8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 271:

Which of the following statements is true?

I - If no loss data is available, good quality scenarios can be used to model operational risk II - Scenario data can be mixed with observed loss data for modeling severity and frequency estimates III - Severity estimates should not be created by fitting models to scenario generated loss data points alone IV - Scenario assessments should only be used as modifiers to ILD or ELD severity models

A. I

B. I and II

C. III and IV

D. All statements are true -

Question 272:

The results of 'desk-level' stress tests cannot be added together to arrive at institution wide estimates because:

A. Desk-level stress tests tend to ignore higher level risks that are relevant to the institution but completely outside the control of the individual desks.

B. Desk-level stress tests focus on desk specific risks that may be minor or irrelevant in the larger scheme at the institution level.

C. Desk-level stress tests tend to focus on extreme movements in risk parameters (such as volatility) without considering economy wide scenarios that may represent more realistic and consistent situations for the institution.

D. All of the above -

Question 273:

In the case of historical volatility weighted VaR, a higher current volatility when compared to historical volatility:

A. will not affect the VaR estimate

B. will increase the confidence interval

C. will decrease the VaR estimate

D. will increase the VaR estimate -

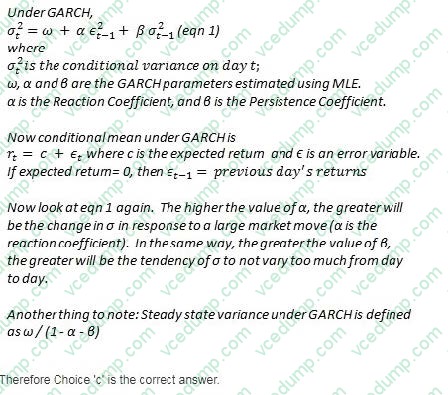

Question 274:

As the persistence parameter under GARCH is lowered, which of the following would be true:

A. The model will give lower weight to recent returns

B. High variance from the recent past will persist for longer

C. The model will react faster to market shocks

D. The model will react slower to market shocks -

Question 275:

If a borrower has a default probability of 12% over one year, what is the probability of default over a month?

A. 12.00%

B. 1.00%

C. 2.00%

D. 1.06% -

Question 276:

As part of designing a reverse stress test, at what point should a bank's business plan be considered unviable (ie the point where it can be considered to have failed)?

A. Where EBITDA for the year is forecast to be negative

B. Where large known losses have been incurred on the bank's positions

C. When the regulatory capital of the bank has been exhausted

D. When the realization of risks leads market participants to lose confidence in the bank as a counterparty or a business worthy of funding -

Question 277:

Which of the following is true in relation to Principal Component Analysis (PCA)?

I - An n x n positive definite square matrix will have n-1 eigenvectors II - The eigenvalues for a correlation matrix can be derived from the corresponding values for the covariance matrix III - Principal components are uncorrelated to each other IV - PCA is useful as it allows 100% of the variation in a complex system to be explained by the first three principal components

A. I and III

B. I, II and IV

C. III and IV

D. III -

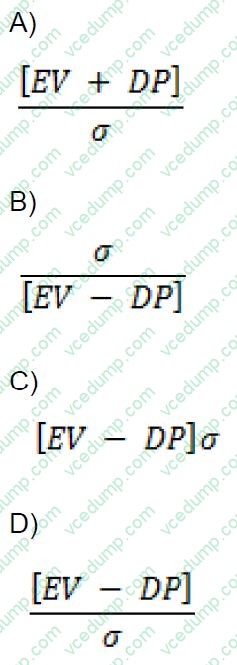

Question 278:

If EV be the expected value of a firm's assets in a year, and DP be the 'default point' per the KMV approach to credit risk, and be the standard deviation of future asset returns, then the distance-to-default is given by:

A. Option A

B. Option B

C. Option C

D. Option D -

Question 279:

If two bonds with identical credit ratings, coupon and maturity but from different issuers trade at different spreads to treasury rates, which of the following is a possible explanation:

I - The bonds differ in liquidity II - Events have happened that have changed investor perceptions but these are not yet reflected in the ratings III - The bonds carry different market risk IV - The bonds differ in their convexity

A. I, II and IV

B. II and IV

C. I and II

D. III and IV -

Question 280:

When estimating the risk of a portfolio of equities using the portfolio's beta, which of the following is NOT true:

A. relies upon the single factor CAPM model

B. use of the beta assumes that the portfolio is diversified enough so that the specific risks of the individual stocks offset each other

C. explicitly considers specific risk inherent in the portfolio for risk calculations

D. using the beta significantly eases the computational burden of calculating risk

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.