Which of the following should be included when calculating the Gross Income indicator used to calculate operational risk capital under the basic indicator and standardized approaches under Basel II?

A. Insurance income B. Operating expenses C. Fees paid to outsourcing service proviers D. Net non-interest income

D. Net non-interest income

Explanation

Gross income is defined by Basel II (see para 650 of the Basel standard) as net interest income plus net non-interest income. It is intended that this measure should: (i) be gross of any provisions (e.g. for unpaid interest); (ii) be gross of operating expenses, including fees paid to outsourcing service providers; (iii) exclude realised profits/losses from the sale of securities in the banking book; and (iv) exclude extraordinary or irregular items as well as income derived from insurance. What this means is that gross income is calculated without deducting any provisions or operating expenses from net interest plus non-interest income; and does not include any realised profits or losses from the sale of securities in the banking book, and also does not include any extraordinary or irregular item or insurance income. Therefore operating expenses are to be not to be deducted for the purposes of calculating gross income, and neither are any provisions. Profits and losses from the sale of banking book securities are not considered part of gross income, and so isn't any income from insurance or extraordinary items. Of the listed choices, only net non-interest income needs to be included for gross income calculations, and the others are to be excluded. Therefore Choice 'd' is the correct answer. Try to remember the components of gross income from the definition above because in the exam the question may be phrased differently.

Question 2:

Which of the following statements are true:

I - Shocks to risk factors should be relative rather than absolute if we wish to avoid a change in the sign of the risk factor.

II - Interest rate shocks are generally modeled as absolute shocks.

III - Shocks to volatility are generally modeled as absolute shocks.

IV - Shocks to market spreads are generally modeled as relative shocks.

A. II and IV B. II only C. I, II and III D. I and II

D. I and II

Explanation

Suppose during a historical event interest rates rose from 2% to 2.25%. This can be understood as a change of either 25 basis points, or a change of 12.5%. When applied to the current portfolio when interest rates are 0.50%, we may model this 'shock' as either a rise to 0.75%, or 0.5625% (ie a rise of 12.5% over existing levels). The former is called an absolute shock, and the latter a relative shock. I is true as relative shocks can never change the sign of a risk factor. Yet interest rate changes are modeled as absolute changes as relative shocks can get artificially amplified or attenuated if the current level of interest rates is too different from those that existed during the crisis being modeled. Therefore II is true. III and IV are false as volatility is modeled as a relative shock and spreads are modeled as absolute shocks.

Question 3:

Which of the following statements is true:

I - Confidence levels for economic capital calculations are driven by desired credit ratings

II - Loss distributions for operational risk are affected more by the severity distribution than the frequency distribution

III - The Advanced Measurement Approach (AMA) referred to in the Basel II standard is a type of a Loss Distribution Approach (LDA)

IV - The loss distribution for operational risk under the LDA (Loss Distribution Approach) is estimated by separately estimating the frequency and severity distributions.

A. I and II B. I, III and IV C. I, II and IV D. III and IV

C. I, II and IV

Explanation

Statement I is correct. Economic capital is the capital available to absorb unexpected losses, and credit ratings are also based upon a certain probability of default. Economic capital is often calculated at a level equal to the confidence required for the desired credit rating. For example, if the probability of default for a AA rating is 0.02%, then economic capital maintained at a 99.98% would allow for such a rating. Economic capital set at a 99.8% level can be thought of as the level of losses that would not be exceeded with a 99.8% probability.

Loss distributions are the product of the severity and frequency distributions, each of which are estimated separately. The total loss distribution is affected far more by the severity distribution than by the frequency distribution, therefore statement II is correct.

The Loss Distribution Approach (LDA) is one of the ways in which the requirements of the AMA can be satisfied, and not the other way round. Therefore statement III is incorrect.

Statement IV is correct as the total loss distribution is estimated using separate estimates of loss frequency and distributions.

Question 4:

Which of the following steps are required for computing the total loss distribution for a bank for operational risk once individual UoM level loss distributions have been computed from the underlhying frequency and severity curves:

I - Simulate number of losses based on the frequency distribution II - Simulate the dollar value of the losses from the severity distribution III - Simulate random number from the copula used to model dependence between the UoMs IV - Compute dependent losses from aggregate distribution curves

A. None of the above B. III and IV C. I and II D. All of the above

C. I and II

Explanation

A recap would be in order here: calculating operational risk capital is a multi-step process. First, we fit curves to estimate the parameters to our chosen distribution types for frequency (eg, Poisson), and severity (eg, lognormal). Note that these curves are fitted at the UoM level - which is the lowest level of granularity at which modeling is carried out. Since there are many UoMs, there are are many frequency and severity distributions. However what we are interested in is the loss distribution for the entire bank from which the 99.9th percentile loss can be calculated. From the multiple frequency and severity distributions we have calculated, this becomes a two step process:

-

Step 1: Calculate the aggregate loss distribution for each UoM. Each loss distribution is based upon and underlying frequency and severity distribution.

-

Step 2: Combine the multiple loss distributions after considering the dependence between the different UoMs. The 'dependence' recognizes that the various UoMs are not completely independent, ie the loss distributions are not additive, and that there is a sort of diversification benefit in the sense that not all types of losses can occur at once and the joint probabilities of the different losses make the sum less than the sum of the parts. Step 1 requires simulating a number, say n, of the number of losses that occur in a given year from a frequency distribution. Then n losses are picked from the severity distribution, and the total loss for the year is a summation of these losses. This becomes one data point. This process of simulating the number of losses and then identifying that number of losses is carried out a large number of times to get the aggregate loss distribution for a UoM. Step 2 requires taking the different loss distributions from Step 1 and combining them considering the dependence between the events. The correlations between the losses are described by a 'copula', and combined together mathematically to get a single loss distribution for the entire bank. This allows the 99.9th percentile loss to be calculated.

Question 5:

If the systematic VaR for an equity portfolio is $100 and the specific VaR is $80, then which of the following is true in relation to the total VaR:

A. Total VaR is greater than $180 B. Total VaR is $20 C. Total VaR is $180 D. Total VaR is less than $180

D. Total VaR is less than $180

Explanation

Choice 'd' is correct because VaR is sub-additive in cases where correlation is less than one.

Specific VaR refers to the risk in the portfolio from security selection, ie the risk from holding the specific equities in the portfolio, while systematic risk refers to the market risk. Definitionally, specific risk and systematic risk are uncorrelated, ie

their correlation is zero. Since their correlation is zero, combining them will produce a VaR number lower than their stand alone aggregate. Total risk includes both specific risk and systematic risk, and can be calculated taking into account the

specific and systematic VaRs and their correlation.

All other answers are therefore incorrect.

Question 6:

If the marginal probabilities of default for a corporate bond for years 1, 2 and 3 are 2%, 3% and 4% respectively, what is the cumulative probability of default at the end of year 3?

A. 8.74% B. 9.58% C. 9.00% D. 91.26%

A. 8.74%

Explanation

Marginal probabilities of default are the probabilities for default for a given period, conditional on survival till the end of the previous period. Cumulative probabilities of default are probabilities of default by a point in time, regardless of when the default occurs. If the marginal probabilities of default for periods 1, 2... n are p1, p2...pn, then cumulative probability of default can be calculated as Cn = 1 - (1 - p1)(1-p2)...(1-pn). For this question, we can calculate the probability of default for year 3 as =1 - (1-2%)*(1-3%)*(1-4%) = 8.74%

Question 7:

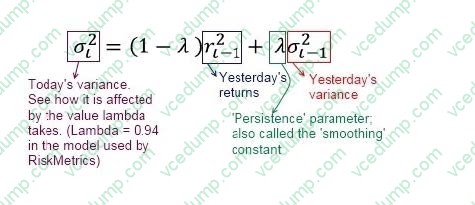

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter = 0.93. A. 0.0421

B. 0.0224

C. 0.0429

D. 0.0018

Correct Answer. A

A

Explanation

The correct answer is choice 'a'

Recall the formula for calculating variance under EWMA. See below. Therefore the correct answer is =SQRT((1 - 0.93)*(LN(11/10))^2 + 0.93*((3.5%^2))) = 4.21%. Other answers are incorrect. Note that continuous returns are to be used, ie ln

(11/10) and not discrete returns (=1/10) - though generally the difference between the two is small over short time periods. (If in the exam the answer doesn't exactly match, try using discrete returns.)

Question 8:

CreditRisk+, the actuarial model for calculating portfolio credit risk, is based upon:

A. the exponential distribution B. the normal distribution C. the Poisson distribution D. the log-normal distribution

C. the Poisson distribution

Explanation

CreditRisk+ treats default as a binary event, ignoring downgrade risk, capital structures of individual firms in the portfolio or the causes of default. It uses a single parameter, or the mean default rate, and derives credit risk based upon the Poisson distribution. Therefore Choice 'c' is the correct answer.

Question 9:

Which of the following is not an approach proposed by the Basel II framework to compute operational risk capital?

A. Basic indicator approach B. Factor based approach C. Standardized approach D. Advanced measurement approach

B. Factor based approach

Explanation

Basel II proposes three approaches to compute operational risk capital - the basic indicator approach (BIA), the standardized approach (SIA) and the advanced measurement approach (AMA). There is no operational risk approach called the factor based approach.

Question 10:

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

A. The risk that mortgage interest rates will rise in the future B. The risk that the homeowners will pay the mortgage off before they are due C. The risk that the homeowners will not be able to pay their mortgage when they are due D. The risk that CDS spreads on the bank's debt will rise making funding more expensive

D. The risk that CDS spreads on the bank's debt will rise making funding more expensive

Explanation

Choice 'd' represents a risk that does not arise from its holdings of mortgages. Therefore Choice 'd' is the correct answer. All the other risks identified are correct - the bank faces interest rate, default and prepayment risks on its mortgages.

Nowadays, the certification exams become more and more important and required by more and more

enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare

for the exam in a short time with less efforts? How to get a ideal result and how to find the

most reliable resources? Here on Vcedump.com, you will find all the answers.

Vcedump.com provide not only PRMIA exam questions,

answers and explanations but also complete assistance on your exam preparation and certification

application. If you are confused on your 8008 exam preparations

and PRMIA certification application, do not hesitate to visit our

Vcedump.com to find your solutions here.