CPA-TEST Exam Details

-

Exam Code

:CPA-TEST -

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation -

Certification

:AICPA Certifications -

Vendor

:AICPA -

Total Questions

:1241 Q&As -

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions & Answers

-

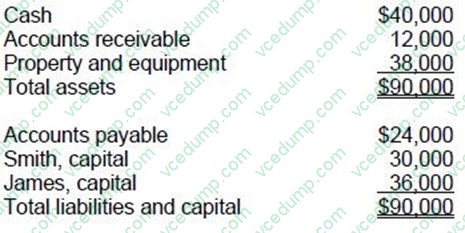

Question 1031:

Smith and James were partners in S and J Partnership. The partnership agreement stated that all profits and losses were allocated 60 percent to Smith and 40 percent to James. The partners decided to terminate and wind up the partnership. The following was the balance sheet for S and J on the day of the windup:

Of the total accounts receivable, $10,000 was collected and the remainder was written off as bad debt. All liabilities of S and J were paid by the partnership. The property and equipment are sold for $32,000. Under the Uniform Partnership Act, what amount of cash was distributed to Smith?

A. $25,200

B. $26,000

C. $30,000

D. $34,800 -

Question 1032:

An inventory loss from a market price decline occurred in the first quarter, and the decline was not expected to reverse during the fiscal year. However, in the third quarter the inventory's market price recovery exceeded the market decline that

occurred in the first quarter. For interim financial reporting, the dollar amount of net inventory should:

A. Decrease in the first quarter by the amount of the market price decline and increase in the third quarter by the amount of the decrease in the first quarter.

B. Decrease in the first quarter by the amount of the market price decline and increase in the third quarter by the amount of the market price recovery.

C. Decrease in the first quarter by the amount of the market price decline and not be affected in the third quarter.

D. Not be affected in either the first quarter or the third quarter. -

Question 1033:

ABC, LP is a limited partnership. Dave is a limited partner. XYZ, Inc. is a creditor of the limited partnership. Upon dissolution of the partnership, the assets of ABC, LP will be distributed to pay:

A. XYZ, Inc., first.

B. Dave first.

C. XYZ, Inc. and Dave.

D. The general partners first. -

Question 1034:

When managing cash and short-term investments, a corporate treasurer is primarily concerned with:

A. Maximizing rate of return.

B. Minimizing taxes.

C. Investing in common stock due to the dividend exclusion for federal income tax purposes.

D. Liquidity and safety. -

Question 1035:

Which of the following procedures would an auditor most likely perform for year-end accounts receivable confirmations when the auditor did not receive replies to second requests?

A. Review the cash receipts journal for the month prior to the year-end.

B. Intensify the study of the internal control structure concerning the revenue cycle.

C. Increase the assessed level of detection risk for the existence assertion.

D. Inspect the shipping records documenting the merchandise sold to the debtors. -

Question 1036:

Management accountants are frequently asked to analyze various decision situations including the following.

A. The cost of a special device that is necessary if a special order is accepted. II. The cost proposed annually for the plant service for the grounds at corporate headquarters. III. Joint production costs incurred, to be considered in a sell-at-split versus a process-further decision. IV. The costs associated with alternative uses of plant space, to be considered in a make/buy decision.

B. The cost of obsolete inventory acquired several years ago, to be considered in a keep-versus disposal decision. The costs described in situations I and IV above are:

C. Prime costs.

D. Sunk costs.

E. Discretionary costs.

F. Relevant costs. -

Question 1037:

ABC Products has received proposals from several banks to establish a lockbox system to speed up receipts. ABC receives an average of 700 checks per day averaging $1,800 each, and its cost of short- term funds is 7 percent per year. Assuming that all proposals will produce equivalent processing results and using a 360-day year, which one of the following proposals is optimal for ABC?

A. A flat fee of $125,000 per year.

B. A fee of 0.03 percent of the amount collected.

C. A compensating balance of $1,750,000.

D. A fee of $0.35 per check plus 0.01 percent of the amount collected. -

Question 1038:

Average daily cash outflows are $3 million for ABC Inc. A new cash management system can add two days to the disbursement schedule. Assuming ABC earns 10 percent on excess funds, how much should the firm be willing to pay per year for this cash management system?

A. $3,000,000

B. $1,500,000

C. $600,000

D. $150,000 -

Question 1039:

During the first quarter of 1993, ABC Co. had income before taxes of $200,000, and its effective income tax rate was 15%. ABC's 1992 effective annual income tax rate was 30%, but ABC expects its 1993 effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of income tax expense should ABC report?

A. $0

B. $30,000

C. $50,000

D. $60,000 -

Question 1040:

In using the work of a specialist, an auditor referred to the specialist's findings in the auditor's report. This would be an appropriate reporting practice if the:

A. Client is not familiar with the professional certification, personal reputation, or particular competence of the specialist.

B. Auditor, as a result of the specialist's findings, adds an explanatory paragraph emphasizing a matter regarding the financial statements.

C. Auditor understands the form and content of the specialist's findings in relation to the representations in the financial statements.

D. Auditor, as a result of the specialist's findings, decides to indicate a division of responsibility with the specialist.

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only AICPA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your CPA-TEST exam preparations and AICPA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.