CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Jul 26, 2026

AICPA CPA-TEST Online Questions & Answers

-

Question 171:

ABC Corp. wants to acquire the entire business of XYZ Corp. Which of the following methods of business combination will best satisfy ABC's objectives without requiring the approval of the shareholders of either corporation?

A. A merger of XYZ into ABC, whereby XYZ shareholders receive cash or ABC shares.

B. A sale of all the assets of XYZ, outside the regular course of business, to ABC, for cash.

C. An acquisition of all the shares of XYZ through a compulsory share exchange for ABC shares.

D. A cash tender offer, whereby ABC acquires at least 90% of XYZ's shares, followed by a short-form merger of XYZ into ABC. -

Question 172:

The understanding with a client of an auditor's contractual obligation ordinarily is set forth in the:

A. Management letter.

B. Scope paragraph of the auditor's report.

C. Engagement letter.

D. Introductory paragraph of the auditor's report. -

Question 173:

Which of the following items does not pertain to the control environment?

A. Management's philosophy and operating style.

B. Participation of those charged with governance.

C. The accounting records.

D. Personnel policies and practices. -

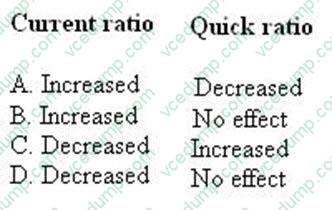

Question 174:

At December 30, 20X3, ABC Co. had cash of $200,000, a current ratio of 1.5:1 and a quick ratio of .5:1. On December 31, 20X3, all cash was used to reduce accounts payable. How did these cash payments affect the ratios?

A. Option A

B. Option B

C. Option C

D. Option D -

Question 175:

Which of the following is not a type of major strategic framework that has proven useful for value chain analysis?

A. Core competencies analysis.

B. Customer preference analysis.

C. Industry structure analysis.

D. Segmentation analysis. -

Question 176:

An auditor may achieve audit objectives related to particular assertions by:

A. Performing analytical procedures.

B. Adhering to a system of quality control.

C. Preparing audit documentation.

D. Increasing the level of detection risk. -

Question 177:

Patents are granted in order to encourage firms to invest in the research and development of new products. Patents are an example of:

A. Market concentration.

B. Entry barriers.

C. Exclusionary practices.

D. Collusion. -

Question 178:

Which of the following statements describes the same characteristic for both an S corporation and a C corporation?

A. Both corporations can have more than 100 shareholders.

B. Both corporations have the disadvantage of double taxation.

C. Shareholders can contribute property into a corporation without being taxed.

D. Shareholders can be either citizens of the United States or foreign countries. -

Question 179:

In 1992, Anchor, Chain, and Hook created ABC Associates, a general partnership. The partners orally agreed that they would work full time for the partnership and would distribute profits based on their capital contributions. Anchor contributed $5,000; Chain $10,000; and Hook $15,000. For the year ended December 31, 1993, ABC Associates had profits of $60,000 that were distributed to the partners. During 1994, ABC Associates was operating at a loss. In September 1994, the partnership dissolved. In October 1994, Hook contracted in writing with XYZ Co. to purchase a car for the partnership. Hook had previously purchased cars from XYZ Co. for use by ABC Associates partners. ABC Associates did not honor the contract with XYZ Co. and XYZ Co. sued the partnership and the individual partners.

A. The ABC Associates oral partnership agreement was valid.

B. The ABC Associates oral partnership agreement was invalid because the partnership lasted for more than one year. -

Question 180:

ABC Corp. is incorporated in State A. Under the Revised Model Business Corporation Act, which of the following activities engaged in by ABC requires that ABC obtain a certificate of authority to do business in State B?

A. Maintaining bank accounts in State B.

B. Collecting corporate debts in State B.

C. Hiring employees who are residents of state B.

D. Maintaining an office in State B to conduct intrastate business.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.