts, and 2. Reports on internal control over financial reporting. Choice "a" is incorrect. Specific reporting requirements and other expanded audit standards associated with Yellow Book audits do not reduce professional judgment. Choice "b" is incorrect. Federal Inspectors General do not split their responsibilities with independent public accountants performing Yellow Book Audits. Choice "d" is incorrect. Although Yellow Book requirements represent logical extensions of generally accepted auditing standards, the specific responsibilities undertaken in an audit that requires application of the Yellow Book would not surface as a result of an audit under generally accepted auditing standards.

Question 166:

Under the Revised Model Business Corporation Act, a merger of two public corporations usually requires all of the following, except:

A. A formal plan of merger. B. An affirmative vote by the holders of a majority of each corporation's voting shares. C. Receipt of voting stock by all stockholders of the original corporations. D. Approval by the board of directors of each corporation.

C. Receipt of voting stock by all stockholders of the original corporations. Choice "c" is correct. A merger can be effected by giving some parties cash or property; not everyone need receive voting shares. Choice "a" is incorrect. The merger must be pursuant to a formal plan. Choice "b" is incorrect. The majority of each corporation generally must approve a merger. Choice "d" is incorrect. A plan of merger must be approved by the boards of the merging corporations.

Question 167:

In the pharmaceutical industry where a diabetic must have insulin no matter what the cost and where there is no substitute, the diabetic's demand curve is best described as:

A. Perfectly elastic. B. Perfectly inelastic. C. Elastic. D. Indifferent.

B. Perfectly inelastic. Choice "b" is correct. When a good is demanded, no matter what the price, demand is described as perfectly inelastic. The demand "curve" is a vertical line at the quantity demanded with price making no difference. Choices "a" and "c" are incorrect. There is no such thing as perfect elasticity. However, the more elastic demand is, the greater the change in quantity demanded for price changes. Choice "d" is incorrect. Diabetics are indifferent to changes in the price of insulin, and to economists, this is perfectly inelastic demand.

Question 168:

Which of the following best describes an auditor's responsibility with respect to communicating internal control deficiencies of issuers?

A. The auditor is required to communicate all deficiencies in internal control to management, deficiencies that constitute a significant deficiency to the audit committee, and deficiencies that constitute a material weakness to the full board of directors. B. The auditor is required to communicate all deficiencies in internal control to management, and deficiencies that constitute a significant deficiency or a material weakness to management and the audit committee. C. The auditor is not required to communicate control deficiencies to management or the audit committee unless they constitute a significant deficiency or a material weakness. D. The auditor is not required to communicate control deficiencies or significant deficiencies to management or the audit committee, but must communicate material weaknesses to both management and the audit committee.

B. The auditor is required to communicate all deficiencies in internal control to management, and deficiencies that constitute a significant deficiency or a material weakness to management and the audit committee. Choice "b" is correct. The auditor is required to communicate all deficiencies in internal control to management, and deficiencies that constitute a significant deficiency or a material weakness to management and the audit committee. Choice "a" is incorrect. There is no requirement that material weaknesses be communicated to the full board of directors. Choice "c" is incorrect. The auditor is required to communicate all deficiencies in internal control to management. Choice "d" is incorrect. The auditor is also required to communicate significant deficiencies to management and the audit committee.

Question 169:

Pell, CPA, decides to serve as principal auditor in the audit of the financial statements of ABC, Inc. Smith, CPA, audits one of ABC's subsidiaries. In which situation(s) should Pell make reference to Smith's audit?

A. Pell reviews Smith's audit documentation and assumes responsibility for Smith's work, but expresses a qualified opinion on ABC's financial statements. II. Pell is unable to review Smith's audit documentation; however, Pell's inquiries indicate that Smith has an excellent reputation for professional competence and integrity. B. I only C. II only D. Both I and II E. Neither I nor II

B. I only Choice "b" is correct. II only. If Pell is unable to review Smith's audit documentation, but inquiries indicate that Smith has an excellent reputation for professional competence and integrity, Pell should divide responsibility by making reference to Smith's audit. Choices "a", "c", and "d" are incorrect. Since the principal auditor in situation I reviews Smith's audit documentation and assumes responsibility for Smith's work, no mention of Smith should be made.

Question 170:

According to the FASB conceptual framework, the usefulness of providing information in financial statements is subject to the constraint of:

A. Consistency. B. Cost-benefit. C. Reliability. D. Representational faithfulness.

B. Cost-benefit. Choice "b" is correct. The pervasive constraint on providing information in financial statements is that the cost should be outweighed by the benefit to be derived from providing the information. SFAC 1 para. 23, SFAC 2 para. 133. Choice "a" is incorrect. Consistency is an underlying concept for financial statements (and a secondary quality of accounting information), but it is not a constraint on providing information. SFAC 2 para. 120. Choice "c" is incorrect. Reliability is a primary quality of accounting information and an underlying concept for financial statements, but it is not a constraint on providing information. SFAC 2 para. 58. Choice "d" is incorrect. Representational faithfulness is an underlying concept for financial statements (as an element of reliability), but it is not a constraint on providing information.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.