AICPA CPA-TEST Online Practice

Questions and Exam Preparation

CPA-TEST Exam Details

Exam Code

:CPA-TEST

Exam Name

:Certified Public Accountant Test: Auditing and Attestation, Business Environment and Concepts, Financial Accounting and Reporting, Regulation

Certification

:AICPA Certifications

Vendor

:AICPA

Total Questions

:1241 Q&As

Last Updated

:Aug 03, 2026

AICPA CPA-TEST Online Questions &

Answers

Question 1051:

To determine whether accounts payable are complete, an auditor performs a test to verify that all merchandise received is recorded. The population of documents for this test consists of all:

A. Payment vouchers. B. Receiving reports. C. Purchase requisitions. D. Vendor's invoices.

B. Receiving reports. Choice "b" is correct. To determine whether accounts payable are complete, an auditor performs a test to verify that all merchandise received is recorded. This test consists of tracing from receiving reports for inventory received before year-end to the accounts payable trial balance to determine whether the purchase has been properly recorded. Choice "a" is incorrect. In testing for completeness of payables, the auditor tries to determine whether there are payables that have not been recorded. If the auditor selects from payment vouchers, he or she may be unlikely to select an unrecorded payable, since unrecorded payables that have not yet been paid would not have corresponding payment vouchers. Choice "c" is incorrect. Purchase requisitions do not indicate when the inventory was received, and therefore they are not useful for testing the completeness of accounts payable. Choice "d" is incorrect. Vendor's invoices do not generally indicate when the inventory was received, and therefore they are not useful for testing the completeness of accounts payable.

Question 1052:

According to the FASB's conceptual framework, the process of reporting an item in the financial statements of an entity is:

A. Recognition. B. Realization. C. Allocation. D. Matching.

A. Recognition. Choice "a" is correct. Recognition. According to the FASB's conceptual framework, the process of reporting an item in the financial statements of an entity is recognition.

Question 1053:

An auditor most likely would review an entity's periodic accounting for the numerical sequence of shipping documents and invoices to support management's financial statement assertion of:

A. Occurrence. B. Classification. C. Cutoff. D. Completeness.

D. Completeness. Choice "d" is correct. An entity's periodic accounting for the numerical sequence of shipping documents and invoices supports management's financial statement assertion of completeness of sales. A gap in recorded sequence numbers might indicate an unrecorded sale. Choice "a" is incorrect. An auditor would trace from the sales invoices or sales journal (accounting records) to the shipping documents (source document) to support management's assertion of occurrence. Choice "b" is incorrect. An auditor would examine journal entries for a sample of shipping documents to determine whether the client has recorded the sales in the proper accounts. Choice "c" is incorrect. An auditor would review supporting documentation for shipping documents just before and just after year-end to determine whether appropriate cutoff has been achieved.

Question 1054:

ABC, Inc. manufactures and sells television sets. All sales are finalized on credit with terms of 2/10, n/30. Seventy percent of ABC customers take discounts and pay on day 10, while the remaining 30% pay on day 30. What is the average collection period in days?

A. 10 B. 16 C. 24 D. 40

B. 16 Choice "b" is correct. The average collection period represents the weighted average of the periods that accounts receivable are outstanding and is computed as follows: Choice "a" is incorrect, per the above computation. Choice "c" is incorrect. This proposed solution mismatches the percentages and the days and represents the sum of the products of 30 x 70 % and 10 x 30%. Choice "d" is incorrect. This proposed solution is purely the sum of the two customer payment patterns presented, 10 and 30.

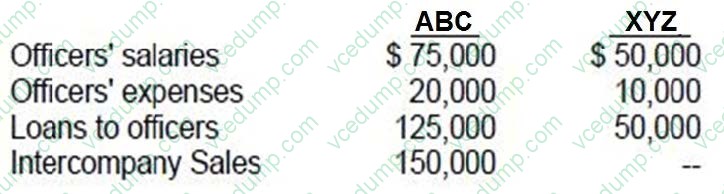

Question 1055:

ABC Co. acquired 100% of XYZ Corp. prior to 1989. During 1989, the individual companies included in their financial statements the following:

What amount should be reported as related party disclosures in the notes to ABC's 1989 consolidated financial statements?

A. $150,000 B. $155,000 C. $175,000 D. $330,000

C. $175,000 Choice "c" is correct. The only related party transaction that would require disclosure (assuming that all amounts are material to the financial statements) would be the loans to officers since they are outside of the ordinary course of business. Choices "a", "b", and "d" are incorrect. Officers' salaries, officers' expenses and intercompany sales (between entities included in a consolidated set of financial statements) are all transactions in the ordinary course of business and generally would not require disclosure.

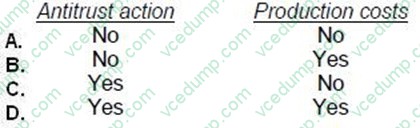

Question 1056:

In 1990, ABC Co. incurred losses arising from its guilty plea in its first antitrust action, and from a substantial increase in production costs caused when a major supplier's workers went on strike. Which of these losses should be reported as an extraordinary item?

A. Option A B. Option B C. Option C D. Option D

C. Option C Choice "c" is correct. Yes - No. Rule: Losses arising from a company's first (and probably "last") "anti-trust" action are unusual and extraordinary and should be reported as an extraordinary item. Losses resulting from additional costs caused by a strike at a major supplier or even at one's own company are not extraordinary and should be disclosed as a separate component of "income from continuing operations."

Question 1057:

The monitoring component of internal control excludes:

A. Assessing information derived from external parties. B. Assessing the quality of internal control performance over time. C. Improving controls that are not operating effectively. D. Eliminating controls that are not operating effectively.

D. Eliminating controls that are not operating effectively. Choice "d" is correct. Monitoring is the process of assessing the quality of internal control performance over time and taking necessary corrective actions. Eliminating a control that is not operating effectively would not be an appropriate corrective action. Choice "a" is incorrect. Information derived from external parties (such as customer complaints and regulator comments) may be useful in identifying problems with the internal control structure. Choices "b" and "c" are incorrect. Assessing the quality of internal control performance over time and improving controls that are not operating effectively are part of the monitoring process.

Question 1058:

The continual process of re-evaluating the strategic plans includes all of the following significant questions a firm should be concerned with, except:

A. Has the firm been able to attain or maintain competitive advantage? B. Is the firm able to be profitable under the current strategy? C. Does the current strategy continue to be aligned with the established goals of the firm? D. Has the firm been able to adapt to the preferences of its employees?

D. Has the firm been able to adapt to the preferences of its employees? Explanation Explanation/Reference:Choice "d" is correct. Although the firm needs to be flexible with respect to changes in many situations and then adapt to them, the ability to adapt to the preferences of its employees is not nearly as significant to the process as the other three choices, which are crucial to the success of the strategic plan. Choices "a", "b", and "c" are incorrect because they are all significant questions a firm should be concerned with when re-evaluating the strategic plan.

Question 1059:

Which of the following conditions is necessary for a practitioner to accept an attest engagement to examine and report on a nonissuer's internal control over financial reporting?

A. The practitioner anticipates relying on the entity's internal control in a financial statement audit. B. Management presents its written assertion about the effectiveness of internal control. C. The practitioner is a continuing auditor who previously has audited the entity's financial statements. D. Management agrees not to present the practitioner's report in a general-use document to stockholders.

B. Management presents its written assertion about the effectiveness of internal control. Choice "b" is correct. In order for a practitioner to examine and report on management's assertion about the effectiveness of an entity's internal control, management must present its written assertion about the effectiveness of internal control. Choice "a" is incorrect. The examination may be made separately from or in conjunction with an audit, and there is no requirement that the practitioner rely on internal control. Choice "c" is incorrect. No requirement for previous engagement experience exists in order to report on a client's internal control. Choice "d" is incorrect. The practitioner's report is considered appropriate for general distribution.

Question 1060:

Which of the following types of entities are required to report on business segments?

A. Nonpublic business enterprises. B. Publicly-traded enterprises. C. Not-for-profit enterprises. D. Joint ventures.

A. Nonpublic business enterprises. Choice "b" is correct. Only publicly-traded enterprises are required to report on business segments. Choices "a", "c", and "d" are incorrect, per theabove.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only AICPA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your CPA-TEST exam preparations

and AICPA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.