8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 351:

What is the risk horizon period used for credit risk as generally used for economic capital calculations and as required by regulation?

A. 1-day

B. 1 year

C. 10 years

D. 10 days -

Question 352:

Which of the following cannot be used to address the issue of heavy tails when modeling market returns

A. EVT

B. EWMA

C. Normal mixtures

D. Student's t-distribution -

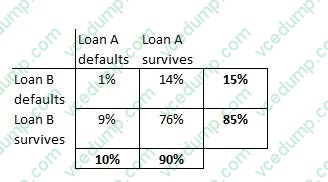

Question 353:

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

A. 500000

B. 250000

C. 1000000

D. 240000 -

Question 354:

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds over a one year horizon are 0.03 and 0.08 respectively. If the default correlation is zero, what is the one year expected loss on this portfolio?

A. $11m

B. $5.26m

C. $5.5m

D. $1.38m -

Question 355:

Which of the following are likely to be useful to a risk manager analyzing liquidity risk for an international bank?

I - Information on liquidity mismatches II - Funding concentration III - Lending concentration IV - A report on illiquid assets

A. I and II

B. III and IV

C. I, II, III and IV

D. I, II and IV -

Question 356:

What is the 1-day VaR at the 99% confidence interval for a cash flow of $10m due in 6 months time? The risk free interest rate is 5% per annum and its annual volatility is 15%. Assume a 250 day year.

A. 5500

B. 1744500

C. 109031

D. 85123 -

Question 357:

An equity manager holds a portfolio valued at $10m which has a beta of 1.1. He believes the market may see a dip in the coming weeks and wishes to eliminate his market exposure temporarily. Market index futures are available and the current futures notional on these is $50,000 per contract. Which of the following represents the best strategy for the manager to hedge his risk according to his views?

A. Sell 200 futures contracts

B. Buy 220 futures contracts

C. Sell 220 futures contracts

D. Liquidate his portfolio as soon as possible -

Question 358:

For a corporate bond, which of the following statements is true:

I - The credit spread is equal to the default rate times the recovery rate II - The spread widens when the ratings of the corporate experience an upgrade III - Both recovery rates and probabilities of default are related to the business cycle and move in opposite directions to each other IV - Corporate bond spreads are affected by both the risk of default and the liquidity of the particular issue

A. I, II and IV

B. III and IV

C. III only

D. IV only -

Question 359:

Credit exposure for derivatives is measured using A. Current replacement value

B. Notional value of the derivative

C. Forward looking exposure profile of the derivative

D. Standard normal distribution

Correct Answer. C -

Question 360:

Which of the formulae below describes incremental VaR where a new position 'm' is added to the portfolio? (where p is the portfolio, and V_i is the value of the i-th asset in the portfolio. All other notation and symbols have their usual meaning.)

A. Option A

B. Option B

C. Option C

D. Option D

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.