AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1041:

Eugene Entrepreneur developed his waste collections and disposal business from one truck 20 years ago to a fleet of 2,000 trucks serving an entire region today. Gene is looking to retire and knows that he cannot find a suitable buyer for the entire business. Gene has developed a series of short range plans with his senior management group that include generous bonuses, funded in part by deferred repair and maintenance expenses and prior earnings, sales of business segments where possible or transfers of assets to the counties and municipalities that had engaged the waste collection and disposal service. Gene has frozen all new capital investment. The mission that Eugene Entrepreneur has mapped out for his company can best be described as:

A. Build. B. Hold. C. Harvest. D. Sunset.

C. Harvest. Choice "c" is correct. Eugene Entrepreneur has mapped out a harvest mission for his company. As Gene retires and pulls assets and value from the company, he is clearly taking a short-term view toward reaping immediate benefit. Choice "a" is incorrect. A "build" mission anticipates that the business is positioned to expand markets or market share and is characterized by a long-term view that promotes investment. Choice "b" is incorrect. A "hold" mission contemplates that the business is trying to hold on to current market share and is characterized by appropriate investment and competitive positioning. Choice "d" is incorrect. The term "sunset" mission is a distracter.

Question 1042:

Corbin Inc. can issue three-month commercial paper with a face value of $1,000,000 for $980,000. Transaction costs would be $1,200. The effective annualized percentage cost of the financing, based on a 360-day year, would be:

A. 2.16% B. 8.48% C. 8.65% D. 8.00%

C. 8.65% Choice "c" is correct. The cost to issue the commercial paper is the $20,000 original issue discount ($1 million - $980,000), plus transaction costs of $1,200 for a total of $21,200. Therefore, it costs $21,200 to borrow $980,000 for 3 months. The 3-month interest cost is 2.16% ($21,200 / $980,000). The annual interest cost is 8.65%. Choices "a", "b", and "d" are incorrect, per the above calculation.

Question 1043:

When the overall price level is rising, nominal interest rates tend to be:

A. Unaffected by changes in the price level. B. Falling. C. Rising. D. None of the above.

C. Rising. Choice "c" is correct. The relationship between nominal interest rates and inflation can be seen by rearranging the equation for real interest rates as follows: Nominal Interest Rate = Real Interest Rate + Inflation Thus, if real interest rates do not change, a 1% increase in the inflation rate will lead to a 1% increase in nominal interest rates.

Question 1044:

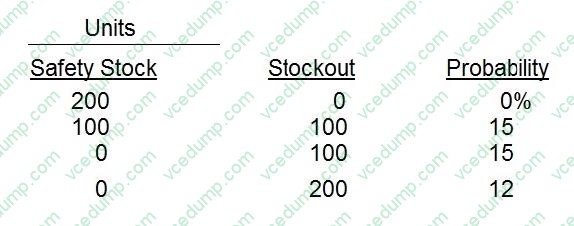

ABC Inc. operates a chain of hardware stores across New England. The controller wants to determine the optimum safety stock levels for an air purifier unit. The inventory manager has compiled the following data.

?The annual carrying cost of inventory approximates 20 percent of the investment in inventory.

?The inventory investment per unit averages $50.

?The stockout cost is estimated to be $5 per unit.

?The company orders inventory on the average of ten times per year.

?The probabilities of a stockout per order cycle with varying levels of safety stock are as follows.

The total cost of safety stock on an annual basis with a safety stock level of 100 units is:

A. $1,750 B. $1,950 C. $2,000 D. $650

A. $1,750 Explanation Explanation/Reference:Choice "a" is correct. $1,750 total annual cost of safety stock of 100 units. Choices "b", "c", and "d" are incorrect, per the above calculation.

Question 1045:

In evaluating the adequacy of the allowance for doubtful accounts, an auditor most likely reviews the entity's aging of receivables to support management's financial statement assertion of:

A. Existence. B. Valuation and allocation. C. Completeness. D. Rights and obligations.

B. Valuation and allocation. Choice "b" is correct. In evaluating the adequacy of the allowance for doubtful accounts, an auditor most likely reviews the entity's aging of receivables to support the assertion of valuation and allocation (i.e., to determine whether the allowance for doubtful accounts properly adjusts the receivables balance to net realizable value). Choice "a" is incorrect. Evaluating the adequacy of the allowance for doubtful accounts does not pertain to existence. To support the assertion of existence, an auditor would most likely confirm accounts receivable. Choice "c" is incorrect. An auditor would trace from shipping records to the sales journal and the accounts receivable ledger to determine if all shipments were properly recorded as sales (completeness assertion). Choice "d" is incorrect. The assertion of rights and obligations relating to accounts receivable would be supported by examining appropriate supporting documentation, not by evaluating the allowance for doubtful accounts.

Question 1046:

Which of the following professional services would be considered an attest engagement?

A. A management consulting engagement to provide EDP advice to a client. B. An engagement to report on management's discussion and analysis (MDandA). C. An income tax engagement to prepare federal and state tax returns. D. The compilation of financial statements from a client's accounting records.

B. An engagement to report on management's discussion and analysis (MDandA). Choice "b" is correct. An engagement to report on management's discussion and analysis (MDandA) would be considered an attest engagement, because the accountant is issuing an examination, review, or agreed-upon procedures report on another party's assertion. Choice "a" is incorrect. A management consulting engagement to provide EDP advice to a client is not considered to be an attest engagement, because the accountant is not issuing an examination, review, or agreed-upon procedures report on another party's assertion. Choice "c" is incorrect. An income tax engagement to prepare federal and state tax returns is not considered to be an attest engagement. Choice "d" is incorrect. The compilation of financial statements from a client's accounting records (a compilation engagement) is not considered to be an attest engagement. (Note that although a compilation of prospective financial statements is covered under Statements on Standards for Attestation Engagements, the question does not indicate that prospective financial statements are involved).

Question 1047:

Which of the following statements is a basic element of the auditor's standard report?

A. The disclosures provide reasonable assurance that the financial statements are free of material misstatement. B. The auditor evaluated the overall internal control. C. An audit includes assessing significant estimates made by management. D. The financial statements are consistent with those of the prior period.

C. An audit includes assessing significant estimates made by management. Choice "c" is correct. The auditor's standard audit report includes a statement that "An audit includes assessing...significant estimates made by management..." Choice "a" is incorrect. The standard audit report does not state that disclosures provide reasonable assurance that the financial statements are free of material misstatement. The correct statement is: "...standards require that we plan and perform the audit to obtain reasonable assurance that the financial statements are free of material misstatement." Choice "b" is incorrect. The standard audit report does not state that the auditor evaluated the overall internal control. The correct statement is "An audit includes...evaluating the overall financial statement presentation." Internal control is not mentioned in the standard audit report. Choice "d" is incorrect. The standard audit report does not state "The financial statements are consistent with those of the prior period." According to the second standard of reporting, consistency is implicitly reported. Only if there is an inconsistency is an explicit statement included.

Question 1048:

Which of the following statements is correct regarding a review engagement of a nonissuer's financial statements performed in accordance with the Statements on Standards for Accounting and Review Services (SSARS)?

A. An accountant must establish an understanding with the client in an engagement letter. B. An accountant must obtain an understanding of the client's internal control when performing a review. C. A review provides an accountant with a basis for expressing limited assurance on the financial statements. D. A review report contains an accountant's opinion of the financial statements taken as a whole.

C. A review provides an accountant with a basis for expressing limited assurance on the financial statements. Choice "c" is correct. A review report is issued when inquiry and analytical procedures provide a reasonable basis for the expression of limited assurance on the financial statements. Choice "a" is incorrect. While the accountant is required to establish an understanding with the client, preferably in writing, an engagement letter is not required. Choice "b" is incorrect. When performing a review under SSARS, the accountant is not required to obtain an understanding of the client's internal control. Choice "d" is incorrect. A review results in the expression of limited assurance that no material modifications are necessary for the financial statements to be in conformity with generally accepted accounting principles. The limited nature of the work performed during a review does not provide sufficient evidence for an opinion on the financial statements taken as a whole.

Question 1049:

During 1993 Kay received interest income as follows:

On U.S. Treasury certificates $4,000 On refund of 1991 federal income tax 500

The total amount of interest subject to tax in Kay's 1993 tax return is:

A. $4,500 B. $4,000 C. $500 D. $0

A. $4,500 Choice "a" is correct. Interest income from U.S. obligations is generally taxable. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed. Choice "b" is incorrect. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed. Choice "c" is incorrect. Interest income from U.S. obligations is generally taxable. Choice "d" is incorrect. Interest income from U.S. obligations is generally taxable. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed.

Question 1050:

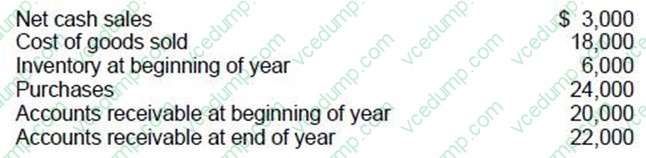

Selected data pertaining to ABC Co. for the calendar year 20X4 is as follows:

What was the inventory turnover for 20X4?

A. 1.2 times. B. 1.5 times. C. 2.0 times. D. 3.0 times.

C. 2.0 times. Choice "c" is correct. Inventory turnover equals cost of goods sold divided by average inventory. Beginning inventory ($6,000) plus purchases ($24,000) less ending inventory equals cost of goods sold ($18,000). Thus, ending inventory equals $12,000 and inventory turnover = $18,000 / [($6,000 + $12,000)/2] = 2.0. Choice "a" is incorrect. Inventory turnover equals cost of goods sold divided by average inventory. Choice "b" is incorrect. Cost of goods sold should be divided by average inventory, not by ending inventory. Choice "d" is incorrect. Cost of goods sold should be divided by average inventory, not by beginning inventory.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.