8008 Exam Details

-

Exam Code

:8008 -

Exam Name

:PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

Certification

:PRMIA Certifications -

Vendor

:PRMIA -

Total Questions

:362 Q&As -

Last Updated

:Jul 15, 2026

PRMIA 8008 Online Questions & Answers

-

Question 281:

Which of the following are true:

I - The total of the component VaRs for all components of a portfolio equals the portfolio VaR.

II - The total of the incremental VaRs for each position in a portfolio equals the portfolio VaR.

III - Marginal VaR and incremental VaR are identical for a $1 change in the portfolio.

IV - The VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than (or in extreme cases equal to) the sum of the individual VaRs.

V - The component VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than the sum of the individual component VaRs.

A. II and V

B. II and IV

C. I and II

D. I, III and IV -

Question 282:

Loss provisioning is intended to cover:

A. Unexpected losses

B. Losses in excess of unexpected losses

C. Both expected and unexpected losses

D. Expected losses -

Question 283:

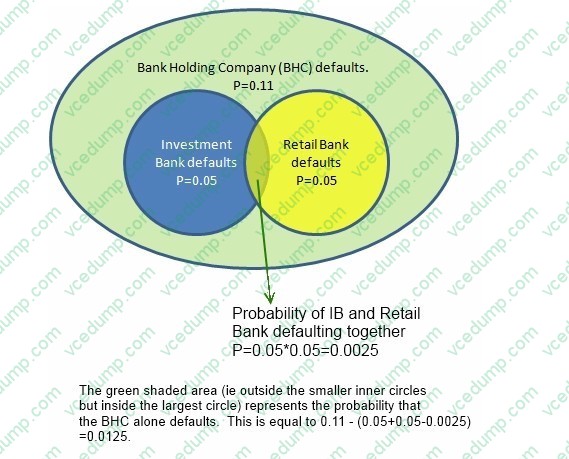

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank's defaults are independent of each other, with a probability of default of 0.05 each. The BHC's probability of default is 0.11. What is the probability of default of both the BHC and the investment bank? What is the probability of the BHC's default provided both the investment bank and the retail bank survive?

A. 0.0475 and 0.10

B. 0.11 and 0

C. 0.08 and 0.0475

D. 0.05 and 0.0125 -

Question 284:

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the probability of the two bonds defaulting simultaneously is 1.4%, what is the default correlation between the two?

A. 0%

B. 100%

C. 40%

D. 25% -

Question 285:

An investor holds a bond portfolio with three bonds with a modified duration of 5, 10 and 12 years respectively. The bonds are currently valued at $100, $120 and $150. If the daily volatility of interest rates is 2%, what is the 1-day VaR of the portfolio at a 95% confidence level?

A. 115.51

B. 163.11

C. 370

D. 165 -

Question 286:

Which of the following statements is correct?

A. Funding liquidity risks present themselves in the form of an adverse market impact on prices from a trade

B. Dynamic simulations of liquidity needs require an assumption of counterparty risk remaining constant

C. Market liquidity risk is idiosyncratic while funding liquidity risk is not

D. Market liquidity risks present themselves in the form of higher bid offer spreads -

Question 287:

Which of the following statements is true in relation to a normal mixture distribution:

I - The mixture will always have a kurtosis greater than a normal distribution with the same mean and variance II - A normal mixture density function is derived by summing two or more normal distributions III - VaR estimates for normal mixtures can be calculated using a closed form analytic formula

A. I and III

B. I, II and III

C. II and III

D. I and II -

Question 288:

Which of the following is the best description of the spread premium puzzle:

A. The spread premium puzzle refers to observed default rates being much less than implied default rates, leading to lower credit bonds being relatively cheap when compared to their actual default probabilities

B. The spread premium puzzle refers to dollar denominated non-US sovereign bonds being priced a at significant discount to other similar USD denominated assets

C. The spread premium puzzle refers to AAA corporate bonds being priced at almost the same prices as equivalent treasury bonds without offering the same liquidity or guarantee as treasury bonds

D. The spread premium puzzle refers to the moral hazard implicit in the monoline insurance market -

Question 289:

Conditional VaR refers to:

A. expected average losses conditional on the VaR estimates not being exceeded

B. value at risk when certain conditions are satisfied

C. expected average losses above a given VaR estimate

D. the value at risk estimate for non-normal distributions -

Question 290:

Which of the following statements are true:

I - The sum of unexpected losses for individual loans in a portfolio is equal to the total unexpected loss for the portfolio.

II - The sum of unexpected losses for individual loans in a portfolio is less than the total unexpected loss for the portfolio.

III - The sum of unexpected losses for individual loans in a portfolio is greater than the total unexpected loss for the portfolio.

IV - The unexpected loss for the portfolio is driven by the unexpected losses of the individual loans in the portfolio and the default correlation between these loans.

A. I and II

B. I, II and III

C. III and IV

D. II and IV

Related Exams:

-

8002

PRM Certification - Exam II: Mathematical Foundations of Risk Measurement -

8004

PRM Certification - Exam IV: Case Studies; Standards: Governance, Best Practices and Ethics -

8006

Exam I: Finance Theory Financial Instruments Financial Markets - 2015 Edition -

8007

Exam II: Mathematical Foundations of Risk Measurement - 2015 Edition -

8008

PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition -

8009

Exam IV: Case Studies: Standards: Governance, Best Practices and Ethics - 2015 Edition -

8010

Operational Risk Manager (ORM) -

8011

Credit and Counterparty Manager (CCRM) Certificate

Tips on How to Prepare for the Exams

Nowadays, the certification exams become more and more important and required by more and more enterprises when applying for a job. But how to prepare for the exam effectively? How to prepare for the exam in a short time with less efforts? How to get a ideal result and how to find the most reliable resources? Here on Vcedump.com, you will find all the answers. Vcedump.com provide not only PRMIA exam questions, answers and explanations but also complete assistance on your exam preparation and certification application. If you are confused on your 8008 exam preparations and PRMIA certification application, do not hesitate to visit our Vcedump.com to find your solutions here.