AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1061:

Tracing copies of computer-prepared sales invoices to copies of the corresponding computer-prepared shipping documents provides evidence that:

A. Shipments to customers were properly billed. B. Entries in the accounts receivable subsidiary ledger were for sales actually shipped. C. Sales billed to customers were actually shipped. D. No duplicate shipments to customers were made.

C. Sales billed to customers were actually shipped. Choice "c" is correct. Tracing from invoices to shipping documents would provide evidence that sales billed to customers were actually shipped. An invoice for which the corresponding shipping documents could not be located might be indicative of fictitious sales (i.e., sales that were recorded but never actually shipped). Choice "a" is incorrect. The auditor would need to start with shipping documents and trace to invoices to ensure that shipments were properly billed. Choice "b" is incorrect. An invoice may exist for which no entry was made in the accounts receivable subsidiary ledger. Therefore, the auditor would need to trace from entries in the accounts receivable subsidiary ledger (and not from invoices) to shipping documents, to obtain evidence that recorded receivables were for sales actually shipped. Choice "d" is incorrect. Tracing from invoices to shipping documents would not necessarily indicate when a duplicate shipment was made, as the auditor would not necessarily realize that two sets of shipping documents related to the same invoice.

Question 1062:

ABC Co. is determining how to finance some long-term projects. ABC has decided it prefers the benefits of no fixed charges, no fixed maturity date and an increase in the credit-worthiness of the company. Which of the following would best meet ABC's financing requirements?

A. Bonds. B. Common stock. C. Long-term debt. D. Short-term debt.

B. Common stock. Choice "b" is correct. Common stock is an equity security that conveys ownership. Common stock does not require any payment, it does not mature and, because it increases equity while having no effect on debt, it decreases the debt equity ratio and increases the credit-worthiness of the firm. Choice "a" is incorrect. Bonds are debt instruments that require specific fixed payments, mature at a specific time and increase debt. Immediately after issue, increases in debt increase the debt equity ratio and decrease credit worthiness. Choice "c" is incorrect. Long-term debt requires specific fixed payments, includes maturity at a specific time and (by definition), increases debt. Immediately after issue, increases in debt increase the debt equity ratio and decrease credit worthiness. Choice "d" is incorrect. Short-term debt requires specific fixed payments, includes maturity at a specific time and, by definition, increase debt. Immediately after issue, increases in debt increase the debt equity ratio and decrease credit worthiness.

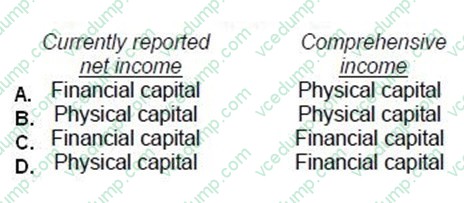

Question 1063:

FASB's conceptual framework explains both financial and physical capital maintenance concepts. Which capital maintenance concept is applied to currently reported net income, and which is applied to comprehensive income?

A. Option A B. Option B C. Option C D. Option D

C. Option C Explanation Explanation/Reference:Choice "c" is correct. Financial capital - Financial capital. Financial capital maintenance is considered to be an element of both "currently reported net income" and "comprehensive income."

Question 1064:

A limited liability company taxed under subchapter K of the Internal Revenue Code (the partnership subchapter):

A. Must pay federal income tax. B. Is generally not considered a legal entity separate and apart from its owners. C. Must have written articles of organization. D. Must provide for apportionment of liability for the company's debts.

C. Must have written articles of organization. Choice "c" is correct. A limited liability company must have written articles of organization, which must be filed with the state. Choice "a" is incorrect. An LLC taxed under subchapter K of the Internal Revenue Code (the partnership subchapter) does not pay federal income tax; the members are taxed on their share of the LLC's income. Choice "b" is incorrect. Unlike a general partnership, but like a corporation and a limited partnership, an LLC is considered a legal entity separate and apart from its owners. Choice "d" is incorrect. An LLC does not have to provide for apportionment of liability for LLC debts; the members of an LLC have limited liability.

Question 1065:

Which of the following statements describes an auditor's obligation to identify deficiencies in the design or operation of internal control?

A. The auditor should design and apply tests of controls to discover significant deficiencies in internal control that could result in material misstatements. B. The auditor need not search for significant deficiencies in internal control unless management requests an attestation that "no significant deficiencies in internal control were noted in the audit." C. The auditor should search for significant deficiencies in internal control if the auditor expects that controls are operating effectively (i.e., if the auditor plans to rely on controls). D. The auditor need not search for significant deficiencies in internal control but should document and communicate any such deficiencies that are discovered.

D. The auditor need not search for significant deficiencies in internal control but should document and communicate any such deficiencies that are discovered. Choice "d" is correct. The auditor need not search for significant deficiencies in internal control, but should document and communicate any such deficiencies that are discovered. Choice "a" is incorrect. Tests of controls are designed and applied to evaluate the risk of financial statement misstatement, and to determine the nature, timing, and extent of substantive tests to be performed. They are not designed to discover significant deficiencies in internal control. Choice "b" is incorrect. Searching for significant deficiencies in internal control is not part of an audit, and it would be inappropriate for the auditor to state that no significant deficiencies in internal control were noted (even if management requested such a statement). Choice "c" is incorrect. Searching for significant deficiencies in internal control is not part of an audit even if the auditor expects that controls are operating effectively (i.e., expects to rely on controls).

Question 1066:

In which of the following circumstances would the use of the negative form of accounts receivable confirmation most likely be justified?

A. A substantial number of accounts may be in dispute and the accounts receivable balance arises from sales to a few major customers. B. A substantial number of accounts may be in dispute and the accounts receivable balance arises from sales to many customers with small balances. C. A small number of accounts may be in dispute and the accounts receivable balance arises from sales to a few major customers. D. A small number of accounts may be in dispute and the accounts receivable balance arises from sales to many customers with small balances.

D. A small number of accounts may be in dispute and the accounts receivable balance arises from sales to many customers with small balances. Choice "d" is correct. The use of negative confirmations most likely would be justified when there are a small number of accounts that may be in dispute and the accounts receivable balance arises from sales to many customers with small balances (e.g., utility consumer customers). Choice "a" is incorrect. Positive (not negative) confirmations should be used when a substantial number of accounts are expected to be in dispute, or if the accounts receivable balance is comprised of accounts from a few major customers. Choice "b" is incorrect. Positive (not negative) confirmations should be used when a substantial number of accounts are expected to be in dispute. Choice "c" is incorrect. Positive (not negative) confirmations should be used when the accounts receivable balance is comprised of accounts from a few major customers.

Question 1067:

Which one of the following statements about supply and demand is true?

A. If supply increases and demand remains constant, equilibrium price will rise. B. If demand increases and supply increases, equilibrium quantity will fall. C. If demand increases and supply decreases, equilibrium price will increase. D. If demand increases and supply remains constant, equilibrium price will fall.

C. If demand increases and supply decreases, equilibrium price will increase. Choice "c" is correct. If quantity demanded for a product goes up, this drives price up. Additionally, if supply decreases, this will also drive prices up. Therefore, it is a certainty that price will be driven up, given an increase in demand and a decrease in supply. Choice "a" is incorrect. Increased supply will reduce (not increase) prices, assuming demand remains constant. Choice "b" is incorrect. Increased demand will increase price, and increased supply will reduce price. The net impact on price cannot be determined without more facts. Choice "d" is incorrect. Increased demand will increase (not reduce) price, assuming supply remains constant.

Question 1068:

In 1992, Anchor, Chain, and Hook created ABC Associates, a general partnership. The partners orally agreed that they would work full time for the partnership and would distribute profits based on their capital contributions. Anchor contributed $5,000; Chain $10,000; and Hook $15,000. For the year ended December 31, 1993, ABC Associates had profits of $60,000 that were distributed to the partners. During 1994, ABC Associates was operating at a loss. In September 1994, the partnership dissolved. In October 1994, Hook contracted in writing with XYZ Co. to purchase a car for the partnership. Hook had previously purchased cars from XYZ Co. for use by ABC Associates partners. ABC Associates did not honor the contract with XYZ Co. and XYZ Co. sued the partnership and the individual partners.

A. Anchor's share of ABC Associates' 1993 profits was $20,000. B. Hook's share of ABC Associates' 1993 profits was $30,000.

B. Hook's share of ABC Associates' 1993 profits was $30,000. Choice "b" is correct. Unless otherwise agreed, partners share profits equally. Here, the partners agreed to share profits on the basis of their contributions, which were in a ratio of 1:2:3 respectively for Anchor, Chain, and Hook. Thus, Anchor's share of the 1993 profits was $10,000, Chain's share was $20,000, and Hook's share was $30,000.

Question 1069:

In which case might an auditor of an issuer render a qualified opinion on internal control?

A. When there is a scope limitation. B. When there is a material weakness in internal control. C. Both "a" and "b". D. Neither "a" nor "b".

D. Neither "a" nor "b". Choice "d" is correct. A scope limitation requires the auditor to disclaim an opinion or withdraw from the engagement, and a material weakness in internal control requires the auditor to issue an adverse opinion. Neither situation would result in a qualified opinion. Choice "a" is incorrect. A scope limitation requires the auditor to disclaim an opinion or withdraw from the engagement. Choice "b" is incorrect. A material weakness in internal control requires the auditor to issue an adverse opinion. Choice "c" is incorrect. A scope limitation requires the auditor to disclaim an opinion or withdraw from the engagement, and a material weakness in internal control requires the auditor to issue an adverse opinion. Neither situation would result in a qualified opinion.

Question 1070:

In competitive markets, an increase in an effective minimum wage will:

A. Have a neutral effect on the demand for labor. B. Decrease the supply of labor. C. Decrease unemployment. D. Increase unemployment.

D. Increase unemployment. Choice "d" is correct. When the "minimum" wages are increased, employers may elect to hire fewer employees thereby increasing unemployment. Choice "a" is incorrect. An increase in the minimum wage will have an effect on the demand for labor. Choice "b" is incorrect. The supply of labor will likely go up as the wage being paid increases. Choice "c" is incorrect. As the minimum wage increases, unemployment will increase.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.